.png)

You just received three rent payments, paid a plumber for emergency repairs, and your accountant is asking for last quarter's receipts. Meanwhile, you're wondering if that new water heater counts as a repair or a capital improvement for your taxes.

Property rental accounting is the process of tracking all financial transactions related to your rental properties, including rental income, expenses, security deposits, and tax-deductible costs. Unlike personal finance, rental property accounting requires meticulous record-keeping to maximize tax deductions, prove income for future investments, and understand which properties in your portfolio are actually profitable.

Done correctly, rental accounting saves landlords an average of $3,000-$8,000 annually in missed deductions while providing clear visibility into each property's performance. This guide covers everything from choosing the right accounting method to setting up systems that prepare you for tax season in 15 minutes instead of 15 hours.

Property rental accounting is the specialized practice of recording, categorizing, and reporting all financial activities related to rental real estate. This goes beyond simple income tracking, you're managing multiple revenue streams, tracking deductible expenses, handling security deposits, and maintaining records that satisfy IRS requirements.

The main difference between rental accounting and regular business accounting is the property-by-property tracking requirement. If you own three rental properties, you essentially run three separate businesses. Each property needs its own income statement showing rent collected, expenses paid, and net profit or loss. This granular tracking is what the IRS requires on Schedule E of Form 1040.

Your rental accounting system must answer three questions for each property: How much rental income did you collect? What expenses did you incur? What's your net taxable income after deductions? These answers directly affect your tax liability and investment returns. Most landlords who skip proper accounting overpay taxes by 15-30% because they miss deductible expenses or can't prove expenses during an audit.

The IRS gives you significant tax advantages for owning rental properties, depreciation, mortgage interest deductions, and expense write-offs, but only if you maintain documentation. Your accounting system is what turns those potential benefits into actual tax savings.

Accurate rental accounting directly impacts your bottom line in three ways: tax savings, investment decisions, and legal protection. Tax savings alone justify the effort. Landlords with organized books typically deduct $12,000-$25,000 more per property annually than those using shoeboxes and guesswork.

When you track expenses properly, you capture every deductible dollar. That $45 trip to the hardware store? Deductible. The $200 monthly property management fee? Deductible. The $8,000 roof repair? Deductible over time through depreciation. Without accounting records, you'll forget 30-40% of these expenses by tax season.

Investment decisions improve with clear financial data. You can't accurately calculate return on investment without knowing your true expenses. Many landlords think a property is profitable because rent exceeds the mortgage payment. But when you factor in maintenance, vacancy, insurance, and property taxes, that "profitable" property might be losing $200 monthly. Proper accounting reveals this before it becomes a major problem.

Legal protection matters too. If the IRS audits your rental income, you need receipts, bank statements, and transaction records proving every deduction. Without documentation, the IRS will disallow expenses and assess penalties. In audit scenarios, organized landlords walk away unscathed while disorganized ones pay thousands in additional taxes and penalties.

Property financing depends on accurate records. When you apply for your next investment property loan, lenders want 2-3 years of tax returns showing rental income and expenses. Clean books make loan approval faster and help you secure better interest rates because lenders see you as a professional operator.

Tracking rental income starts with separating personal and business finances. Open a dedicated bank account for each rental property or at minimum one account for all your rental operations. Every rent payment deposits into this account, and every property expense pays from it. This separation is critical for both accounting accuracy and IRS audit protection.

Record income as it arrives. When a tenant pays $1,500 rent, log it immediately with the date, property address, and payment method. Don't wait until month-end to batch-record payments. Real-time tracking prevents errors and gives you current cash flow visibility. Beyond rent, remember to record other income sources: late fees, pet fees, parking fees, laundry income, and application fees all count as taxable rental income.

Expense tracking requires more detail. Every expense needs documentation showing the date, amount, vendor, property address, and expense category. The IRS recognizes specific expense categories on Schedule E, so organize your tracking around these: advertising, auto and travel, cleaning and maintenance, commissions, insurance, legal and professional fees, management fees, mortgage interest, repairs, supplies, taxes, utilities, and depreciation.

Use the right tools for your portfolio size. Managing 1-2 properties? A dedicated spreadsheet or basic accounting software like QuickBooks might work. Managing 3-10 properties? Purpose-built rental property software like Stessa, Landlord Studio, or REI Hub will save you hours weekly. Managing 10+ properties? Consider outsourcing your bookkeeping to specialized accounting services that understand real estate.

Digitize everything immediately. Use scanning apps to photograph receipts the moment you get them. Many accounting platforms let you snap photos of receipts and automatically extract the amount, date, and vendor. Paper receipts fade and get lost, digital copies are searchable and permanent.

