.png)

You're looking at a profitable rental property, $2,400 monthly rent, maybe $1,800 in expenses. But is it really profitable when you factor in your $180,000 mortgage? What's your actual equity? How much depreciation should you claim this year?

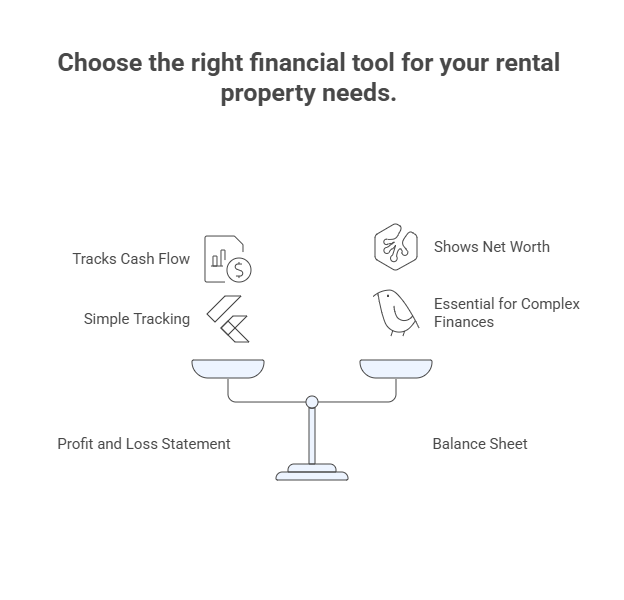

The answer: A rental property balance sheet gives you this complete financial picture instantly. Unlike your profit and loss statement that tracks cash flow, a balance sheet shows what you own, what you owe, and your true net worth in a property, critical data when securing financing, planning tax strategy, or deciding whether to refinance or sell.

Most landlords with 1-2 properties can skip formal balance sheets and rely on simpler tracking. But once you hold multiple properties, seek commercial financing, or bring in partners, a balance sheet becomes essential. This guide provides a real-world rental property balance sheet example, shows you exactly how to build one, and includes a free template you can use today.

A rental property balance sheet is a financial snapshot showing your investment's assets, liabilities, and equity at a specific point in time. Think of it as a photograph of your property's financial health on December 31st or June 30th, capturing what you own (assets) minus what you owe (liabilities) to reveal your true ownership stake (equity).

The balance sheet follows a fundamental accounting equation: Assets = Liabilities + Owner's Equity. This equation always balances, which is why it's called a balance sheet. For rental properties, assets include the property value, any cash in property accounts, and accounts receivable (rent owed to you). Liabilities cover your mortgage balance, credit card debt, unpaid property taxes, and refundable security deposits. The difference is your equity, your actual ownership value in the property.

Unlike an income statement that shows monthly or annual cash flow from rent minus expenses, a balance sheet reveals accumulated value. Your property might show negative cash flow for a month due to major repairs, but the balance sheet could show $80,000 in equity. This distinction matters when lenders evaluate loan applications or when you're deciding whether to hold or sell a property.

Balance sheets also track accumulated depreciation, the total depreciation you've claimed over time to reduce taxable income. This becomes crucial at sale time when calculating depreciation recapture taxes. For comprehensive guidance on managing rental property finances, including reading balance sheets alongside other financial statements, deeper resources help you understand how these reports work together.

