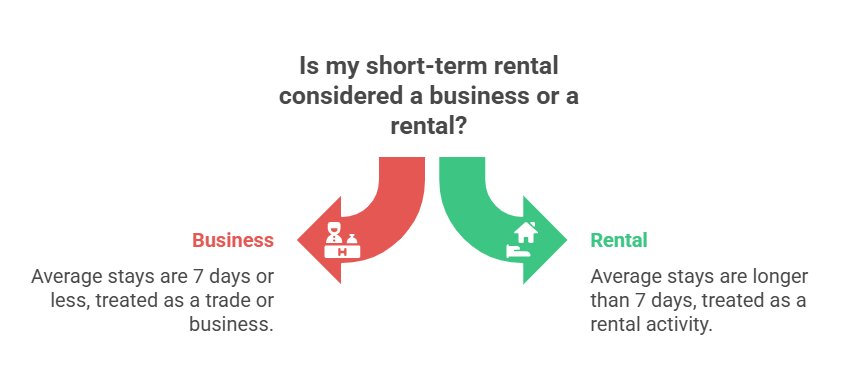

The IRS short-term rental tax loophole allows property owners to deduct rental losses against W-2 income and other active income by treating short-term rentals as a business rather than passive rental activity. Properties with average guest stays of 7 days or less qualify when owners materially participate in operations.

Most rental properties create passive losses that you can't use to reduce your tax bill from your job. But short-term rentals operate under different IRS rules, a gap in the tax code originally written for hotels that now applies to Airbnb and VRBO properties.

Madras Accountancy has processed 50,000+ tax returns for U.S. property owners and CPA firms since 2015. Here's what you need to know.

The term "loophole" catches attention, but this strategy is perfectly legal. The IRS created these rules in the 1990s for hotels, businesses that rent rooms for short stays with daily housekeeping. The regulations couldn't anticipate platforms like Airbnb making short-term rentals accessible to millions of individual owners. When average stays run 7 days or less, the IRS stops viewing your activity as a rental and treats it as a trade or business instead.

The IRS normally classifies rental income as passive. You earn passive income with minimal effort, and the tax code prevents you from using passive losses to offset your salary or business profits.

Short-term rentals escape this restriction when two conditions align. First, your average guest stay must be 7 days or fewer (divide total rental days by number of bookings). Second, you must materially participate in running the property. When you meet both tests, your rental becomes non-passive and your losses can offset active income like W-2 wages.

The IRS provides seven tests for material participation. You only need to pass one.

The 500-hour test requires you spend more than 500 hours during the tax year on your short-term rental activities. Count time spent communicating with guests, coordinating cleaners, handling bookings, performing maintenance, and managing the property. The 100-hour test requires that you work at least 100 hours and no other individual, including contractors, spends more time than you do. If your cleaning service logs 120 hours while you contribute 100, you fail.

Documentation matters enormously. The IRS expects detailed time logs showing what you did and when. Use apps or spreadsheets, just maintain consistent records throughout the year, not reconstructed in April.

The real power emerges when you combine material participation with accelerated depreciation. Standard depreciation spreads your property's cost over 27.5 or 39 years. But short-term rentals qualifying as non-passive open the door to bonus depreciation and cost segregation studies.

A cost segregation study identifies components that depreciate faster, HVAC systems, appliances, flooring, landscaping can become 5-year, 7-year, or 15-year property instead of 39-year. Bonus depreciation allows immediate write-offs of these shorter-life components, creating substantial paper losses in year one that offset W-2 income. Understanding how Section 179 and bonus depreciation work together helps maximize first-year deductions.

For 2025, properties placed in service after January 19 may qualify for 100% bonus depreciation under new legislation.

Property owners make four recurring errors that invite audits. Failing to track hours properly tops the list, you need contemporaneous records, not estimates created later. Note dates, hours, and specific tasks as you work.

Ignoring the personal use limitation creates problems. If you use your property personally for more than 14 days or 10% of rental days (whichever is greater), the IRS treats it as a personal residence, limiting your loss deductions. Miscounting contractor hours undermines your material participation claim. When your property manager spends 300 hours and you log 250, you fail the test.

Claiming the loophole without substantial services for 8-30 day stays causes issues. If average stays exceed 7 days but remain under 30, you must provide hotel-like services, daily cleaning, meals, transportation. Basic amenities like Wi-Fi don't meet this standard.

