Form 4797 (Sales of Business Property) is used to report the sale or disposition of rental property to the Internal Revenue Service, calculating both capital gains and depreciation recapture amounts. When you sell rental property, you must separate the building from the land, reporting the building in Part III to calculate Section 1250 depreciation recapture, and the land in Part I as a Section 1231 gain. This matters because depreciation recapture is taxed as ordinary income (up to 25%), while the remaining gain receives preferential long-term capital gains treatment (typically 15-20%).

Form 4797 is required when you sell depreciable property used in trade or business, including residential rental property. If you claimed depreciation and sold it, the IRS requires Form 4797 to recapture depreciation and categorize gains.

You need it if you sold rental property held for investment or claimed depreciation. It doesn't apply to primary residence sales. The form has four parts, but rental sales primarily use Part I (Section 1231 gains including land) and Part III (building depreciation recapture).

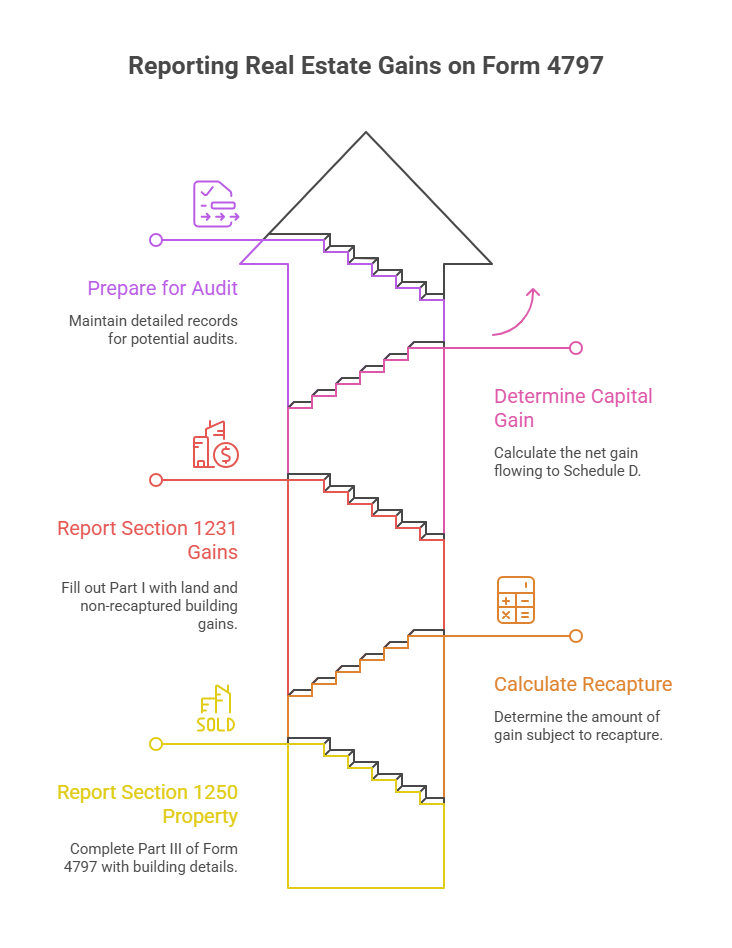

The biggest mistake is failing to separate building from land. Land isn't depreciable, only the building depreciates. The IRS treats these as two distinct sales requiring separate reporting.

If you purchased for $300,000 with $240,000 to building and $60,000 to land, only building depreciates. After six years at $8,727 annually, you've claimed $52,362. Adjusted basis is $187,638.

When selling for $350,000, allocate by fair market value. If building is 80% ($280,000) and land 20% ($70,000), report building in Part III and land in Part I.

Section 1250 property refers to depreciable real property. When you sell, the IRS "recaptures" claimed depreciation, treating it as unrecaptured Section 1250 gain taxed at up to 25%, rather than lower long-term capital gains rates of 15-20%.

Using our example, you sold the building for $280,000 with adjusted basis of $187,638. Total gain is $92,362. The first $52,362 (claimed depreciation) is unrecaptured Section 1250 gain taxed at 25%. The remaining $40,000 gets 15-20% capital gains treatment.

For residential rental property placed in service after 1986 using straight line depreciation, you don't calculate "additional depreciation" on line 26. The entire depreciation is tracked as unrecaptured Section 1250 gain.

Part III (lines 19-29) reports Section 1250 property, the building. Complete lines 19-24: property description, dates, building sale price, cost basis, depreciation, total gain. Line 20 shows building sale ($280,000). Line 21 is original cost plus improvements and selling expenses. Lines 25-29 determine recapture.

Part I (lines 1-8) reports Section 1231 gains from property held over one year, including land and building gain not recaptured in Part III. The $10,000 land gain plus $40,000 non-recaptured building gain go here.