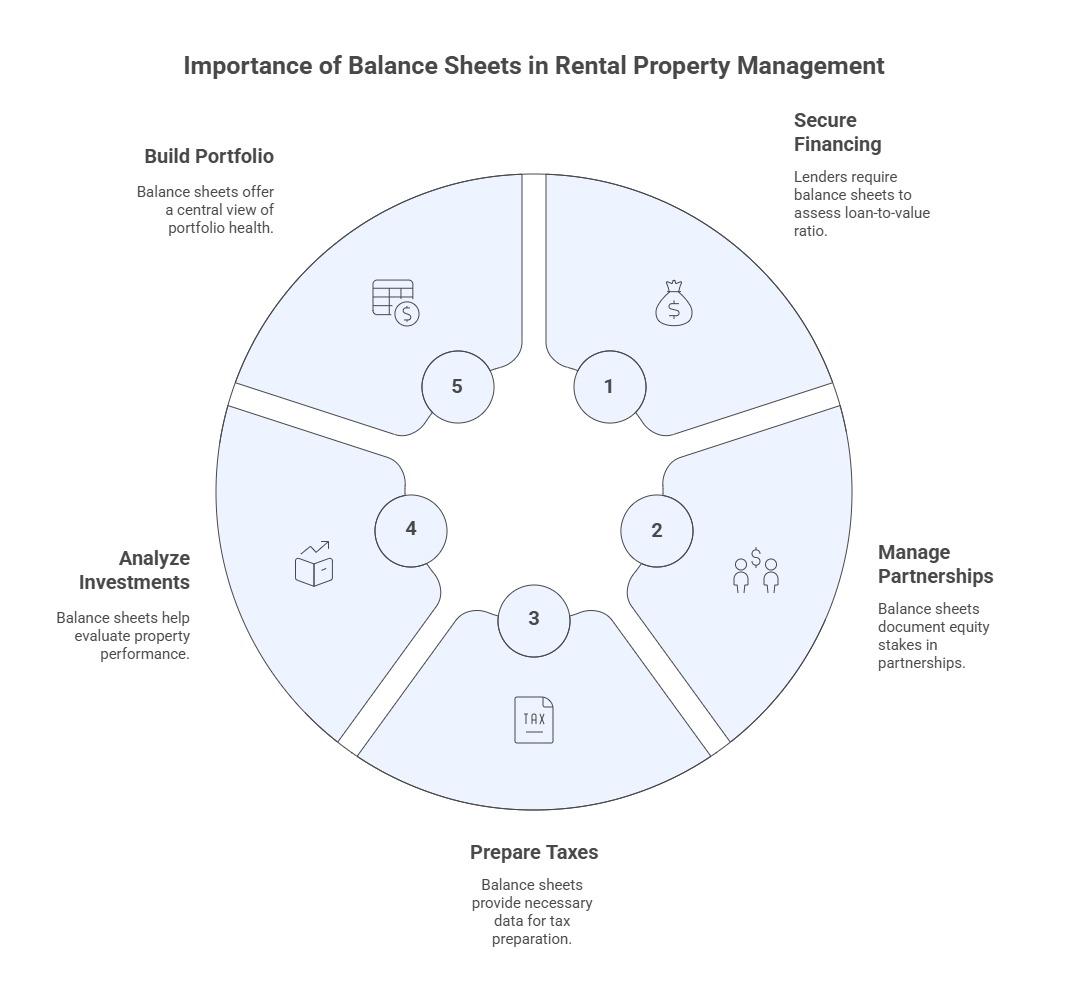

Most landlords with a single rental property don't need formal balance sheets. Simple tracking in a spreadsheet showing rent collected, expenses paid, and maybe a separate note on mortgage balance works fine. But balance sheets become essential in specific situations.

When securing financing or refinancing, lenders require balance sheets to assess your loan-to-value ratio and overall financial position. A bank wants to see that your property value of $250,000 against a mortgage of $150,000 gives you substantial equity cushion. Without a balance sheet presenting this clearly, loan applications stall.

For properties held in partnerships or LLCs with multiple owners, balance sheets provide objective documentation of each owner's equity stake. When one partner wants to buy out another, the balance sheet establishes fair market value and ownership percentages.

Tax preparation becomes significantly easier with accurate balance sheets. Your CPA needs your property's cost basis and accumulated depreciation to complete Schedule E properly.

Come tax time, providing your accountant with a well-maintained balance sheet instead of asking them to reconstruct records from scattered documents saves hours of billable time. Many real estate investors use professional tax preparation services to ensure their depreciation and basis calculations remain accurate across multiple properties.