Landlords have two accounting method options, and your choice affects how you report income and expenses. Most individual landlords use cash basis accounting, while larger rental businesses often use accrual accounting.

Cash basis accounting works for most landlords because it's straightforward and matches your bank account. You report income when you actually receive the payment and deduct expenses when you pay them. If a tenant's $1,200 rent check arrives on January 3rd for December's rent, you report that income in January under cash accounting.

Accrual accounting records transactions when they're earned or incurred, not when cash changes hands. December rent gets recorded in December even if the tenant pays late in January. This method provides a more accurate picture of monthly performance but requires more complex bookkeeping.

The IRS allows most individual landlords to use either method, but you must remain consistent year-to-year. Cash basis is almost always the better choice unless you manage 15+ properties or operate as a corporation. If you're unsure which method fits your situation, review our guide on choosing between cash and accrual accounting methods for your business structure.

The IRS allows rental property owners to deduct ordinary and necessary expenses for managing and maintaining investment properties. Understanding these deductions can save you thousands annually.

Expense Category

What's Deductible

Common Examples

Repairs & Maintenance

Costs to keep property in working condition

Plumbing fixes, painting, appliance repairs, pest control

Property Management

Fees paid to manage the property

Property manager fees (typically 8-10% of rent)

Utilities

Services you pay (not tenant-paid)

Water, sewage, trash, gas, electric (when landlord-paid)

Insurance

Property and liability coverage

Landlord insurance, liability insurance, flood insurance

Property Taxes

Annual real estate taxes

Municipal, county, and state property taxes

Mortgage Interest

Interest portion of mortgage payments

Interest on acquisition loans, refinances, HELOCs

Legal & Professional

Services for property operations

Attorney fees, accountant fees, CPA services, eviction costs

Travel & Mileage

Travel to/from property

IRS standard mileage rate ($0.67/mile in 2025)

Advertising

Tenant finding costs

Zillow listings, signs, newspaper ads, photography

Depreciation

Building value spread over 27.5 years

Residential property depreciation (excludes land)

Repairs versus capital improvements is a critical distinction. Repairs restore property to original condition and are immediately deductible. A capital improvement adds value or extends the property's life and must be depreciated over multiple years. Fixing a broken water heater is a repair ($800 immediate deduction). Installing central air conditioning where none existed is a capital improvement ($8,000 depreciated over 27.5 years).

Most landlords miss travel deductions. Every mile driven to the property, hardware store, or meeting with tenants is deductible at $0.67 per mile. If you drive 2,000 miles annually for your rentals, that's $1,340 in deductions. Use a mileage tracking app to automatically log these trips.

Home office deductions apply if you use space exclusively for rental property management. A dedicated office where you handle bookkeeping, tenant communications, and property research qualifies for a home office deduction calculated by square footage or simplified method ($5 per square foot, up to 300 square feet).

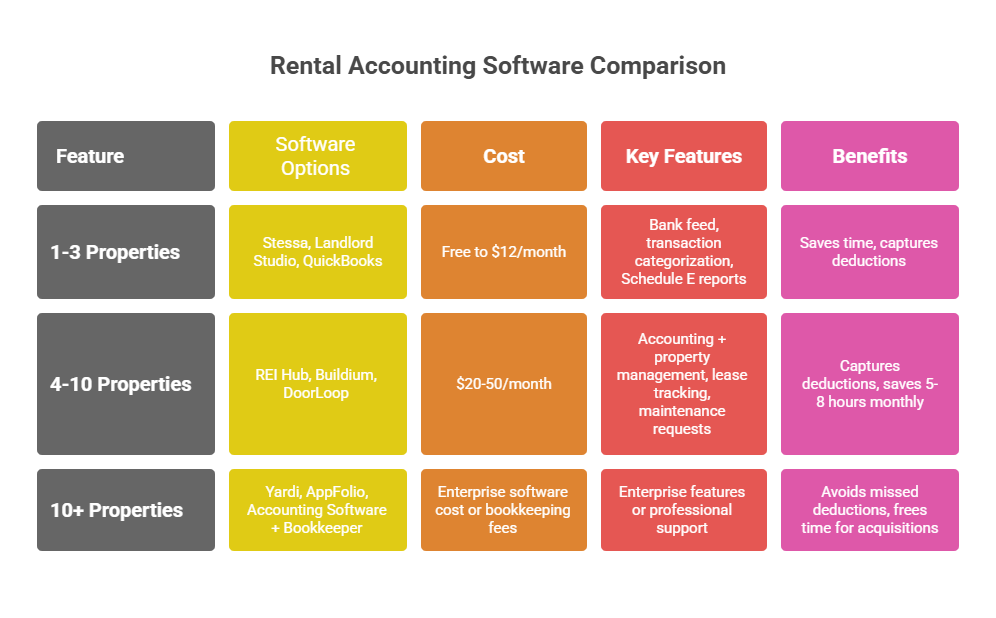

Choosing the right software depends on your portfolio

size and technical comfort level. Free spreadsheets work for 1-2 properties but become unmanageable beyond that. Purpose-built rental accounting software saves time and captures deductions you'd otherwise miss.

