Direct Answer: What Is Vacation Rental Bookkeeping?

Vacation rental bookkeeping is the systematic process of tracking all rental income and expenses for properties listed on platforms like Airbnb and VRBO. It involves separating personal use from rental use, categorizing deductible expenses, and maintaining records that satisfy IRS requirements. Proper vacation rental bookkeeping determines whether you can deduct expenses like mortgage interest, depreciation, and operating costs on Schedule E.

The key distinction: if you rent your vacation home for more than 14 days annually, the IRS requires you to report that rental income and maintain detailed financial records.

Last month, a property owner contacted us panicking about a $12,000 tax bill. The problem? They'd been running their vacation rental for two years without proper bookkeeping. They missed thousands in legitimate deductions simply because they couldn't prove their expenses.

When you convert your vacation home into a rental property, you're essentially launching a business. The IRS views your property differently based on how many days you rent it versus use it personally. This classification determines which tax deductions you qualify for and how you report your rental income.

At Madras Accountancy, we've processed vacation rental bookkeeping for hundreds of property owners since 2015. The owners who establish proper bookkeeping systems from day one save an average of 40% more on taxes than those who scramble to organize receipts at year-end.

The stakes are higher than most realize. Without adequate records, the IRS can disallow your deductions entirely during an audit. We've seen property owners lose $8,000-15,000 in legitimate deductions because they couldn't substantiate their expenses with proper documentation.

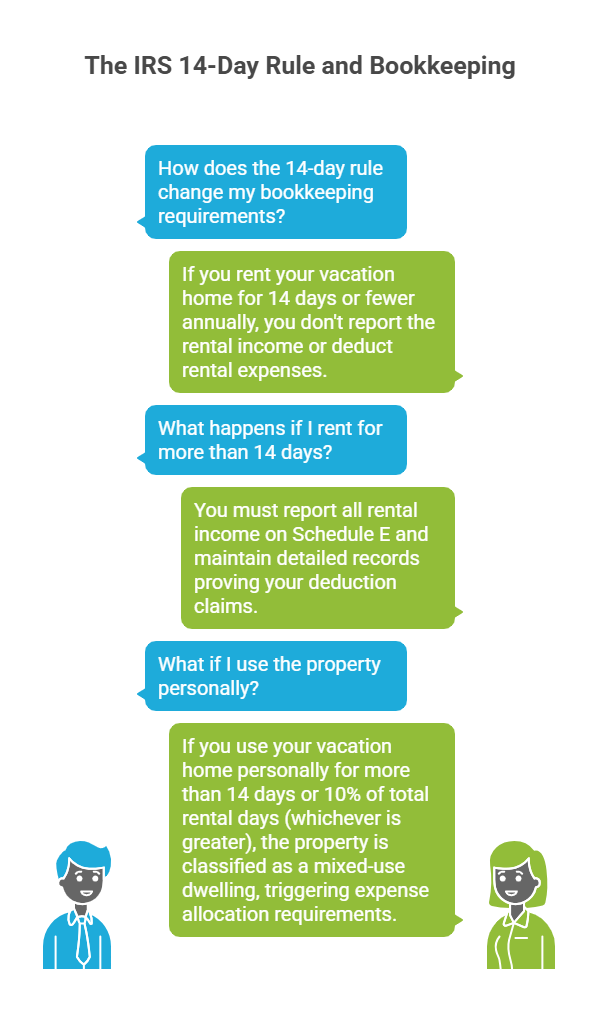

The IRS 14-day rule fundamentally determines your bookkeeping obligations. If you rent your vacation home for 14 days or fewer annually, you don't report the rental income or deduct rental expenses. This tax-free rental income is called the Augusta Rule.

However, once you exceed 14 rental days, everything changes. You must report all rental income on Schedule E and maintain detailed records proving your deduction claims. The complexity increases further based on personal use.

Personal Use Threshold: If you use your vacation home personally for more than 14 days or 10% of total rental days (whichever is greater), the property is classified as a mixed-use dwelling. This triggers expense allocation requirements.

