It is easy to fall in love with a property based on its finishes, location, or story. Numbers do not care about any of that. They describe what a deal is actually doing for you, in cash and in long-term wealth. Learning a few core metrics gives you a way to compare options and spot problems early, without getting lost in jargon.

You do not need to memorize every formula in a textbook. Focusing on a handful of measures—cash-on-cash return, cap rate, total return on investment, and debt service coverage—covers most of what everyday investors need.

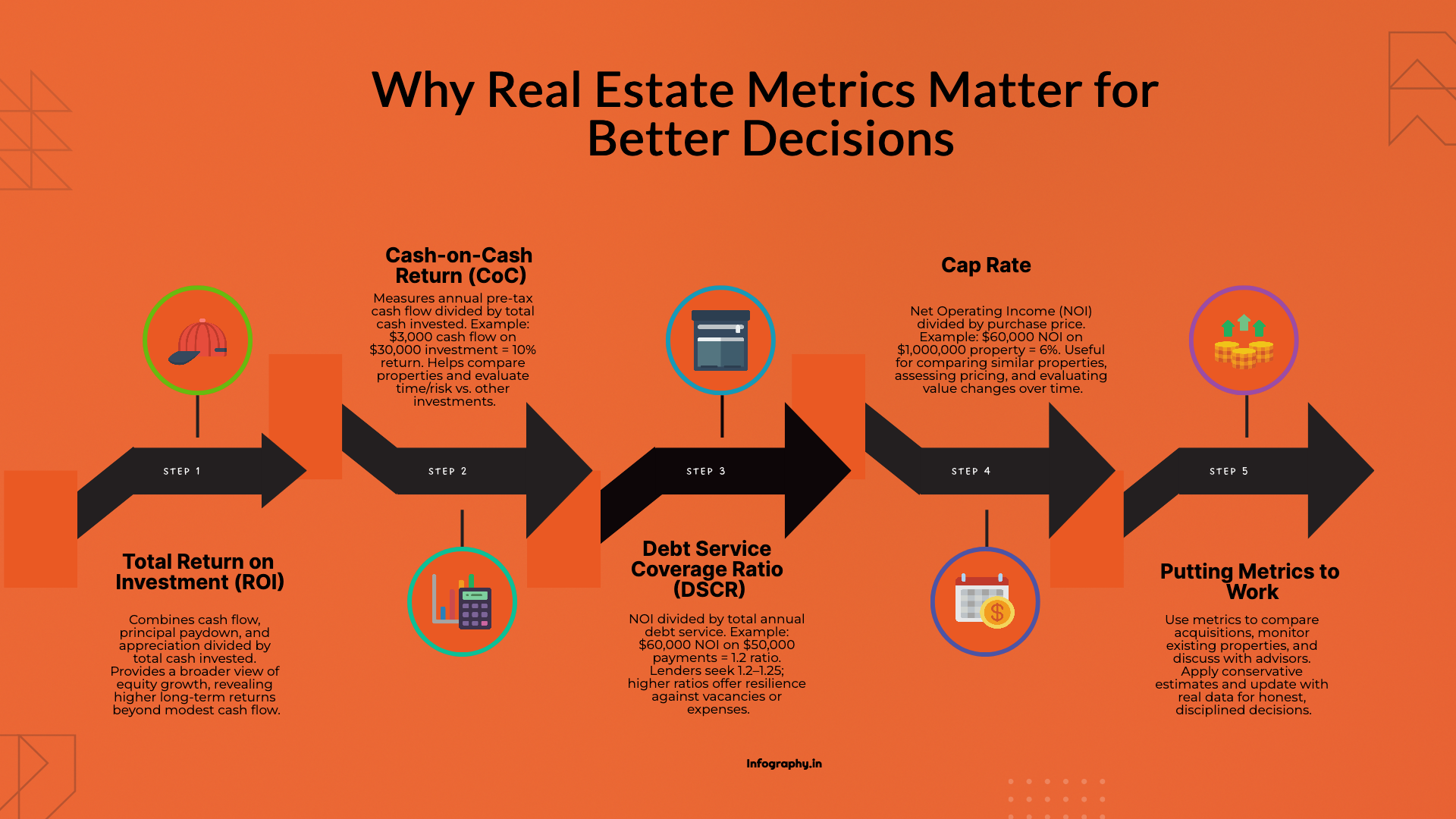

Cash-on-cash return (CoC) looks at how much cash a property puts in your pocket each year compared to the cash you invested. It ignores appreciation and principal paydown and focuses squarely on near-term cash flow.

The basic formula is:

Annual pre-tax cash flow ÷ total cash invested

For example, if you invest $30,000 between down payment, closing costs, and initial repairs, and the property generates $3,000 in cash after expenses and debt service in a year, your cash-on-cash return is 10%.

This metric is helpful when comparing properties or evaluating whether a deal justifies the time and risk involved relative to other uses of your money.

The capitalization rate, or cap rate, is a way to express a property's income-generating ability independent of how you finance it. It answers the question: "If I bought this property with cash, what percentage return would I earn on the purchase price based on current net operating income?"

The formula is:

Net Operating Income (NOI) ÷ purchase price

NOI excludes financing costs and focuses on income minus operating expenses. If a property generates $60,000 in NOI and costs $1,000,000, the cap rate is 6%.

Cap rates are most useful for:

They are less helpful on their own for deciding whether your particular deal is good, because they ignore how you finance and manage the asset.

Return on investment (ROI) takes a broader view. It adds together multiple sources of return—cash flow, principal reduction, and appreciation—to show how much your equity is growing overall.

A simplified version looks like:

(Cash flow + principal paydown + appreciation) ÷ total cash invested

In many real estate deals, cash-on-cash returns may be modest while total ROI is much higher because tenants are paying down your loan and the property's value is increasing. Seeing all components together helps you avoid underestimating the long-term impact of a property that looks only average on cash flow alone.

DSCR measures how comfortably a property's income covers its debt payments. Lenders use it to assess risk; you can use it to test how fragile or resilient your cash flow is.

The formula is:

Net Operating Income ÷ total annual debt service

If NOI is $60,000 and annual loan payments total $50,000, the DSCR is 1.2. Many lenders look for coverage of at least 1.2–1.25, meaning income exceeds debt service by 20–25%. Lower coverage leaves little room for vacancies or unexpected expenses.

For your own planning, a stronger DSCR provides breathing room. If a deal barely meets minimums, ask what changes in rent, expenses, or interest rates would do to coverage.

These metrics are tools, not goals on their own. They are most useful when you:

Equally important is the quality of the inputs. Overly optimistic rent assumptions, underestimated expenses, or ignoring future capital needs can make any deal look good on paper. Using conservative estimates and updating them with actual results over time helps keep the numbers honest.

When you let the metrics inform, but not completely dictate, your decisions, they become a way to bring discipline to what can otherwise be an emotional process. They turn questions like "Does this feel like a good deal?" into clearer prompts: "What does the cash yield look like? How much cushion do we have on the debt? What is driving most of the return here?" Those are questions you can answer—and then act on—with more confidence. For more on cash flow analysis and real estate bookkeeping, see our guides.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.