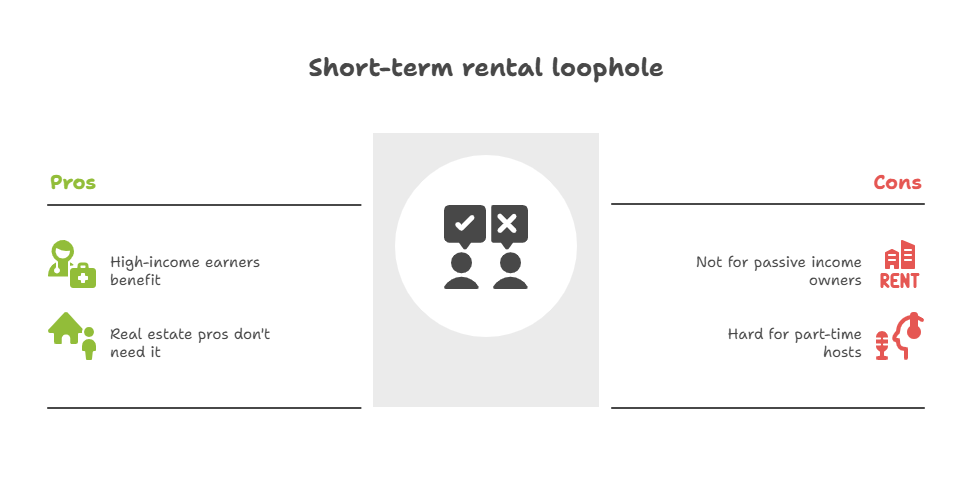

High-income earners with substantial W-2 wages gain the most. Doctors, attorneys, tech professionals earning $200,000+ annually can use rental losses to offset high-bracket income, often saving $20,000+ yearly.

Property owners with existing passive income should evaluate carefully. If you have profitable long-term rentals, making your short-term rental non-passive prevents netting income and losses together. Real estate professionals don't need this loophole, if you already qualify for real estate professional status, you can deduct rental losses without the 7-day requirement. Part-time hosts may struggle to meet material participation tests while working full-time jobs.

Many investors operate through an LLC for liability protection and cleaner recordkeeping. The entity structure doesn't affect tax benefits, the loophole works whether you own property personally or through a pass-through entity.

Start tracking time from day one using apps, spreadsheets, or paper logs. Record guest communications, booking management, cleaning coordination, maintenance, financial management, and marketing. Effective tax planning strategies incorporate proactive record-keeping throughout the year.

Calculate your average stay monthly to ensure you stay under 7 days. One 30-day booking can push your annual average above the threshold without enough shorter stays to offset it. Maintain separate books for each property, the IRS expects individual tracking for material participation.

Federal tax benefits mean nothing if local regulations shut down your operation. Many cities restrict short-term rentals through zoning laws, permit requirements, and occupancy limits. Research your jurisdiction's rules before investing, some areas prohibit rentals entirely or cap rental days at 90-120 per year.

Occupancy taxes add another layer. Most locations charge lodging taxes on short-term rentals, typically 8-15%. You're responsible for collecting from guests and remitting to authorities. HOA restrictions can also prevent short-term rentals, review covenants and obtain written approval before starting operations.

If you earn over $250,000 annually, own multiple properties, or combine this strategy with cost segregation studies, work with a CPA who specializes in real estate taxation. Our tax planning and preparation services help property owners implement these strategies correctly from the start.

First-time owners benefit from establishing proper systems early. Setting up correct bookkeeping and tracking methods in year one prevents problems that take years to fix. Building an audit-ready file from day one provides peace of mind and protects your tax savings.

Yes, you can convert existing long-term rentals to short-term rentals and apply this strategy. Start tracking hours and average guest stays from the conversion date forward. You'll need to meet all requirements during the tax year you claim the benefits.

The loophole only applies in years when you meet both requirements. If your average exceeds 7 days in a particular year, your rental income reverts to passive status for that year only.

Most tax professionals treat qualified short-term rentals as rental activities exempt from self-employment tax, even when classified as non-passive. The IRS hasn't provided definitive guidance. Consult your tax advisor about your specific situation.

The 14-day rule (allowing tax-free rental income for fewer than 15 rental days annually) and the short-term rental loophole are separate provisions. You generally can't use both on the same property in the same year.

The 3.8% NIIT applies to passive rental income when modified AGI exceeds $250,000 (married filing jointly) or $200,000 (single). Qualifying your short-term rental as non-passive excludes that income from NIIT.

Keep detailed time logs showing dates, hours, and activities. Maintain rental agreements showing guest stay lengths, receipts for all expenses, contractor invoices with hours worked, and booking platform reports. Store documentation for at least three years after filing.

The IRS short-term rental tax loophole creates legitimate tax savings when properly implemented. High-income property owners can offset $30,000 to $100,000+ in W-2 income through rental losses from depreciation and operating expenses. Success requires meeting specific tests, maintaining detailed records, and working with tax professionals who understand real estate strategies. The benefits are substantial, but compliance requirements are strict, structure your operations correctly from the start.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.