.png)

You just closed on your third rental property, and tax season is three months away. Your receipts are scattered across email, your glove compartment, and that shoe box in your closet. Meanwhile, you're leaving thousands in deductions on the table, and you don't even know it.

Real estate bookkeeping is the systematic process of recording, categorizing, and managing all financial transactions in your property business. For real estate investors and agents, proper bookkeeping isn't just about staying organized, it's about capturing every legally allowable deduction, maintaining clear cash flow visibility, and avoiding costly IRS audits. Most investors who implement solid bookkeeping systems save between $8,000 and $15,000 annually through better expense tracking and tax planning.

In this guide, you'll learn the exact bookkeeping system that successful real estate investors use to simplify their finances, maximize deductions, and sleep better at night knowing their books are audit-ready.

Real estate bookkeeping is the process of tracking and organizing all money flowing in and out of your property business. This includes rental income, property expenses, loan payments, repair costs, and every receipt in between. Unlike general business bookkeeping, real estate requires tracking multiple properties separately, managing depreciation schedules, and understanding complex tax rules specific to rental properties.

Without proper bookkeeping, you're flying blind. You can't answer basic questions like "Is my Oak Street property actually profitable?" or "Do I have enough cash to cover next month's mortgage payments?" More importantly, poor bookkeeping costs real money.

The IRS allows real estate investors to deduct mortgage interest, property taxes, repairs, maintenance, insurance, property management fees, and even travel to view properties. But you can only claim these deductions if you have proper documentation.

Here's what makes real estate bookkeeping different from other businesses.

First, you're dealing with capital assets that depreciate over 27.5 years for residential rentals.

Second, you need property-level reporting to understand which investments are winners and which are draining your cash.

Third, real estate has unique tax advantages like 1031 exchanges and the qualified business income deduction that require meticulous records to claim properly.

The bottom line? Solid bookkeeping gives you three critical advantages: complete visibility into your portfolio's performance, maximum tax deductions, and peace of mind during an audit. Most successful real estate investors spend 2-3 hours monthly on bookkeeping or outsource it entirely, knowing this investment pays for itself many times over.

The foundation of real estate bookkeeping starts with separation. Open a dedicated business bank account for each property or LLC, this single step prevents 90% of bookkeeping headaches and protects you during IRS audits. When your business and personal expenses are mixed, you create a nightmare for yourself at tax time and raise red flags with the IRS.

Next, choose your accounting method. Most real estate investors use cash-basis accounting, where income is recorded when received and expenses when paid. This method is simpler and matches how most people think about money.

However, if you're managing multiple properties or planning to scale significantly, accrual accounting provides better insights into your true financial position by recording transactions when they occur, not when cash changes hands.

Your software choice matters tremendously.

QuickBooks Online is the industry standard, offering property-specific features and integration with most property management platforms. Alternatives like Stessa and Rentec Direct cater specifically to real estate investors with built-in features for tracking multiple properties, rent collection, and tenant information. Whatever you choose, make sure it can generate property-level profit and loss statements, you need to see each property's performance individually, not just your overall numbers.

Create a chart of accounts tailored to real estate. Standard categories should include rental income, property taxes, insurance, repairs and maintenance, property management fees, HOA dues, utilities, mortgage interest, and depreciation.

The key is consistency, use the same categories every month so you can spot trends and compare properties accurately.

Many investors struggle with whether to handle bookkeeping themselves or outsource it. If you have 1-2 properties and enjoy working with numbers, DIY bookkeeping with good software works fine. Beyond three properties, most investors find that outsourcing bookkeeping services saves them 10-15 hours monthly while ensuring accuracy.

Professional bookkeepers catch deductions you might miss and keep your records audit-ready year-round.

Understanding deductible expenses is where real estate bookkeeping pays for itself. The IRS allows you to deduct any "ordinary and necessary" expense for maintaining and managing your rental properties.

Let's break down what this actually means in practice.

Direct property expenses are your bread and butter deductions. These include property taxes, insurance premiums, HOA fees, property management fees (typically 8-10% of rent), repairs and maintenance, utilities you pay, landscaping, pest control, and cleaning services between tenants. The rule of thumb: if it keeps the property rentable and maintains its current condition, it's deductible.

