.png)

Real estate consolidation accounting combines financial statements of separate legal entities, properties, funds, partnerships, into unified reports under ASC 810 guidance. It determines whether parent companies must consolidate subsidiaries based on control, whether through voting rights or variable interests. Real estate firms use this analysis to accurately report their financial position across complex ownership structures including joint ventures and limited partnerships.

Consolidation accounting merges financial data from multiple legal entities into unified financial statements representing the parent company's complete economic position. For commercial real estate, this typically involves special purpose entities, property-level subsidiaries, and investment funds.

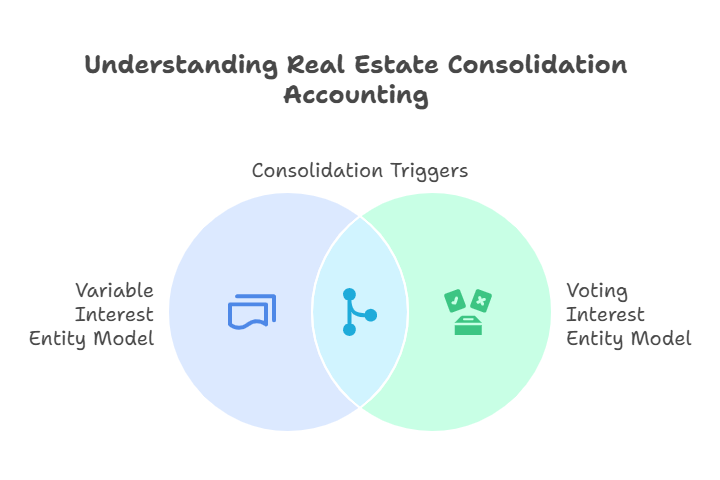

The Financial Accounting Standards Board established ASC 810 to govern consolidation decisions. Companies evaluate each legal entity using two models: the Variable Interest Entity model or the voting interest entity model. Most real estate structures trigger consolidation analysis because properties sit in separate legal entities for liability protection and tax planning.

Key consolidation triggers: ownership exceeding 50% voting interest, power to direct activities impacting economic performance, obligation to absorb entity losses, or general partner status in limited partnerships. Understanding these principles becomes essential when preparing accurate financial statements that reflect true economic control.

ASC 810 requires companies to first determine if an entity qualifies as a Variable Interest Entity. If not, the voting interest model applies. This sequence matters because the models produce different consolidation conclusions for identical ownership structures.

A legal entity becomes a VIE when equity at risk is insufficient to finance activities, equity holders lack power to direct significant activities, or voting rights are non-substantive. Most commercial real estate partnerships meet VIE criteria because limited partners provide capital but lack operational control.

Under the VIE model, the primary beneficiary consolidates the entity. You're the primary beneficiary when you have both power (directing significant activities) and economics (absorbing losses or receiving benefits). The voting interest entity model is simpler, ownership exceeding 50% of voting rights generally requires consolidation unless substantive participating rights prevent effective control.

For CPA firms handling these complexities, leveraging offshore accounting expertise provides technical depth while controlling costs during consolidation processes.

Joint ventures create unique consolidation challenges because partners share decision-making authority. When one venturer has unilateral power to direct significant activities plus absorbs substantial economic variability, it consolidates the joint venture and reports 100% of assets and liabilities with a noncontrolling interest for the partner's share.

If both partners possess substantive participating rights requiring mutual consent for significant decisions, neither consolidates. Instead, both use the equity method, reporting their investment as a single line item. Proportionate consolidation isn't permitted under U.S. GAAP.

Critical factors: approval requirements in operating agreements, deadlock provisions, capital contribution obligations, and distribution waterfall structures affecting economic interests. Real estate investment trusts face additional complexity since ASC 946 doesn't apply to REITs, but REITs in fund structures could be consolidated depending on control assessment.

Recent ASC 810 amendments changed consolidation outcomes for limited partnerships. Current guidance recognizes that general partners typically act as service providers without true control. For limited partnerships that aren't VIEs, usually only a limited partner with substantive kick-out rights consolidates the entity.

Kick-out rights let limited partners remove the general partner without cause through a simple majority vote. When the limited partnership qualifies as a VIE, the general partner consolidates only if it's the primary beneficiary with both power and significant economic exposure. General partners earning customary management fees don't necessarily have economics requiring consolidation.