Net gain in Part I flows to Schedule D as long-term capital gain. Losses are ordinary. Audit preparation includes maintaining detailed purchase and improvement records.

Form 4797 integrates with multiple tax forms. Recaptured depreciation (ordinary income) from Part II line 13 flows to Schedule 1 (Form 1040), line 4. Section 1231 gains from Part I line 7 transfer to Schedule D, line 11, combining with other capital gains.

You'll need Form 1099-S showing gross proceeds from the sale. Enter this on Form 4797 line 1a. Errors on Form 4797 cascade through your entire return. Common accounting mistakes often stem from misunderstanding these connections.

First, using the entire sale price for the building instead of allocating between building and land. This overstates gain and depreciation recapture, resulting in overpaid taxes. Always allocate based on fair market value ratios, documented by property tax assessment or appraisal.

Second, entering wrong adjusted basis on line 21. Start with original cost, add improvements and selling expenses, then subtract depreciation. Missing selling expenses (commissions, legal fees, transfer taxes) inflates your gain.

Third, not reporting losses. Form 4797 captures losses that offset other income. Fourth, mishandling mixed-use properties that were primary residences before becoming rentals. Understanding legal tax strategies helps navigate complex situations while staying compliant.

If rental property was destroyed by casualty, theft, or condemnation, you still use Form 4797. Part I includes involuntary conversion gains. If proceeds exceed adjusted basis, you have a gain that can be deferred if you purchase replacement property within two years (three for condemnations).

Report casualty details on Form 4684, then transfer gain to Form 4797 line 3. Depreciation recapture rules still apply.

Many rental owners have suspended passive activity losses, losses that couldn't be deducted in prior years because passive losses only offset passive income. When you dispose of your entire interest in rental property in a fully taxable transaction, those suspended losses are released on Form 8582, potentially reducing or eliminating tax liability from the sale.

Track suspended losses carefully throughout ownership. If you have multiple rentals, released losses only apply to the specific property sold. Outsourced accounting services maintain these tracking requirements across properties and tax years.

Yes, you still need Form 4797 even with a loss. Losses from rental property sales can offset other income, providing valuable tax benefits. Report the loss in Part I of Form 4797, which treats it as an ordinary loss that can reduce your taxable income dollar-for-dollar, potentially saving more tax than a capital loss would.

Yes, a Section 1031 like-kind exchange defers depreciation recapture and capital gains if you reinvest proceeds into similar replacement property within strict IRS timelines. However, the recapture is deferred, not eliminated, it applies when you eventually sell the replacement property without doing another exchange. The depreciation from the original property carries over to reduce your basis in the new property.

If you converted your home to rental use and claimed depreciation, you must report the sale on Form 4797 for the period it was rental property. You may still qualify for the partial Section 121 exclusion ($250,000 single, $500,000 married) for the period it was your primary residence, but depreciation claimed after May 6, 1997 must be recaptured at 25% regardless of the exclusion.

Use the same ratio you used at purchase if possible, adjusted for any improvements. If your original purchase documents don't show the split, use your property tax assessment ratios or get an appraisal. The IRS expects reasonable allocation based on fair market values, typically 70-85% building and 15-30% land for most residential properties, varying by location.

Real estate commissions, attorney fees, title insurance, transfer taxes, escrow fees, and marketing costs are all deductible selling expenses. Add these to your cost basis on line 21 to reduce your gain. Keep all closing documents, the settlement statement (HUD-1 or Closing Disclosure) details all expenses that qualify for deduction.

Unrecaptured Section 1250 gain (the depreciation recapture amount) is taxed at a maximum rate of 25%, while regular long-term capital gains are taxed at 0%, 15%, or 20% depending on your income. The 25% rate applies even if your regular capital gains rate is lower. This makes depreciation recapture more costly than pure appreciation gains.

Partnerships file Form 1065 and report property sales on their own Form 4797, then pass the gains and losses through to partners via Schedule K-1. Partners don't file separate Forms 4797 for partnership property, they report their K-1 amounts on their personal returns. S corporations follow similar rules using Form 1120-S. The entity-level calculation ensures consistent treatment across all owners.

Since 2015, we've processed over 50,000 tax returns for U.S. CPA firms, including complex rental property dispositions. Our offshore accounting team handles the detailed calculations for depreciation recapture, proper building/land allocation, and form integration. We ensure accurate reporting that minimizes tax liability while maintaining full IRS compliance, backed by our same-day error resolution commitment.

Form 4797 complexity increases with multiple properties, installment sales, or mixed-use properties. Reporting errors can mean overpaying taxes or facing IRS penalties. Most investors benefit from professional tax preparation for rental property sales.

Since 2015, Madras Accountancy has processed over 50,000 tax returns for U.S. CPA firms, specializing in Form 4797 preparation and real estate tax planning. Our team ensures accurate reporting that minimizes tax liability while maintaining IRS compliance.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.