After you have seen a few dozen audits of small and mid-sized companies, certain themes start to repeat. The industry changes, the software changes, but the findings often sound familiar.

If you can address these weak spots before an audit, you not only make the auditors happier. You also end up with cleaner books for your own decision making.

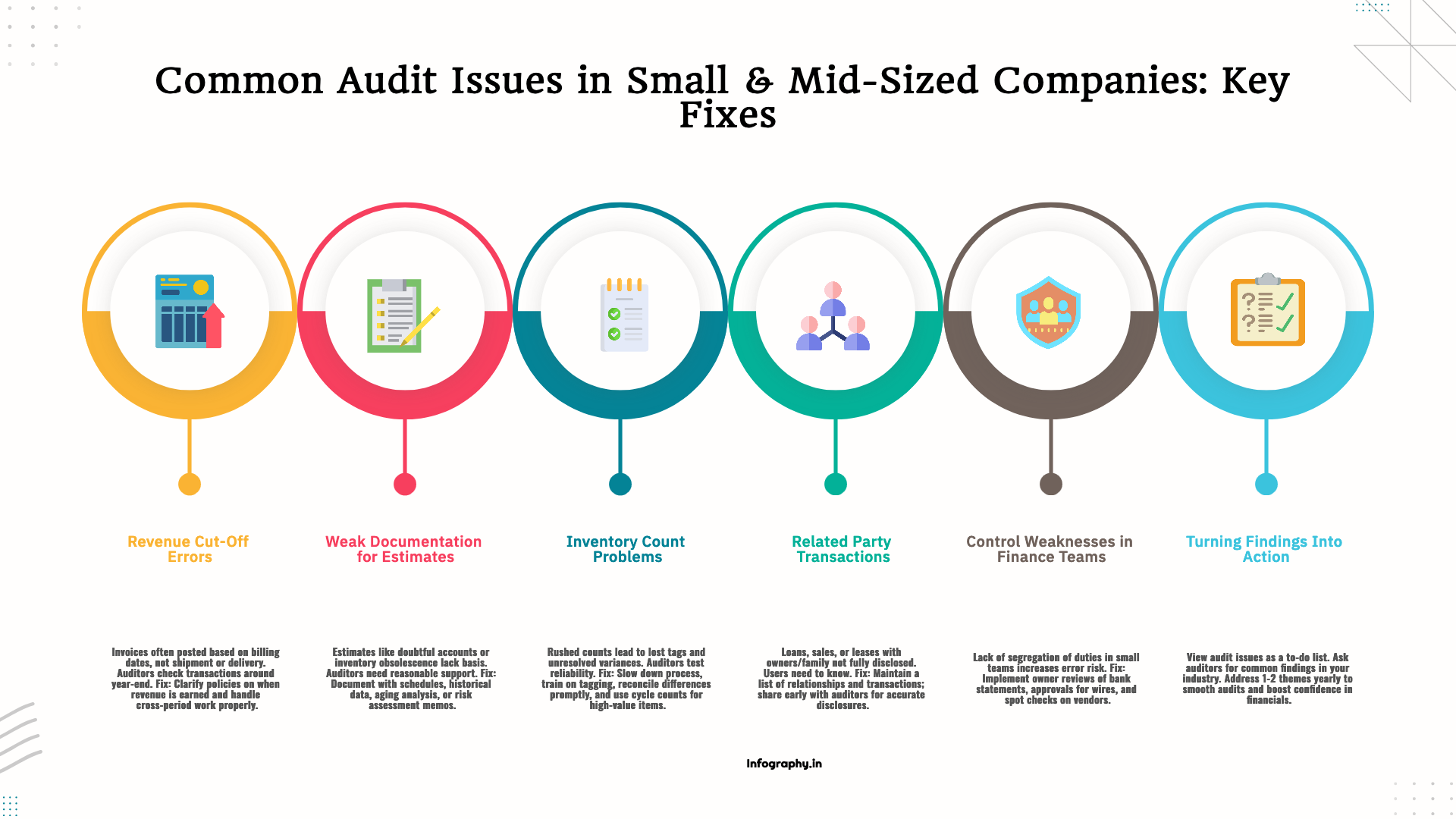

One classic issue involves when revenue is recorded. In the rush to close the year, invoices get posted based on billing dates rather than when goods were shipped or services were delivered. Sometimes invoices for January work end up in December. Other times December work sits unbilled until January.

Auditors test cut off by looking at transactions just before and just after the year end date. If they see patterns of misclassification, they may propose adjustments. To reduce this, clarify your policies: when is revenue considered earned, and how should staff handle work that crosses the reporting date?

Areas that rely on estimates, such as allowance for doubtful accounts, inventory obsolescence, or warranty reserves, often draw scrutiny. Many small businesses make these estimates informally, based on management experience, but do not document how they arrived at the numbers.

Auditors need to see a reasonable basis. That might be a simple schedule showing historical write off rates, aging analysis, or a memo describing how you assessed risks this year compared to last. You do not need a research paper, just a clear trail.

Physical inventory can be messy. Counts are rushed, tags get lost, and differences between the warehouse and the system remain unresolved. When auditors perform test counts or observe your count procedures, they may find gaps that raise questions about the reliability of the recorded balance.

Improvement here usually involves slowing down the count process a bit, training staff on consistent tagging, and reconciling differences promptly instead of brushing them aside. Cycle counts during the year, focusing on high value items, can also reduce surprises at year end.

Another recurring theme is incomplete disclosure of related party transactions. Loans between owners and the business, sales or purchases involving family members, or leases from entities under common control all fall into this category.

These arrangements are not automatically problematic, but users of the financial statements need to know they exist. Keep a list of such relationships and transactions, and share it with your auditors early. That makes it easier to draft accurate disclosures.

Many small companies have just one or two people handling all accounting tasks. That lack of segregation of duties is a common audit comment. The same person might be entering bills, cutting checks, recording deposits, and reconciling bank accounts.

You may not be able to hire a large team, but you can still build basic checks. Owners can review bank statements, approve wire transfers above a certain threshold, or spot check vendor changes. Even modest oversight can lower the risk of errors or misappropriation.

The most useful way to approach common audit issues is to view them as a to do list for strengthening your financial processes. Ask your auditors which findings they see most often in businesses like yours, and which fixes would have the biggest impact.

If you address one or two themes each year, the pile of comments tends to shrink. Over time, your audits get smoother, and your own confidence in the numbers grows. That is the real payoff. For more guidance, see our guide on preparing for your first external audit and materiality and risk in audits.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.