Here's where investors miss money: the difference between repairs and improvements. Repairs are immediately deductible, fixing a broken window, patching a leaky roof, or replacing a broken appliance. Improvements must be depreciated over time, adding a new room, replacing the entire roof, or upgrading all windows. This distinction matters because repairs give you an immediate tax benefit while improvements spread the deduction over many years.

Professional services are fully deductible. This includes your CPA fees, bookkeeping costs, attorney fees, property inspection costs, and even investment advisory fees. Travel expenses count too. If you drive to inspect a property, meet a contractor, or handle tenant issues, track those miles at the IRS standard rate of 67 cents per mile in 2025.

Don't forget about depreciation, it's often your largest deduction. Residential rental properties depreciate over 27.5 years, commercial properties over 39 years. You can also bonus depreciate certain improvements and equipment. Many investors working with a CPA or qualified bookkeeper discover they've been missing tens of thousands in depreciation deductions simply because their records weren't organized properly.

One critical note: you can only deduct expenses in the year they're paid if you use cash-basis accounting. This is why timing matters, paying property taxes in December versus January can shift your deduction to a more favorable tax year.

The number one mistake is mixing personal and business finances. When you use your personal credit card for property expenses or deposit rental income into your personal checking account, you create a mess that's painful to untangle. Worse, it weakens your legal protection if you're operating as an LLC. The IRS expects clear separation, give it to them.

Poor receipt management kills deductions. You can't deduct what you can't prove. Store receipts digitally using apps like Expensify, Shoeboxed, or even just take photos and save them in property-specific folders.

The IRS requires receipts for expenses over $75, but save everything anyway. During an audit, "I know I bought that" doesn't count, only documentation does.

Not reconciling bank accounts monthly is surprisingly common. Reconciliation means comparing your bookkeeping records against your actual bank statements to catch errors, duplicate entries, or missed transactions. This monthly 20-minute task prevents small errors from becoming big problems. Unreconciled books are like driving with a dirty windshield, you can sort of see where you're going, but details are fuzzy.

Improper expense categorization costs you at tax time. Lumping everything into "miscellaneous" or "property expenses" makes it impossible to identify spending patterns or prove deductions during an audit. Create specific categories and use them consistently. The more detailed your categories, the better you understand your business and the easier tax preparation becomes.

Many investors fail to track property-level performance. If you only look at overall numbers, you can't identify underperforming properties dragging down your portfolio. Smart investors generate monthly P&L statements for each property to spot issues early, like that property with slowly increasing maintenance costs signaling a future major expense.

Finally, waiting until tax season to organize records is a recipe for stress and missed deductions. Real estate bookkeeping works best as a monthly routine, not an annual panic. Investors who review their books monthly make better decisions, catch issues early, and breeze through tax season. Those who avoid common accounting mistakes typically save 15-20 hours during tax preparation and avoid costly filing extensions.

Tracking rental income seems straightforward, tenant pays rent, you record it. But real estate income has nuances that catch many investors off guard. Each property needs its own income tracking to understand which investments are actually profitable and which are barely breaking even.

Set up income streams by property in your accounting software. Don't just record "rental income", specify which property it came from. This granular tracking lets you generate property-specific profit and loss statements. You'll quickly see that your duplex generates 12% returns while your single-family home barely covers its mortgage after expenses.

Beyond base rent, track other income sources separately: late fees, pet deposits, application fees, laundry income, parking fees, and tenant-paid utilities. Why? Because these categories have different tax treatments and help you understand your true income per property. Late fees, for example, might signal tenant quality issues that need attention.

Security deposits require special handling. In most states, security deposits aren't income when received, they're held in trust and only become income if you keep them for repairs or unpaid rent. Track security deposits in a separate liability account until they're earned or returned. This prevents you from accidentally spending money that isn't yours and keeps you compliant with state landlord-tenant laws.