Investment analysis requires balance sheets when evaluating whether to hold or sell properties. A property showing $500 monthly negative cash flow might seem like a poor investment until the balance sheet reveals you've gained $40,000 in equity through appreciation and mortgage paydown in three years.

That context changes the hold-vs-sell decision.

Finally, building a comprehensive portfolio demands professional financial management. Once you own 3-4 properties, especially across different LLCs or partnerships, manually tracking everything in separate spreadsheets becomes error-prone.

Balance sheets become your central source of truth for portfolio-level financial health. For landlords scaling beyond a few units, outsourced bookkeeping services handle balance sheet maintenance while you focus on property operations.

Every rental property balance sheet has three main sections that always balance according to the equation: Assets = Liabilities + Equity. Here's how each section works with specific rental property examples.

Assets Section - What You Own

Current assets convert to cash within one year. Cash and cash equivalents include your property bank account balance, let's say $8,500. Accounts receivable covers rent owed to you, perhaps $2,400 if one tenant hasn't paid this month. Prepaid expenses might include $1,200 of prepaid insurance that covers the next 6 months.

Fixed assets hold longer-term value.

The rental property itself appears at cost basis, not market value. If you bought a duplex for $200,000, that's your recorded value regardless of current $250,000 market value. Land value gets separated, let's say $20,000, because land doesn't depreciate. The building value of $180,000 gets depreciated over 27.5 years per IRS rules, creating annual depreciation of $6,545.

After three years, accumulated depreciation totals $19,635. Your balance sheet shows the building at $180,000 minus $19,635 accumulated depreciation equals $160,365 net value.

Other fixed assets include appliances, property improvements, and equipment. If you installed a $5,000 HVAC system last year, it appears here with its own depreciation schedule.

Liabilities Section - What You Owe

Current liabilities require payment within one year. Accounts payable might show $1,500 owed to contractors for recent repairs. Refundable security deposits of $4,800 (two months' rent from two tenants) appear here because you'll eventually return these. Unpaid property taxes of $2,100 for the current quarter sit in current liabilities.

Long-term liabilities extend beyond one year. The mortgage principal balance is your largest liability, perhaps $152,000 remaining on the original $170,000 loan after three years of payments. Note that only the principal balance appears on the balance sheet; interest payments flow through your income statement as expenses, not balance sheet items.

Credit card balances for property expenses of $3,200 might appear under liabilities if you're carrying balances rather than paying monthly. Unpaid taxes or liens against the property also sit here.

Equity Section - Your Ownership Stake

Owner's equity starts with your initial investment, the $30,000 down payment plus $8,000 in closing costs equals $38,000 initial capital. Each year's profit or loss from your income statement flows into retained earnings. If you had $12,000 profit in year one, $9,500 in year two, and $11,200 in year three, retained earnings total $32,700. Current year profit of $14,100 appears separately. Total equity is $84,800 ($38,000 + $32,700 + $14,100).

This equity section represents your true ownership value in the property. It grows through mortgage paydown, property appreciation (though appreciation doesn't appear until sale or appraisal updates), and accumulated retained earnings from positive cash flow.

Here's a realistic balance sheet for a single-family rental property purchased three years ago for $200,000 (including $20,000 land value) with a $170,000 mortgage:

ABC Rental Property LLC - Balance Sheet

As of December 31, 2024

ASSETS

Current Assets:

Fixed Assets:

TOTAL ASSETS: $198,065

LIABILITIES

Current Liabilities:

Long-Term Liabilities:

TOTAL LIABILITIES: $160,400

OWNER'S EQUITY

TOTAL LIABILITIES + EQUITY: $198,065

Notice how the balance sheet balances: Total Assets ($198,065) exactly equal Total Liabilities + Equity ($198,065). This is the fundamental check that your balance sheet is correctly prepared.

The key insight from this example: Despite having taken $47,135 in distributions over three years, the owner still maintains $37,665 in equity. The property value shown ($180,365 net building value) is based on original cost less depreciation, not current market value. If the property appreciated to $250,000 market value, that unrealized gain doesn't appear until a new appraisal or sale.