Here's how it works in practice: You rent your vacation rental property for 180 days at $200 per night, generating $36,000 in rental income. You use it personally for 20 days. Since your personal use exceeds the threshold (10% of 180 days = 18 days), you must prorate expenses between rental and personal use.

Calculate your rental use percentage: 180 rental days ÷ 200 total days = 90%. You can deduct 90% of mortgage interest, property tax, insurance, and utilities as rental expenses. The remaining 10% may qualify as itemized deductions on Schedule A if you itemize deductions.

Properties that stay under the personal use threshold qualify as pure rental businesses. You can deduct rental expenses even if they exceed rental income, subject to passive activity loss limitations.

Understanding which vacation rental expenses are deductible saves thousands annually. The IRS Publication 527 provides comprehensive guidance, but here are the categories that matter most:

Mortgage Interest: The largest deduction for most owners. Unlike your primary residence's $750,000 mortgage limit, rental properties have no cap on deductible mortgage interest. If you finance your second home as a rental, all business-portion interest is deductible against rental income.

Property Tax: State and local property taxes for your vacation rental are fully deductible as rental expenses, separate from the $10,000 SALT cap affecting primary residences. This distinction provides significant tax savings for high-value vacation rental properties.

Depreciation: You can depreciate the structure (not land) over 27.5 years once your property is ready for rental. A $300,000 vacation home with $50,000 in land value generates approximately $9,091 in annual depreciation deductions. This "paper loss" reduces taxable income without actual cash outflow.

Operating Expenses: These include cleaning fees between guests, maintenance and repairs, utilities, insurance, HOA fees, property management fees, supplies, linens, and amenities. Platform fees from Airbnb and VRBO (typically 15-20% of booking price) are fully deductible.

Marketing and Software: Website costs, professional photography, listing fees, accounting software, property management software, and booking automation tools qualify as deductible business expenses.

Travel to the Property: If you travel to your vacation rental for maintenance, repairs, or meeting with contractors, those transportation expenses and lodging may be deductible. Keep detailed logs showing business purpose.

Most vacation rental owners we work with miss deductions on smaller items: lightbulbs, toilet paper, coffee supplies, welcome baskets, and other guest amenities. These add up to $1,500-3,000 annually in lost deductions.

Establishing the right bookkeeping system prevents year-end chaos and maximizes deduction claims. Here's the framework that works for 90% of vacation rental owners:

Separate Bank Accounts: Open dedicated bank accounts for your rental operations. Never mix personal and rental transactions. This separation provides clear audit trails and simplifies expense categorization. Link your Airbnb and VRBO accounts to transfer rental income directly into this account.

Choose Accounting Software: QuickBooks Online integrates well with vacation rental platforms through apps like Bnbtally. For simpler operations, spreadsheets work if you maintain consistent categorization. The key is recording every transaction when it occurs, not reconstructing history at tax time.

Create a Chart of Accounts: Structure your categories to match Schedule E reporting requirements:

Document Personal Use: Maintain a detailed calendar tracking every day the property is rented, used personally, or vacant. Include maintenance days (which don't count as personal use). This log is your primary defense during IRS audits for proving expense allocations.

Receipt Management: Photograph or scan every receipt immediately. Use apps like HubDoc or Expensify to digitize receipts as you incur expenses. For expenses over $75, you need receipts showing date, vendor, amount, and business purpose.

After reviewing thousands of vacation rental tax returns, we've identified patterns that consistently trigger problems:

Improper Expense Allocation: Many owners deduct 100% of expenses when they exceed personal use thresholds. If you use your vacation home for 25 days when renting it 150 days, you're over the 15-day limit (10% of 150 = 15 days). You must prorate expenses proportionally.

Missing the Schedule C Requirement: If you provide substantial services like daily housekeeping, meals, or tours, your vacation rental qualifies as a business requiring Schedule C reporting instead of Schedule E. This changes your tax obligations and may subject income to self-employment taxes.