Rent collection timing matters for cash flow management. Create a system that flags late payments immediately. Many investors use property management software that automatically tracks when rent is received, sends late notices, and updates your books. This automation reduces bookkeeping time while improving cash flow visibility, you'll know exactly which properties paid on time and which need follow-up.

For investors with multiple properties, color-coded systems or property-specific naming conventions in your accounting software create instant visual clarity. Property A might be "123 Oak St," not just "rental property." This simple organization pays dividends when you're reviewing reports or preparing taxes for 5+ properties.

The DIY approach works when you're starting with one or two properties, but there's a tipping point where professional bookkeeping becomes essential.

Three factors determine when to outsource: portfolio size, time availability, and tax complexity.

Portfolio size is the clearest indicator. Managing books for 1-2 properties takes 2-3 hours monthly with good software. At 3-5 properties, that jumps to 6-8 hours. Beyond five properties, you're looking at 10+ hours monthly just keeping records current. Most investors find that outsourcing becomes cost-effective at 3-4 properties because the time saved is worth more than the bookkeeper's fee.

Time availability is personal. If you're a high-income professional juggling real estate investments on the side, spending 10 hours monthly on bookkeeping means 10 hours not spent on your primary career or finding new deals. Outsourcing might cost $300-500 monthly but frees up time worth $2,000-3,000 to you. The math is simple.

Tax complexity drives the decision for many investors. If you're using strategies like cost segregation studies, 1031 exchanges, or navigating qualified business income deductions, professional help isn't optional, it's essential. The tax code for real estate is complex, and mistakes cost thousands. Experienced real estate bookkeepers know which expenses are deductible, how to categorize improvements versus repairs, and how to document everything for maximum audit protection.

What does professional bookkeeping cost? For basic monthly services handling 1-3 properties, expect $200-400 monthly. This includes transaction recording, bank reconciliation, monthly financial statements, and basic tax preparation support. For larger portfolios or more complex structures, costs range from $500-1,500 monthly. Most investors find this expense pays for itself through better tax deductions and avoided mistakes.

The middle ground is co-sourcing, you handle day-to-day transactions while a professional reconciles monthly and prepares tax documents. This hybrid approach costs less than full outsourcing while ensuring accuracy where it matters most.

Many fractional CFO services offer this model, providing strategic financial guidance alongside bookkeeping support.

Technology has transformed real estate bookkeeping from a paper-heavy burden into a streamlined process. The right tools reduce bookkeeping time by 60-70% while improving accuracy and providing better insights into your portfolio's performance.

Property management software does the heavy lifting. Platforms like Buildium, AppFolio, and Rent Manager handle rent collection, maintenance requests, and tenant communication while automatically feeding transactions into your accounting system. This integration eliminates manual data entry, the biggest source of bookkeeping errors and wasted time.

Bank feed integration is a game-changer. Connect your business bank accounts and credit cards directly to your accounting software. Transactions download automatically, and you simply categorize them. This takes a process that used to require 3-4 hours monthly and reduces it to 30-45 minutes. Most modern accounting software uses machine learning to remember your categorization choices, making the process faster each month.

Receipt capture apps eliminate the shoe box. Snap a photo of every receipt with your phone, and apps like Expensify or Hubdoc automatically extract key information, attach it to the relevant transaction, and store it securely in the cloud. During an audit, you'll have every receipt organized and searchable in seconds.

Automated reporting provides insights you couldn't get manually. Set up recurring reports that show property-level performance, vacancy rates, maintenance spending trends, and cash flow projections. These reports take seconds to generate but would require hours to create manually. Better information leads to better investment decisions.