For 1-3 properties, consider Stessa (free for unlimited properties), Landlord Studio (free for 3 units, $12/month after), or simple QuickBooks tracking. These platforms connect to your bank accounts, categorize transactions automatically, and generate Schedule E reports for tax filing.

For 4-10 properties, invest in more powerful software like REI Hub, Buildium, or DoorLoop. These platforms combine accounting with property management features: lease tracking, maintenance requests, and tenant communication. The $20-50 monthly cost pays for itself by capturing every deductible expense and saving 5-8 hours monthly on bookkeeping.

For 10+ properties, you need either enterprise software (Yardi, AppFolio) or a combination of accounting software plus professional bookkeeping support. At this scale, missing deductions costs more than hiring help. Many successful rental property investors outsource their accounting entirely once they reach 15-20 units, freeing time to acquire more properties instead of managing spreadsheets.

Key features to prioritize: bank feed connections that import transactions automatically, mobile receipt capture for instant documentation, property-level profit and loss statements, Schedule E report generation, and mileage tracking for travel deductions. These features alone can save landlords $2,000-$5,000 annually in missed deductions and tax preparation fees.

Tax preparation starts with year-round organization, not December scrambling. Landlords who maintain monthly accounting routines spend 90% less time preparing taxes than those who batch-record an entire year in January.

Schedule monthly bookkeeping sessions. Set aside 2-3 hours monthly to categorize transactions, reconcile bank accounts, and file digital receipts. This habit prevents year-end chaos and catches errors while they're still fresh. Most accounting software can handle this reconciliation process automatically if you keep bank feeds connected.

Maintain separate documentation for security deposits. These aren't income when received, they're liability. Only when you keep a portion for damages does it become income. Track security deposits in a separate account or ledger to avoid accidentally reporting them as rental income.

Generate property-level profit and loss statements quarterly. This shows each property's rental income, operating expenses, and net income. Quarterly reviews help you identify underperforming properties and make mid-year adjustments before problems compound.

For guidance on avoiding common pitfalls, review our article on accounting mistakes small business owners should avoid. Many of these principles apply directly to rental property operations.

Prepare Form 1040 Schedule E by pulling data from your accounting system. Schedule E lists income and expenses for each property separately. Your accounting software should generate this form automatically, saving hours of manual data entry. Most tax professionals charge $150-300 per Schedule E property, but clean books often reduce this to $75-150 because the work is already done.

The most expensive mistake is commingling personal and business funds. When your personal expenses and rental income flow through the same account, separating them for taxes becomes nearly impossible. This mistake costs landlords thousands in missed deductions and creates nightmare scenarios during IRS audits.

Missing depreciation deductions costs landlords $3,000-$5,000 annually per property. Depreciation is a non-cash deduction that reduces taxable income by spreading the building's cost over 27.5 years. A $275,000 rental property (excluding land value of $75,000) provides roughly $7,272 in annual depreciation deductions. Landlords who don't claim this are voluntarily paying extra taxes.

Failing to track mileage is leaving money on the table. That trip to Home Depot? Deductible. Driving to show the property to prospective tenants? Deductible. Meeting the plumber on-site? Deductible. At $0.67 per mile, the average landlord with 3 properties misses $800-1,500 annually by not tracking travel.

Not keeping receipts destroys deductions during audits. The IRS can disallow any expense without documentation. That $2,500 water heater replacement becomes non-deductible if you can't prove the expense. Digital receipt storage through accounting software solves this problem by automatically linking receipts to transactions.

Misclassifying repairs as capital improvements or vice versa affects current-year taxes. Repairs are immediately deductible while capital improvements must be depreciated. A $1,000 repair saves you $220-370 in taxes this year (depending on your tax bracket). The same expense incorrectly classified as a capital improvement only saves you $8-13 annually for 27.5 years.

Managing multiple rental properties requires systems that scale. What works for one duplex breaks down at five single-family homes. The key is property-level accounting that rolls up into portfolio-level reporting.

Create a separate chart of accounts for each property within your accounting system. Each property gets its own income and expense categories. This separation allows you to compare property performance, identify which properties generate the best returns, and make data-driven decisions about selling underperformers.

Use property codes or tags to categorize every transaction. When you pay a $300 plumbing bill for 123 Oak Street, tag it with that property's code. Your software can then filter all transactions by property, generating individual profit and loss statements automatically.

