.png)

The accounting profession is experiencing a revolution, and artificial intelligence is leading the charge. If you're an accounting professional wondering whether AI will replace you or help you do your job better, here's some reassuring news: AI in accounting isn't about replacing accountants, it's about making them more powerful, efficient, and strategic than ever before.

Think about how much time you currently spend on repetitive tasks like data entry, invoice processing, or basic reconciliations. Now imagine if those hours could be freed up for higher-value activities like strategic advisory work, complex problem-solving, and building stronger client relationships.

That's exactly what's happening as accounting firms use AI to transform their operations and deliver better results for their clients.

Artificial intelligence is reshaping accounting by automating routine tasks and providing insights that would take humans hours or days to uncover. AI tools can analyze thousands of transactions in minutes, identify patterns and anomalies, and generate reports with accuracy levels that consistently exceed manual processes.

The integration of AI doesn't mean accounting professionals become obsolete. Instead, it elevates their role from data processors to strategic advisors. When AI handles the mundane tasks, accountants can focus on interpreting results, providing guidance, and solving complex business problems that require human judgment and expertise.

This transformation is already happening across accounting firms of all sizes. From solo practitioners to large firms, those who leverage AI are finding they can serve more clients, provide better insights, and build more profitable practices while reducing the stress and burnout associated with repetitive work.