Ignoring State and Local Taxes: Beyond federal income tax, most locations require vacation rental operators to collect occupancy taxes, lodging taxes, or transient occupancy taxes. Rates vary from 8-18% depending on location. These taxes aren't your income—they're pass-through obligations requiring separate tracking.

Claiming Expenses Without Documentation: The IRS requires contemporaneous records. Reconstructing expenses months later using bank statements doesn't satisfy documentation requirements. You need receipts showing what was purchased and its business purpose.

Forgetting Platform Fees: Airbnb and VRBO deduct service fees before depositing funds. Your rental income equals the gross amount guests paid, not the net deposit you received. The difference is a deductible expense, but many owners forget to record it.

The reporting method depends on your usage pattern and service level:

Schedule E (Most Common): Report vacation rental income and expenses on Schedule E if you provide minimal services. This includes most Airbnb and VRBO rentals where you simply provide a furnished space. Rental losses are passive and can only offset passive income unless you qualify as a real estate professional.

Schedule C (Active Business): Use Schedule C if you provide substantial services making your operation a business rather than passive rental. Examples include bed-and-breakfast operations with daily cleaning and meals. Net profits face self-employment tax (15.3% on earnings).

No Reporting (Under 14 Days): Properties rented 14 days or fewer don't require income reporting. However, you also can't deduct rental expenses for those days.

Keep separate records by property if you own multiple vacation rental properties. Each property should have its own income and expense tracking to calculate profit or loss individually.

Most vacation rental owners can handle basic bookkeeping independently during the first year. However, certain situations warrant professional assistance:

CPA firms specializing in real estate understand nuances like the qualified business income deduction for rental properties, passive activity loss rules, and optimal expense timing strategies that can save thousands annually.

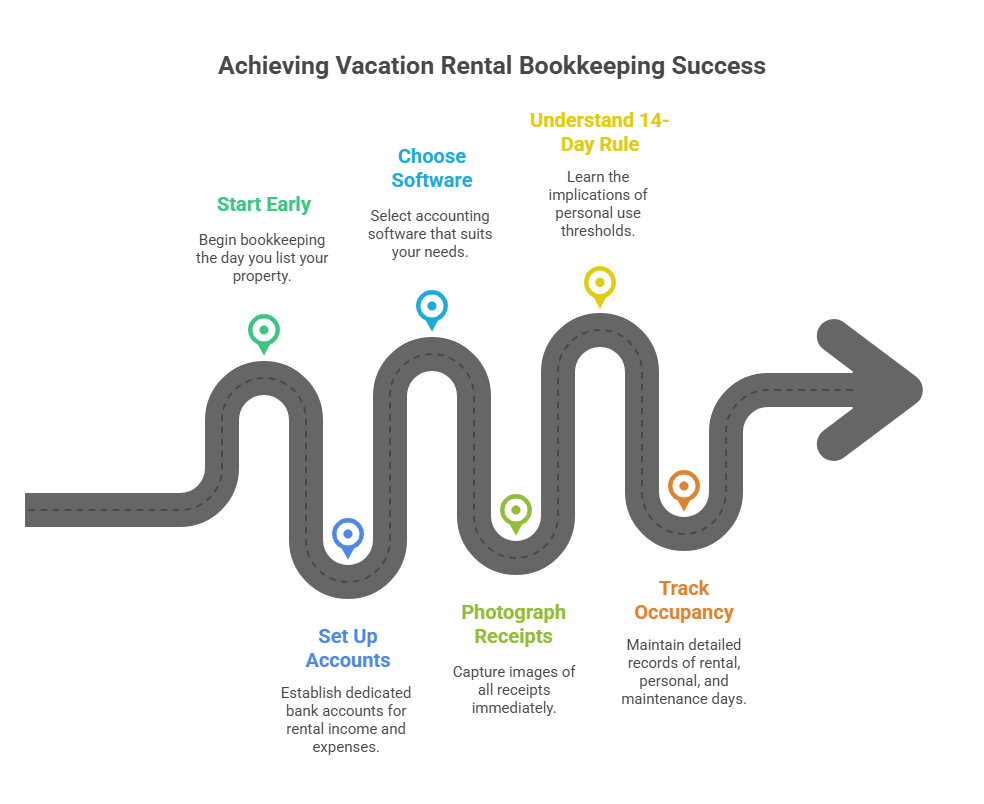

Proper vacation rental bookkeeping starts the day you list your property, not at tax season. Set up dedicated bank accounts, choose appropriate accounting software, and photograph every receipt immediately.