Depreciation is the single most important calculation for rental property balance sheets because it affects both your balance sheet and your tax return. The IRS allows residential rental properties to be depreciated over 27.5 years, meaning you can deduct a portion of the building's value each year to reduce taxable income.

Step 1: Determine depreciable basis. Start with your total purchase price, then subtract the land value. Land never depreciates. If you bought a property for $200,000 and the county assessor values the land at $20,000 (10% of total), your depreciable basis is $180,000. If you're unsure of land value, check your county's tax assessment, they separate land from improvement values.

Step 2: Calculate annual depreciation. Divide your depreciable basis by 27.5 years. For a $180,000 building, annual depreciation is $6,545 ($180,000 / 27.5 = $6,545.45, typically rounded). This amount gets deducted on your tax return each year as a depreciation expense, reducing your taxable rental income.

Step 3: Track accumulated depreciation. Each year, add the annual depreciation to your running total. After year one: $6,545. After year two: $13,090. After year three: $19,635. This accumulated depreciation appears on your balance sheet under Fixed Assets as a contra-account (negative value) that reduces the building's book value.

Step 4: Update your balance sheet. Your balance sheet shows: Building at Cost $180,000, Less Accumulated Depreciation $19,635, equals Building Net Value $160,365. This net value represents your property's "book value", not market value, but the accounting value after depreciation.

The tax implication: When you eventually sell the property, the IRS recaptures all that depreciation. If you claimed $50,000 in depreciation over 8 years then sold the property, that $50,000 gets taxed as ordinary income (up to 25% rate) before calculating capital gains on the remainder. Tracking accumulated depreciation accurately on your balance sheet ensures you know your potential tax liability at sale time.

For capital-intensive improvements like a new roof ($15,000) or HVAC replacement ($8,000), these don't get expensed immediately. Instead, they're added to Fixed Assets and depreciated over their useful lives, typically 27.5 years for structural improvements or 5-15 years for equipment. Understanding these rules is crucial for managing your tax obligations properly.

Many landlords confuse balance sheets with income statements (also called profit and loss statements), but they serve completely different purposes and answer different questions about your rental property.

An income statement shows financial performance over a period of time, typically monthly, quarterly, or annually. It answers: "Did I make money this period?" The income statement lists all rental income collected, subtracts all operating expenses paid, and shows whether you had profit or loss. It's like a video showing cash flowing in and out over time.

A balance sheet shows financial position at a single point in time. It answers: "What's my total investment worth right now?" The balance sheet lists what you own (assets), what you owe (liabilities), and calculates your equity. It's like a photograph frozen at December 31st showing your net worth.

Example of the difference: Your December income statement might show:

That same December balance sheet shows:

One bad month with $800 loss doesn't mean your investment is underwater. The balance sheet reveals you still have $37,665 in equity built up over three years. Both reports together give the complete picture: the income statement tracks monthly operating performance, while the balance sheet tracks accumulated wealth.

Most property management software generates both reports automatically. For landlords managing multiple properties, having both income statements and balance sheets provides complete financial visibility. The income statement helps you spot underperforming properties month-to-month, while the balance sheet shows which properties have gained the most equity.

Here's the practical reality: small landlords with 1-2 properties rarely need formal balance sheets. If you own a single rental house with straightforward finances, a simple spreadsheet tracking monthly rent and expenses suffices. Your tax preparer can work from that basic information plus year-end mortgage statements.

Balance sheets become essential in specific situations:

Loan applications and refinancing: Every commercial lender requires balance sheets to evaluate your financial strength. When you apply to refinance a rental property or secure a line of credit against your portfolio, lenders want to see assets versus liabilities presented professionally. They're calculating loan-to-value ratios and debt service coverage ratios, both require accurate balance sheet data.