Limited liability companies structured similarly to limited partnerships follow the same analysis. For firms managing multiple entity structures, proper integration of accounting systems ensures consolidation accuracy across portfolio companies.

Substantive participating rights give investors power to approve or veto significant financial and operating decisions beyond ordinary business operations. These rights prevent consolidation even when one party holds majority ownership. In real estate, participating rights typically cover asset sales, refinancing above thresholds, development expenditures, admission of new partners, or entity dissolution.

Rights become non-substantive when barriers prevent their exercise, such as unanimous consent requirements with related parties or supermajority approval thresholds. The voting interest model and VIE model define substantive participating rights differently, voting model focuses on significant financial decisions while VIE model examines activities most significantly impacting economic performance.

A right to veto management compensation might be substantive participating under the voting model but irrelevant under VIE analysis because it doesn't significantly impact property economic performance. Property sale approval matters under both models. Capital account adjustments and profit allocations don't typically constitute participating rights.

Consolidation analysis requires reassessment when facts and circumstances change, ownership transfers, operating agreement amendments, or refinancing affecting subordination structures. An entity's VIE status can switch to voting interest entity when equity at risk increases or equity holders gain decision-making authority. The primary beneficiary can change through contract amendments or waterfall structure changes.

Maintain robust documentation: complete operating agreements with version control, partnership agreements showing capital accounts, meeting minutes documenting decisions, loan agreements affecting VIE analysis, and consolidation memorandums with ASC 810 citations. Quality documentation protects against audit findings and demonstrates GAAP compliance.

CPA firms processing real estate portfolios benefit from outsourced accounting support that provides technical expertise in ASC 810 application while maintaining consistent quality controls.

Real estate consolidation accounting combines financial statements of multiple legal entities into unified reports under ASC 810 guidance. It determines whether parent companies must consolidate subsidiaries, joint ventures, or variable interest entities based on control assessments. This process ensures accurate reporting of assets, liabilities, and financial performance across complex real estate portfolios.

The Variable Interest Entity model examines power to direct significant activities plus obligation to absorb losses, while the voting interest model focuses on ownership percentages above 50%. VIE analysis comes first. If an entity isn't a VIE, you apply the voting model. Most commercial real estate partnerships qualify as VIEs because equity investors lack typical control through voting rights.

Under current ASC 810 guidance, general partners typically don't consolidate limited partnerships unless they're the primary beneficiary of a VIE. Recent amendments recognize that general partners often act as service providers without true control. Limited partners with substantive kick-out rights may consolidate instead.

Joint ventures require consolidation analysis under ASC 810. If one partner has power to direct significant activities and absorbs substantial economic benefits, consolidation applies. When partners share decision-making through substantive participating rights, the joint venture may use proportionate consolidation or equity method accounting instead.

Substantive participating rights let investors approve or veto significant financial and operating decisions beyond ordinary business operations. In real estate, these include approving asset sales, refinancing, development budgets, or dissolving the entity. Rights must be exercisable and have real economic substance to prevent consolidation.

Reassess consolidation whenever facts and circumstances change materially. Triggers include ownership transfers, amended operating agreements, refinancing, or changes in decision-making authority. An entity's VIE status can switch to voting interest entity or vice versa, requiring immediate analysis and potential financial statement adjustments.

Essential documents include operating agreements, partnership agreements, governing documents, capital account statements, loan agreements, management contracts, and voting records. Proper documentation protects against audit findings and demonstrates compliance with GAAP requirements during financial statement preparation and review.

Yes. Madras Accountancy provides offshore accounting support for U.S. CPA firms handling real estate consolidation. Our team processes complex multi-entity structures, performs ASC 810 analysis, and prepares consolidated financial statements while maintaining quality controls that match in-house standards.

Real estate consolidation accounting demands technical precision in applying ASC 810's dual-model framework. The difference between VIE and voting interest analysis determines which entities consolidate, directly affecting reported leverage, asset values, and financial performance metrics stakeholders rely on for investment decisions.

For CPA firms managing portfolios across multiple properties and ownership structures, accurate consolidation analysis protects against audit adjustments while ensuring financial statements reflect economic reality. The complexity increases with joint ventures, limited partnerships, and related party relationships that require careful documentation and judgment.

Madras Accountancy supports U.S. CPA firms with offshore accounting expertise in multi-entity consolidation, ASC 810 technical analysis, and financial statement preparation. Since 2015, we've processed consolidated financials for 200+ partnerships while maintaining quality standards that match in-house teams.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.