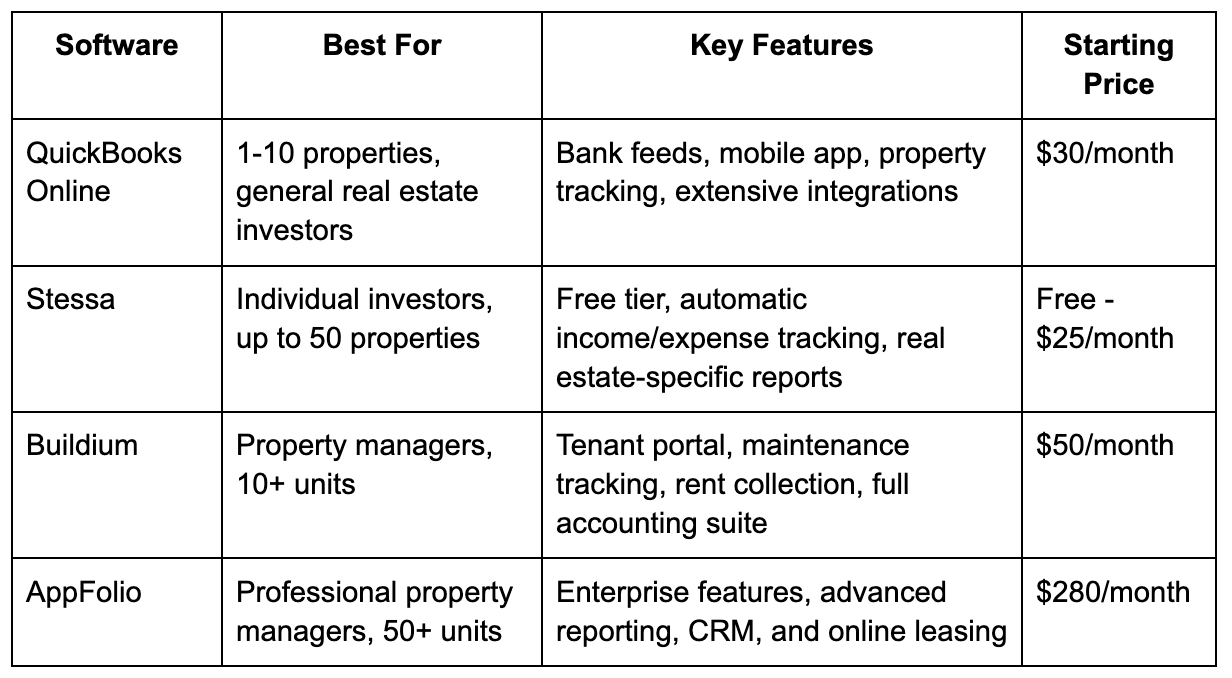

Here's a comparison of popular real estate accounting software options:

The key is choosing software that matches your portfolio size and technical comfort level. Starting with free or low-cost options makes sense for new investors, but as your portfolio grows, investing in more robust systems pays dividends through time savings and better financial visibility.

Cloud-based solutions offer another major advantage: access anywhere, anytime. Review your portfolio's performance from your phone while viewing potential properties. Share real-time financial data with your CPA during tax planning sessions. Give your property manager access to submit expenses without sharing your entire accounting file. This flexibility is impossible with desktop software or paper systems.

The IRS can audit your returns up to three years back, or six years if they suspect substantial underreporting. Having audit-ready books isn't paranoia, it's smart business. The good news? If you're following proper bookkeeping practices, you're already 90% prepared for an audit.

Bank statements and cancelled checks form your primary defense. Keep statements for all business accounts going back at least four years.

These prove money flowed where you claim it did. Digital statements stored securely in the cloud work fine, the IRS accepts electronic records as long as they're complete and readable.

Receipts and invoices support your deductions. The IRS requires receipts for any expense over $75, but smart investors keep everything. Your receipt should show the date, amount, vendor, and business purpose. A credit card statement alone isn't enough, you need the actual receipt. For mileage deductions, maintain a log showing date, destination, miles driven, and business purpose for each trip.

Lease agreements and rental records prove your rental income and terms. Keep copies of all leases, rent rolls showing payment history, and documentation of security deposit handling. If you're claiming vacancy losses, you need proof the property was genuinely available for rent, listing screenshots, showing logs, and marketing expenses demonstrate this.

Property acquisition and improvement records are critical for depreciation calculations. Keep the settlement statement from when you purchased each property, along with receipts for all improvements (not repairs). These documents determine your cost basis and depreciation schedule. Without them, the IRS can disallow your depreciation deductions, often your largest tax benefit.

