Schedule E is where many individual landlords report rental income and expenses. The form may look simple, but the records behind it need care.

If your rental activity is growing, Schedule E should be supported by clean bookkeeping and clear property records.

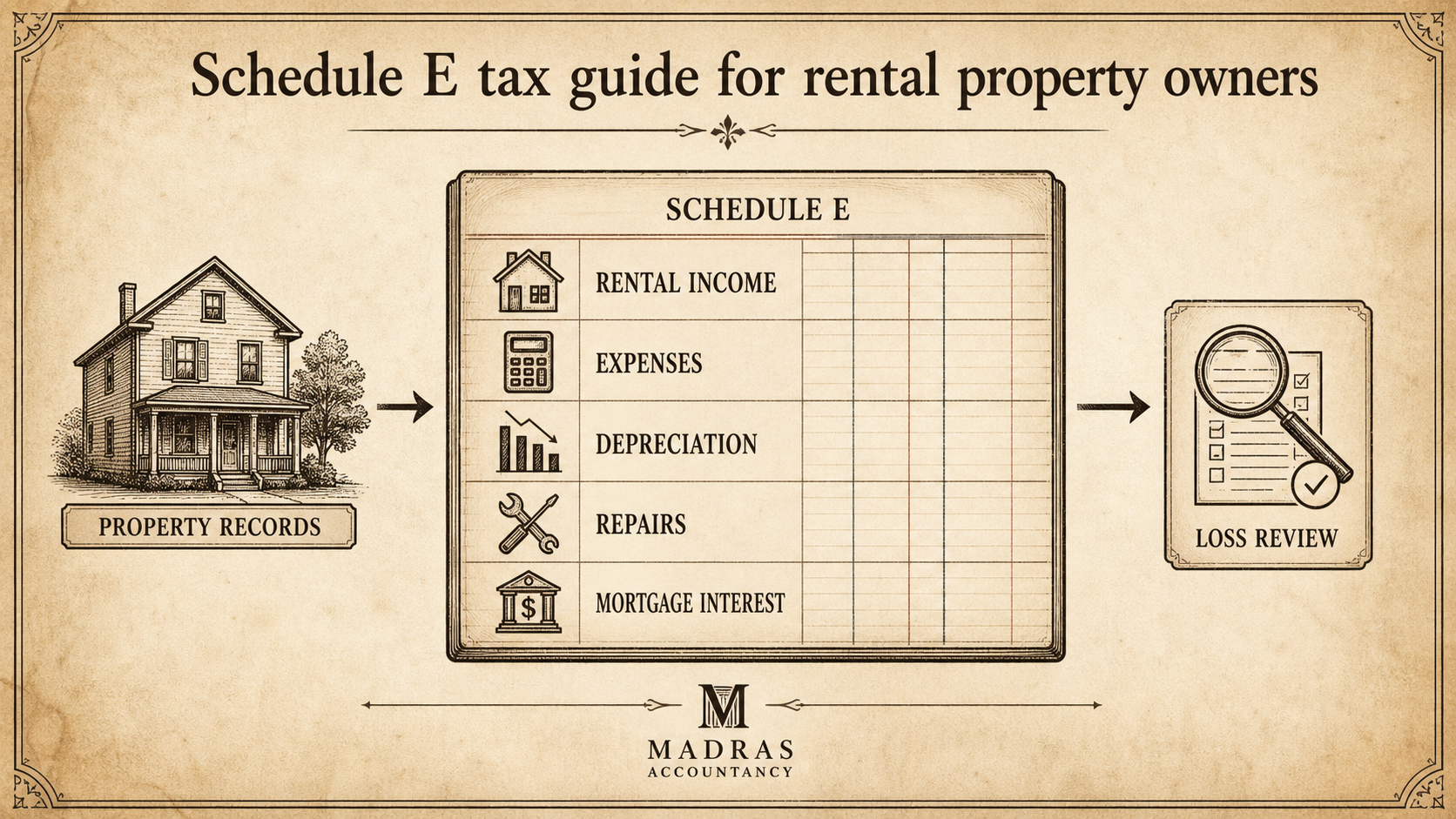

Schedule E reports rental income, expenses, depreciation, and certain losses. Each property may need its own details.

Income can include rent, fees, reimbursements, and other amounts received from tenants. Expenses may include mortgage interest, taxes, insurance, repairs, utilities, management fees, and professional fees.

If you own more than one rental, separate the records by property. This helps show which property earns profit and which one creates losses.

It also makes tax preparation easier. Our accounting and bookkeeping services can help landlords set up property-level records.

Depreciation is a major part of rental property taxes. It can reduce taxable income, but it also needs to be tracked over time.

Keep closing statements, improvement invoices, and prior depreciation schedules. These records may matter when the property is sold.

Some rental losses may be limited by passive activity rules. This is an area where owners should not guess.

Our existing Schedule E rental income and loss guide gives more background.

Schedule E records should separate normal repairs from larger improvements. The tax treatment can be different.

For more detail, see our guide on repairs vs capital improvements.

Get help if you bought or sold property, made major upgrades, have rental losses, own multiple properties, or have messy records.

Our tax preparation and planning services can help review rental filing needs.

Each property should have its own file for lease records, rent reports, repairs, improvements, mortgage statements, insurance, taxes, and management fees. This helps support Schedule E and gives owners a better view of each property.

Good records also help when a property is sold or refinanced.

Before filing, review rent collected, deposits, repairs, improvements, mileage, insurance, taxes, mortgage interest, and depreciation records. Also check whether any tenant reimbursements were received.

This review helps avoid missing income or expenses on Schedule E.

If a property is used personally and rented, the tax reporting may need extra care. Keep calendars, rental records, and expense details clear so the return can reflect the facts.

Use this guide as a monthly review tool, not just a tax-season article. Assign one person to gather records, check open questions, and flag anything that may affect filing, cash flow, or compliance. A simple habit like this keeps small issues from becoming year-end cleanup work.

After reading this, make a short list of the records, deadlines, and open questions tied to this topic. Review that list with your accounting or tax team before the next filing cycle, not after a deadline is already close.

Schedule E works best when rental records are clean. Track income, expenses, depreciation, and each property separately.

If your rental tax records are unclear, contact Madras Accountancy before filing.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.