Year-end bookkeeping for landlords involves reconciling all bank accounts, verifying rental income and expenses, updating depreciation schedules, organizing tax documents, reviewing accounts receivable and payable, and preparing financial statements before closing the books for the fiscal year. This process ensures accurate tax filing and sets up proper financial tracking for the next year.

December 28th. You're staring at twelve months of rent receipts, repair invoices, and property tax bills. Tax deadline looms, but your books look incomplete.

Madras Accountancy has processed year-end closes for 50,000+ rental properties since 2015. Here's your step-by-step checklist to close your books correctly.

Year-end close finalizes your financial records for the tax year, ensuring every rental transaction is accurately recorded. The IRS requires complete documentation of all rental income and expenses. Without proper procedures, you risk audit penalties and missed deductions.

Properties generate hundreds of transactions annually. Each needs proper classification. Mix up a capital improvement with a repair, and you've lost an immediate deduction. The year-end close also reveals your property's actual profitability after depreciation and adjustments.

Start collecting documents in November. You'll need bank statements for all property accounts, credit card statements, rent rolls, lease agreements, vendor invoices for repairs and services, property tax bills, insurance policies, mortgage statements showing principal and interest, 1099 forms for contractors paid $600+, and utility bills you paid.

Digital organization saves time. Create folders by property, then subfolders by expense category. Scan paper receipts immediately. Lost receipts equal lost deductions, the IRS won't accept "I know I paid for that" without proof.

Reconciliation compares your records against external statements. Start with bank reconciliation, pull December's statement and compare every deposit and withdrawal against your books. Deposits should match rent, security deposits collected, and reimbursements. Withdrawals must tie to invoices or receipts.

Common issues include duplicate payments, uncashed checks, and bank errors. Understanding the difference between cash and accrual accounting helps you reconcile correctly. Credit card reconciliation follows the same process, every charge needs documentation.

December 31st creates timing issues. Record all rent received through December 31st as current-year income, even if it covers January. Advance rent is taxable when received. Security deposits aren't income unless you keep them for damages or unpaid rent.

For cash-basis landlords, you can only deduct expenses paid by December 31st. Prepaid expenses need allocation, pay 12 months insurance in December, but only one month is deductible this year.

Depreciation provides your largest non-cash deduction. Residential rentals depreciate over 27.5 years; appliances and furnishings depreciate faster (5-7 years). Each asset needs its own schedule showing purchase date, cost, useful life, and annual deduction.

Add new assets acquired this year. Remove disposed assets and calculate gain or loss. Our guide to Section 179 and bonus depreciation explains accelerated strategies for qualifying property.

Three core statements show your property's position. The profit and loss statement summarizes rental income and expenses, showing net profit or loss. This feeds into Schedule E on your tax return. The balance sheet shows what you own and owe. The cash flow statement tracks actual cash movement.

Generate these through accounting software or spreadsheets. Review for obvious errors, income too low, expenses that spiked unexpectedly. Knowing how to read financial statements helps spot problems before filing taxes.

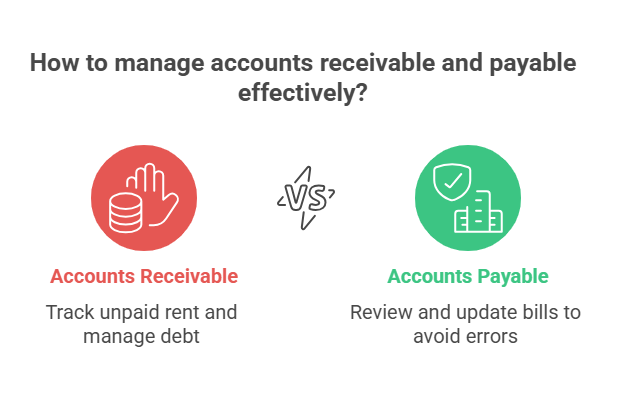

Accounts receivable includes unpaid rent. Generate an aging report showing who owes money and how long it's outstanding. Rent unpaid 90+ days is probably uncollectible, consider writing it off as bad debt with proper documentation.

Accounts payable shows bills you owe. Review your list for accuracy. Remove bills already paid, add December invoices not yet recorded. Accurate payables prevent double-paying vendors in January.

Create a tax folder with Form 1098 mortgage statements, property tax summaries, 1099 forms for contractors paid $600+, and complete rent rolls. Summarize expenses by IRS category matching Schedule E: advertising, auto, cleaning, insurance, management fees, mortgage interest, repairs, taxes, utilities.

Compile your depreciation summary showing all assets and current-year deductions. Professional tax planning and preparation services ensure you maximize deductions while maintaining compliance.

Mixing personal and rental transactions tops the error list. Maintain completely separate accounts for rental activities. Misclassifying repairs as capital improvements (or vice versa) costs money, a $500 fix is a repair, a $25,000 addition needs depreciation.

Forgetting rental property mileage loses thousands. Track every mile for property management, the 2025 rate is 70 cents per mile. Neglecting to document cash expenses creates audit risk. Get signed receipts for all cash payments.

Year-end isn't just looking backward. Review your chart of accounts and add needed categories. Update your budget based on actual results. Schedule quarterly bookkeeping reviews for next year, catching errors in March beats discovering them in December.

Evaluate whether your current system still works. One property in a spreadsheet is fine. Ten properties need proper accounting software. Plan system changes in January.

Expect 4-8 hours per property if you maintained good records throughout the year. Properties with poor bookkeeping can require 20+ hours. Start in early December rather than waiting until year-end to avoid time pressure.

No, security deposits you must return aren't deductible or taxable. Only report security deposits as income when you keep them for damages or unpaid rent. Maintain separate accounting for security deposits.

Reopen the prior year's books, make corrections, and close again. If you filed taxes, determine whether corrections require an amended return. Small errors (under $100) typically don't warrant amendments, but material mistakes need Form 1040-X.

Most landlords use cash-basis accounting, record income when received and expenses when paid. It's simpler than accrual accounting. The IRS allows cash basis for most rental activities unless you're a tax shelter or have gross receipts exceeding $27 million.

Mail 1099-NEC forms to any individual or unincorporated business you paid $600+ for services by January 31st. This includes property managers, handymen, landscapers. Corporations (except attorneys) don't require 1099s. File with IRS by same deadline to avoid $60-$310 per form penalties.

Year-end bookkeeping becomes manageable with systematic process. Start gathering documents in November, reconcile throughout December, finalize adjustments by January 15th. This timing provides breathing room before tax season.

Proper year-end close means maximum deductions, confident tax filing, and audit-ready documentation. You'll know which properties perform well and which drain cash. Start the new year with clean books ready for another cycle.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.