Insurance policies and tax notices prove you paid deductible expenses. Keep copies of property insurance policies and proof of premium payments. Property tax assessments and payment receipts are essential since property taxes are typically one of your largest deductions.

How long should you keep records? The IRS generally has three years to audit, but keep everything for seven years to be safe. For property acquisition documents and improvements that affect your cost basis, keep them for as long as you own the property plus seven years after you sell it. Digital storage makes this easy, scan everything and store it securely in the cloud with backups.

Organization is as important as keeping records. File documents by property and year, creating subfolders for income, expenses by category, taxes, insurance, and repairs. When the IRS comes knocking, you should be able to produce any document within minutes, not days of searching through boxes.

Working with professionals who understand real estate tax compliance provides additional protection. Experienced bookkeepers and CPAs know exactly what documentation the IRS expects and ensure your records meet those standards before tax season arrives. Many investors find that professional tax planning and preparation services pay for themselves through reduced audit risk and maximized deductions.

While not legally required, separate accounts for each property (or at minimum one dedicated business account for all properties) makes bookkeeping exponentially easier. It provides clear audit trails, simplifies tax preparation, and protects your personal assets if you're sued. Most investors use one business account for smaller portfolios and separate accounts or LLCs for properties valued over $200,000.

Monthly updates are the sweet spot for most investors. This cadence keeps your books current without feeling overwhelming. Record transactions weekly if possible, then reconcile and review reports monthly. Waiting until year-end creates a massive time crunch and increases the likelihood of missing deductions or making errors that cost you money.

Yes, through the home office deduction, but only if you have a dedicated space used exclusively for business. Measure the square footage of your office and calculate what percentage it represents of your total home. You can deduct that percentage of mortgage interest, utilities, insurance, and repairs. Most investors claim $5-8 per square foot using the simplified method, which requires less documentation.

Repairs maintain the property's current condition and are immediately deductible, fixing a broken window, patching a roof leak, or repainting a room. Improvements add value or extend the property's life and must be depreciated over many years, replacing the entire roof, adding a bedroom, or installing new windows throughout. When in doubt, consult your CPA because this distinction affects thousands in tax deductions.

Most small real estate investors use cash-basis accounting because it's simpler, income is recorded when received, expenses when paid. This method matches how you think about money and works well for portfolios under 10 properties. Accrual accounting records transactions when they occur and provides better financial insights for larger portfolios, but requires more sophisticated bookkeeping.

Basic monthly bookkeeping for 1-3 properties typically costs $200-400 monthly and includes transaction recording, reconciliation, and monthly statements. Larger portfolios with 5-10 properties run $500-800 monthly. These fees are tax-deductible business expenses, and most investors find that proper bookkeeping saves them far more in found deductions and avoided mistakes than it costs.

QuickBooks Online dominates the market for investors with 1-10 properties due to its flexibility and integrations. Stessa is popular among newer investors because it's free for basic features and designed specifically for rental properties.

Investors managing 10+ units often prefer property management platforms like Buildium or AppFolio that combine rent collection, maintenance tracking, and full accounting in one system.

Yes, Madras Accountancy offers comprehensive bookkeeping and accounting services tailored to real estate investors and property managers. Our team specializes in multi-property tracking, tax-optimized expense categorization, and preparing audit-ready financial statements. We serve as offshore accounting partners to U.S. CPAs and directly support real estate professionals who need reliable, cost-effective financial management.

Solid bookkeeping isn't about being a numbers person, it's about protecting your investment and keeping more of what you earn. The investors who treat bookkeeping as a monthly habit rather than an annual chore consistently outperform those who don't. They spot problems earlier, make better decisions, and pay less in taxes because they capture every deduction they're entitled to.

Start with the basics: separate bank account, consistent monthly updates, and proper expense categorization. As your portfolio grows, invest in quality software or professional help that scales with you. The few hours or dollars you invest in bookkeeping each month will save you thousands in taxes and countless hours of stress.

If you're managing multiple properties or spending more time on bookkeeping than finding deals, it's time to get professional support. Madras Accountancy specializes in real estate bookkeeping and accounting services for investors and agents across the United States. We handle the details so you can focus on growing your portfolio.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.