Multiple property portfolios: Once you own 3+ properties, especially across different LLCs or legal entities, consolidated balance sheets become necessary for managing your overall financial position. Without balance sheets, you're guessing at total equity across your portfolio. Balance sheets for each entity, plus a consolidated view, show your true net worth.

Partnership or LLC structures: If you co-own rental properties with partners, formal balance sheets document each owner's capital account and ownership percentage. When partners want to exit, buy each other out, or bring in new investors, the balance sheet provides objective valuation. Without it, disputes over "fair value" drag on.

Property sales and 1031 exchanges: When selling a rental property, your balance sheet provides the cost basis and accumulated depreciation needed for calculating capital gains and depreciation recapture taxes. For 1031 exchanges, accurate basis tracking ensures you properly defer gains into the replacement property.

Portfolio expansion: As you scale from 2-3 properties to 5-10+, maintaining balance sheets for each property plus consolidated statements becomes standard practice. Professional real estate investors treat their portfolios as businesses, and businesses maintain balance sheets. For investors at this stage, professional bookkeeping services handle monthly balance sheet updates, ensuring accuracy without consuming your time.

If none of these situations apply to you, don't overcomplicate your accounting. A simple income/expense spreadsheet and annual tax return filing handles most small landlords' needs just fine.

Creating balance sheets manually in Excel works for small portfolios, but automation saves substantial time as you grow. Modern property management software generates balance sheets automatically from your daily transactions.

The automation works like this: When you record rent payment in your property management software, it updates both your income statement (adds rental income) and your balance sheet (increases cash assets). When you pay a mortgage payment, the software splits the payment between principal (reduces mortgage liability on balance sheet) and interest (expense on income statement). Security deposits received increase both cash assets and security deposit liability. Every transaction updates both reports simultaneously.

Quality software also tracks depreciation automatically. You enter your property's purchase price and land value once, and the system calculates annual depreciation, updates accumulated depreciation on the balance sheet, and generates the depreciation schedule your CPA needs. This eliminates the manual calculations and reduces errors.

For landlords managing multiple properties, software generates individual balance sheets for each property plus consolidated balance sheets showing your entire portfolio. You can instantly see which properties have the most equity, which carry the highest debt ratios, and where your total net worth stands.

Popular platforms like Buildium, Landlord Studio, and REI Hub specialize in rental property accounting. They offer bank feed integration, automated transaction categorization, and one-click financial report generation. The trade-off is monthly subscription costs ($30-$200 depending on portfolio size), but most landlords find the time savings and accuracy improvements worth the investment.

For landlords who prefer focusing on property operations rather than bookkeeping, partnering with offshore accounting professionals provides an alternative. They handle daily transaction coding, monthly reconciliations, and balance sheet updates in your software, delivering clean financial reports while you manage tenants and properties.

We've created a comprehensive rental property balance sheet template you can download and customize for your properties.

What's included in the template:

How to use this template:

The template works for single-family homes, duplexes, small multifamily properties, and commercial rentals. Simply make a copy for each property you own, or use the multi-property tab to consolidate several properties into one balance sheet.

Customization tips: Add line items specific to your situation, perhaps you have property tax reserves, insurance escrow accounts, or lines of credit. Delete sections that don't apply. The template structure follows standard accounting principles but remains flexible for your specific needs.

Remember that this template provides a starting point. For complex situations like multiple LLCs, partnership structures, or portfolios exceeding 5 properties, consider professional accounting software or outsourced accounting services to ensure accuracy and save time.

How often should I update my rental property balance sheet?

Most landlords update balance sheets quarterly or annually. If you're applying for loans, refinancing, or bringing in partners, update monthly to show current financial position. Small landlords with simple finances often update just once yearly at tax time. The key is consistency, whatever frequency you choose, stick with it so you can track trends over time. Property management software can update balance sheets daily if needed, but quarterly reviews work well for most investors.

Do I include rental income on my balance sheet?

No, rental income doesn't appear directly on balance sheets because balance sheets show assets and liabilities at a point in time, while income flows over a period.

