IRS Publication 527 is the Internal Revenue Service's official guide explaining how to report rental income and expenses for residential rental properties. It covers deductible expenses, depreciation rules, passive activity limitations, and special situations like vacation homes and properties with mixed personal and rental use.

You rent out a property and collect $2,400 monthly. At tax time, you're staring at receipts for repairs, mortgage interest, and property taxes, wondering what you can actually deduct. Publication 527 answers these questions with 50+ pages of rules, examples, and worksheets.

Madras Accountancy has prepared rental property tax returns for 50,000+ property owners since 2015. We've seen landlords lose thousands in deductions simply because they didn't understand what Publication 527 allows. Here's what you need to know.

Publication 527, titled "Residential Rental Property," is the IRS's comprehensive tax reference updated annually. It addresses three property types: full-time rentals with no personal use, vacation homes split between personal and rental use, and properties converted from personal residence to rental.

Chapter 1 covers rental income, what counts, when to report it, advance rent, security deposits, and tenant-paid expenses. Chapter 2 explains deductible expenses: mortgage interest, taxes, insurance, repairs, utilities, and management fees. Chapter 3 details depreciation rules. Chapter 4 tackles passive activity limitations on rental losses.

You must report all rental income when received if you use the cash method (which most landlords do). This includes regular rent, advance rent, lease cancellation payments, and tenant-paid expenses.

Advance rent creates reporting errors. If your tenant pays December plus January and February in advance, you report all three months in December's tax year. The IRS cares when you received money, not the period it covers. Security deposits follow special rules, don't include as income when received if you plan to return them. Report amounts kept for damages or unpaid rent in the year you keep them.

Publication 527 lists dozens of deductible expenses that must be ordinary, necessary, and directly related to rental activity. Mortgage interest, property taxes, insurance premiums, management fees, advertising, legal fees, and utilities all qualify during rental periods.

Repairs versus improvements causes confusion. Repairs maintain current condition (fixing broken windows, patching leaks) and are deducted immediately. Improvements add value or extend life (new roof, HVAC replacement) and must be depreciated over 27.5 years. Understanding which accounting method works best for your rental helps maximize deductions while maintaining proper records.

Depreciation is your most valuable deduction, creating tax benefits without spending additional money. The IRS lets you write off your property's cost over 27.5 years for residential rentals. You recover your investment through annual tax deductions based on three factors: basis (purchase price minus land value), recovery period, and depreciation method.

Start depreciating when you place property in service, when it becomes available for rent, not when you find tenants. The mid-month convention means the IRS assumes you placed property in service mid-month regardless of actual date, affecting first and last year deduction amounts. Detailed guidance on accelerated depreciation options like Section 179 can create larger first-year deductions.

Rent your property for 14 days or fewer per year, and all rental income is tax-free. You don't report it, don't file Schedule E, don't owe taxes on any amount collected. This benefits homeowners near major events, Masters Tournament, Super Bowls, music festivals.

The catch: you can't deduct rental expenses for those 14 days. But you keep 100% of rental income tax-free. Rent your home for $5,000 daily during a special event, collect $70,000 for two weeks without federal income tax. The rule only applies if you also use the property as a residence. Count carefully, day 15 changes everything.

When you use rental property personally and also rent it out, Publication 527 requires dividing expenses between rental and personal use based on days. This determines deductible amounts and affects passive loss limitations.

Calculate rental percentage by dividing rental days by total days used. Rent your vacation home 90 days and use it personally 30 days, you deduct 75% (90/120) of expenses as rental expenses. Properties rented less than 15 days follow the 14-day rule. Properties rented 15+ days with personal use exceeding the greater of 14 days or 10% of rental days qualify as personal residences, limiting rental loss deductions to rental income. Effective financial statement tracking helps separate personal and rental use properly.

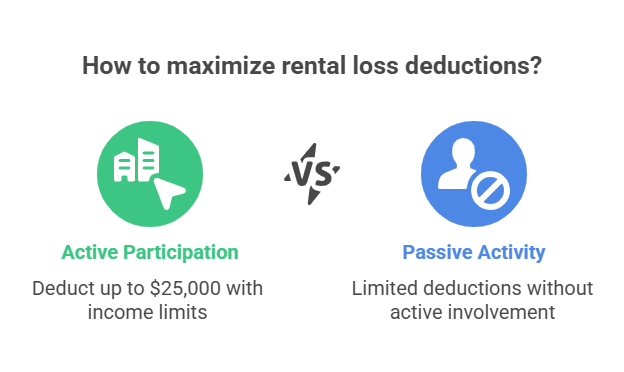

Most rental activities are passive, limiting how much rental losses offset other income. The $25,000 special allowance helps, if you actively participate (make management decisions, approve tenants, decide on repairs), you can deduct up to $25,000 in rental losses against non-passive income. This phases out when modified adjusted gross income exceeds $100,000 and disappears at $150,000.

Real estate professional status eliminates passive loss limitations, but requires 750+ hours annually in real property trades or businesses. Suspended passive losses carry forward to future years when you have passive income or sell the property.

Report rental income and expenses on Schedule E (Form 1040), Part I. List each property with its address, show gross rents received, then subtract deductible expenses line by line: advertising, auto, cleaning, insurance, management fees, mortgage interest, repairs, taxes, utilities, depreciation. The result shows net rental income or loss.

Keep meticulous records supporting all entries: bank statements showing rent deposits, receipts for repairs, mileage logs, and documentation of personal versus rental days. The IRS expects contemporaneous records created during the year. Our comprehensive tax planning and preparation services help property owners maintain proper documentation while maximizing deductions.

Visit IRS.gov/Pub527 to download the current year PDF or read the HTML version online. The IRS updates Publication 527 annually in January with latest tax law changes. You can also order printed copies by calling 800-TAX-FORM (800-829-3676).

Yes, up to $25,000 annually if you actively participate and your modified adjusted gross income is under $100,000. The allowance phases out between $100,000-$150,000. Above $150,000, rental losses are fully passive unless you qualify as a real estate professional.

Yes, if you charge fair market rent. Below-market rates to relatives may limit expense deductions. If you let family stay free, you can't claim rental losses, the IRS treats it as personal use, not rental activity.

All suspended passive losses become deductible when you sell the property in a fully taxable transaction. These losses can offset both the gain from sale and other income, creating significant tax benefits for properties held many years.

Don't report security deposits as income when received if you plan to return them. Include in income only when you keep all or part for damages or unpaid rent. Maintain separate accounting to track deposits, commingling funds makes proving which money represents deposits versus rent difficult during audits.

Maintain lease copies, rent receipts or bank deposits, receipts for all expenses, improvement records with costs and dates, vehicle mileage logs for property-related travel, and calendars showing rental versus personal use days. Keep these for at least three years after filing, or longer if you claimed depreciation.

IRS Publication 527 provides the framework for rental property tax compliance. The difference between repairs and improvements affects immediate versus multi-year deductions. Personal use calculations determine whether you can deduct losses. Proper expense tracking throughout the year ensures you claim every allowable deduction.

Property owners who master Publication 527's rules typically save $3,000-$15,000 annually. The 14-day rule alone can create $10,000-$50,000 in tax-free income. Depreciation deductions reduce taxable income by $7,000-$20,000+ yearly for typical rentals. Read Publication 527 before filing, strategies work best when implemented during the tax year, not discovered in March.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.