Standardize your processes across properties. Use the same expense categories, same vendor management system, and same rent collection process for all properties. Standardization reduces errors and makes it easier to train assistants or property managers as you grow.

Consider entity structuring as your portfolio expands. Many landlords create separate LLCs for groups of properties to limit liability. This adds accounting complexity because each LLC needs its own books, tax returns, and bank accounts. The protection often justifies the cost once you own $500,000+ in rental property. Professional guidance helps determine the right structure, explore our resources on structuring your business for tax efficiency.

Portfolio reporting should show both individual property performance and aggregate numbers. You want to see that 123 Oak Street generated $18,500 net income while 456 Maple Street lost $3,200. This visibility helps you prioritize maintenance spending, adjust rent pricing, and decide which properties to sell or refinance.

How do I report rental income if my tenant pays late?

If you use cash basis accounting (most landlords do), report rental income in the year you actually receive payment, not when it's due. If December rent arrives on January 4th, report it on next year's taxes. Keep documentation showing payment dates in case of IRS questions. For advance rent paid covering future periods, you must report the full amount in the year received regardless of accounting method.

Can I deduct the cost of furniture and appliances in my rental property?

Yes, but the deduction method depends on the item's cost and useful life. Items under $2,500 can often be expensed immediately. More expensive items like refrigerators, washers, or HVAC systems must be depreciated over their useful life (typically 5-7 years for appliances, 27.5 years for structural items). Furniture follows similar rules, inexpensive items expense immediately, while quality furniture depreciates over 5-7 years.

Do I need separate bank accounts for each rental property?

Separate accounts for each property simplify accounting but aren't legally required. At minimum, maintain one dedicated rental business account separate from personal finances. As your portfolio grows beyond 3-4 properties, separate accounts per property become valuable for tracking cash flow and security deposits. Many landlords use one checking account with sub-accounts or accounting software property codes to track separately without multiple physical accounts.

What records should I keep for rental property tax purposes?

Keep all receipts, invoices, bank statements, and lease agreements for at least 7 years. The IRS can audit returns from the past 3 years (6 years if income is understated by 25% or more). Beyond receipts, maintain documentation showing property acquisition costs, improvement expenses, and depreciation calculations. These records prove your tax basis when you eventually sell the property and calculate capital gains.

How does depreciation work for rental properties?

Residential rental properties depreciate over 27.5 years using the straight-line method. You can only depreciate the building value, not the land. If you purchased a property for $350,000 with a land value of $100,000, your depreciable basis is $250,000, giving you $9,091 annual depreciation deduction. This is a paper loss that reduces taxable income without requiring cash outflow, making it one of real estate's most powerful tax benefits.

Should I hire a bookkeeper or accountant for my rental properties?

Hire a bookkeeper if managing 5+ properties becomes time-consuming (expect $200-500 monthly for professional bookkeeping). Hire a CPA or tax accountant at minimum for annual tax preparation, regardless of portfolio size. Tax professionals understand rental property deductions and save most landlords 2-3 times their fee in additional tax savings. Many successful investors use bookkeepers for monthly work and CPAs for tax strategy and filing.

How do I track expenses when I use a credit card for rental property costs?

Open a dedicated credit card exclusively for rental property expenses. This creates an automatic expense log and builds business credit. Categorize and record credit card charges when made, not when you pay the bill. Your accounting software should connect to the credit card account and import charges automatically. Pay the card from your rental property bank account to maintain clean separation from personal finances.

What's the difference between a repair and a capital improvement for tax purposes?

Repairs maintain existing condition and are immediately deductible (fixing a broken pipe, painting a room, replacing broken windows). Capital improvements add value, adapt property to new use, or extend its life beyond one year, and must be depreciated (installing new HVAC, adding a deck, replacing the entire roof, kitchen remodel). IRS Publication 527 provides detailed guidance, but when in doubt, consult a tax professional since misclassification can cost thousands in current-year deductions.

Property rental accounting transforms from overwhelming to manageable when you implement the right systems from the start. Separate bank accounts, consistent transaction tracking, and monthly bookkeeping sessions are the foundation. Most landlords who master these basics save $3,000-$8,000 annually in missed deductions while spending 75% less time on tax preparation.

Start with your accounting method choice and software selection based on your current portfolio size, then commit to recording transactions as they happen rather than batch-processing monthly. The 15 minutes spent categorizing a week's expenses saves 15 hours of chaos during tax season.

At Madras Accountancy, we partner with rental property investors across the US who want professional bookkeeping and tax preparation without hiring full-time accounting staff. Our team understands real estate taxation, tracks property-level performance, and prepares Schedule E forms that maximize deductions while maintaining IRS compliance.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.