However, rent you've collected sits in your cash account (an asset), and rent owed to you appears as accounts receivable. The cumulative effect of rental income over time shows up in retained earnings within the equity section. Your income statement tracks rental income, while your balance sheet shows the assets that income created.

What's the difference between market value and book value on a balance sheet?

Book value is what appears on your balance sheet, your property's original cost minus accumulated depreciation. Market value is what your property would sell for today. Balance sheets use book value (also called basis) because it's objective and based on actual costs, not opinions or market fluctuations. For example, you might show a property at $160,000 book value (original $180,000 cost minus $20,000 depreciation) even though market value is $250,000. The market value matters for net worth calculations and refinancing, but balance sheets stick with historical cost.

How do I handle major repairs, balance sheet or expense?

Small repairs and maintenance ($500 or less typically) get expensed immediately on your income statement. Major improvements that extend the property's life or add value get capitalized on the balance sheet as Fixed Assets and depreciated over time. Examples: repainting is an expense; replacing the roof is a capital improvement added to the balance sheet. New appliances, HVAC replacement, and significant renovations all get capitalized. The IRS provides guidance on repairs versus improvements, and your tax professional can advise on borderline cases.

What if my balance sheet doesn't balance?

If total assets don't equal total liabilities plus equity, you've made an accounting error. Common mistakes include forgetting to record security deposits as liabilities, miscalculating depreciation, or failing to account for distributions taken from the business.

Work backwards through recent transactions to find the error. Check that your beginning equity plus current year profit minus distributions equals ending equity. Verify mortgage principal balances match lender statements. Most balance sheet software has built-in checks that flag when totals don't balance.

Can I create one balance sheet for multiple rental properties?

Yes, you can create a consolidated balance sheet showing all properties together. List total cash across all properties, combined accounts receivable, all properties at cost, total accumulated depreciation, all mortgages, and combined equity. However, most landlords also maintain individual balance sheets for each property to track performance separately. This dual approach, individual property balance sheets plus one consolidated view, provides both detailed property-level insights and big-picture portfolio understanding. Software handles this consolidation automatically.

How does Madras Accountancy help rental property owners with balance sheets?

Madras Accountancy provides offshore bookkeeping services specifically for rental property owners and real estate investors. Our team handles daily transaction coding, monthly reconciliations, depreciation calculations, and balance sheet preparation using your property management software. Since 2015, we've supported 200+ U.S. real estate investors, delivering accurate balance sheets monthly at approximately one-third the cost of hiring locally. We work in platforms like QuickBooks, Buildium, and AppFolio, ensuring your balance sheets stay current without consuming your time. Our team also assists with tax preparation support, ensuring your depreciation tracking aligns with IRS requirements.

Do I need separate balance sheets for each LLC?

If you hold different properties in different LLCs, each entity needs its own balance sheet to properly track that entity's financial position and maintain corporate records.

Failing to keep separate balance sheets for separate legal entities can pierce the corporate veil and jeopardize your liability protection. However, you can also create a consolidated personal balance sheet showing your ownership interest across all entities.

Most accounting software handles multi-entity structures, or you can work with professional accounting services to maintain proper entity separation while gaining consolidated visibility.

A rental property balance sheet provides the complete financial picture your income statement can't show, your true equity, accumulated depreciation for taxes, and total assets versus liabilities. While small landlords with 1-2 properties can often skip formal balance sheets, anyone seeking financing, managing multiple properties, or operating through partnerships needs accurate balance sheets updated at least quarterly.

The key is starting simple: use our free template, enter your property's basic information, and track the three main components, assets, liabilities, and equity. As your portfolio grows, consider property management software to automate balance sheet updates, or work with bookkeeping professionals to handle this task while you focus on property operations.

Start creating your rental property balance sheet today using our free template. For landlords managing 3+ properties who want professional support without hiring full-time staff, Madras Accountancy's offshore bookkeeping services provide monthly balance sheet updates and complete rental property accounting at a fraction of local costs.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.