Understanding the 14-day rule and personal use thresholds determines your entire tax strategy. Track occupancy meticulously using calendars that distinguish rental days, personal days, and maintenance days.

The most successful vacation rental owners we work with schedule monthly bookkeeping sessions to categorize expenses and reconcile accounts. This 2-3 hour monthly investment prevents the 40+ hour scramble at year-end and ensures you capture every legitimate deduction.

Remember that vacation rental bookkeeping serves two purposes: IRS compliance and business intelligence. Good records show which months are most profitable, which expenses are trending higher, and whether your rental rate adjustments are working.

Do I need to report income if I only rent my vacation home for two weeks?

No, if you rent your vacation home for 14 days or fewer annually, the IRS doesn't require reporting that rental income under the Augusta Rule. However, you also cannot deduct any rental expenses for those days. This applies regardless of how much you charge—you could earn $10,000 during those two weeks tax-free.

How do I split expenses between personal and rental use?

Calculate your rental use percentage by dividing rental days by total days used (rental + personal). For example, 150 rental days ÷ 200 total days = 75% rental use. Apply this percentage to shared expenses like mortgage interest, property tax, insurance, and utilities. Direct rental expenses like cleaning fees after guest stays are 100% deductible.

Can I deduct the mortgage interest on my vacation rental?

Yes, mortgage interest is deductible based on your rental use percentage. Unlike personal residences with $750,000 loan limits, rental properties have no cap on deductible interest. If your property is 80% rental use, you can deduct 80% of mortgage interest as a rental expense on Schedule E.

What records does the IRS require for vacation rental deductions?

The IRS requires receipts for all expenses over $75 showing date, vendor, amount, and business purpose. For vehicle expenses, maintain mileage logs. Most importantly, keep a detailed calendar tracking rental days, personal days, and maintenance days throughout the year. Store records for at least three years from filing date.

Should I use QuickBooks or can I track expenses in spreadsheets?

For a single vacation rental property with straightforward transactions, spreadsheets work fine if you maintain consistent categorization. QuickBooks becomes valuable when managing multiple properties, needing integration with Airbnb/VRBO, or wanting automated financial reports. The key is recording transactions promptly, regardless of tool.

What happens if I exceed the 14-day personal use limit?

Exceeding 14 days or 10% of rental days (whichever is greater) classifies your property as mixed-use. This limits your rental expense deductions to your rental income—you can't claim rental losses. Proper expense allocation between personal and rental use becomes mandatory for tax compliance.

Are Airbnb and VRBO service fees tax deductible?

Yes, platform fees charged by Airbnb (typically 3% from hosts) and VRBO (5-15%) are fully deductible business expenses. Many platforms deduct fees before depositing funds, so track the gross booking amount as income and the fee as a separate deduction. Guest service fees aren't your responsibility to track.

When should I hire a CPA for vacation rental bookkeeping?

Consider hiring professional help when managing multiple properties, earning over $100,000 in rental income, receiving IRS notices, or facing complex scenarios like cost segregation studies. A CPA specializing in real estate can identify deductions you're missing and ensure proper expense classification that could save $3,000-8,000 annually in taxes.

This guide reflects current IRS regulations for vacation rental bookkeeping. Tax laws change regularly, so consult qualified tax professionals for advice specific to your situation. Madras Accountancy provides comprehensive bookkeeping and tax preparation services for property owners nationwide.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.