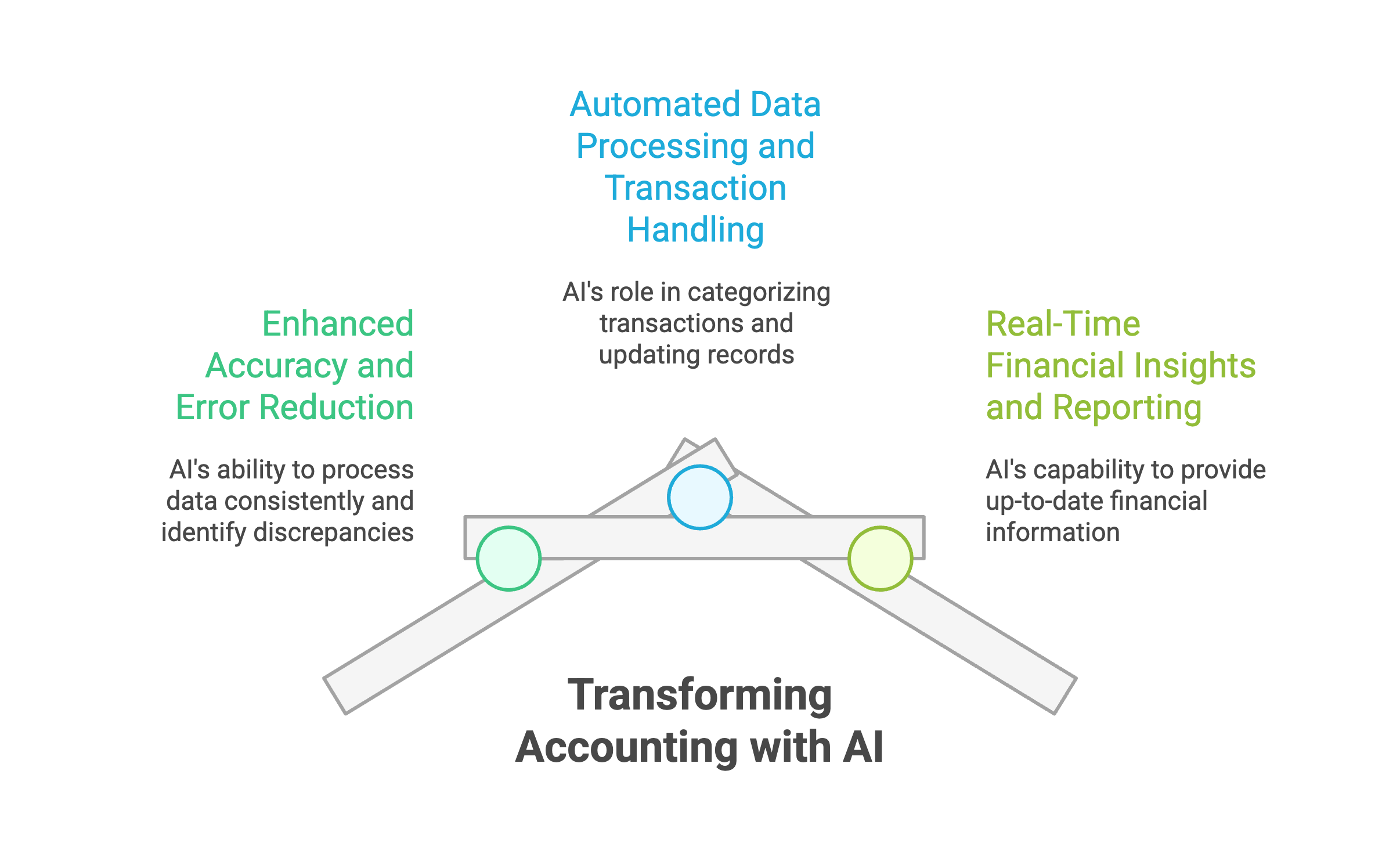

One of the most significant advantages of using AI in accounting is the dramatic improvement in accuracy. AI systems don't get tired, distracted, or make computational errors. They process financial data consistently and can identify discrepancies that human eyes might miss during manual reviews.

AI tools can quickly analyze large datasets and flag unusual transactions or patterns that might indicate errors or fraud. This capability is particularly valuable during audits, where AI can review entire populations of transactions rather than just samples, providing more comprehensive assurance.

The reduction in errors doesn't just improve quality; it also saves significant time that would otherwise be spent on corrections, restatements, and the stress that comes with discovering mistakes after the fact.

Modern AI accounting software can automatically categorize transactions, extract data from invoices and receipts, and update financial records without human intervention. This automation extends to bank reconciliations, expense reporting, and even basic financial statement preparation.

Generative AI tools are particularly powerful for processing unstructured data like contracts, agreements, and correspondence, extracting relevant financial information and integrating it into accounting systems seamlessly.

The time savings from automation are substantial. Tasks that previously took hours can be completed in minutes, allowing accounting professionals to handle larger volumes of work or dedicate more time to analytical and advisory activities.

AI enables real-time financial reporting by continuously processing transactions and updating financial positions as business activities occur. This capability provides business owners and managers with up-to-date insights that support better decision-making.

Traditional accounting often involves waiting until month-end or quarter-end to understand financial performance. AI systems can provide daily or even hourly updates on key metrics, cash flow positions, and performance indicators that matter most to business success.

This real-time capability is particularly valuable for cash flow management, budget monitoring, and identifying trends before they become problems or opportunities before they disappear.

AI can analyze and extract information from various document types including invoices, receipts, contracts, and bank statements. This capability eliminates manual data entry while ensuring consistency and accuracy in how information is captured and categorized.

Optical character recognition (OCR) combined with machine learning allows AI systems to understand context, not just read text. This means they can distinguish between different types of charges, allocate expenses to appropriate accounts, and even identify potential compliance issues.

AI tools can analyze historical financial data to identify trends and predict future performance with remarkable accuracy. This capability helps businesses plan more effectively and make informed decisions about investments, staffing, and strategic initiatives.

Predictive analytics can forecast cash flow needs, identify seasonal patterns, and alert management to potential financial challenges before they become critical. For accounting firms, this adds tremendous value to client relationships by providing forward-looking insights rather than just historical reporting.

AI systems excel at identifying unusual patterns that might indicate fraudulent activity. They can analyze transaction patterns, vendor relationships, and employee behaviors to flag potential risks that would be difficult to detect through manual processes.

The power of AI in fraud detection comes from its ability to process vast amounts of data and identify subtle anomalies that human reviewers might miss. This capability is particularly valuable for larger organizations with complex transaction volumes.

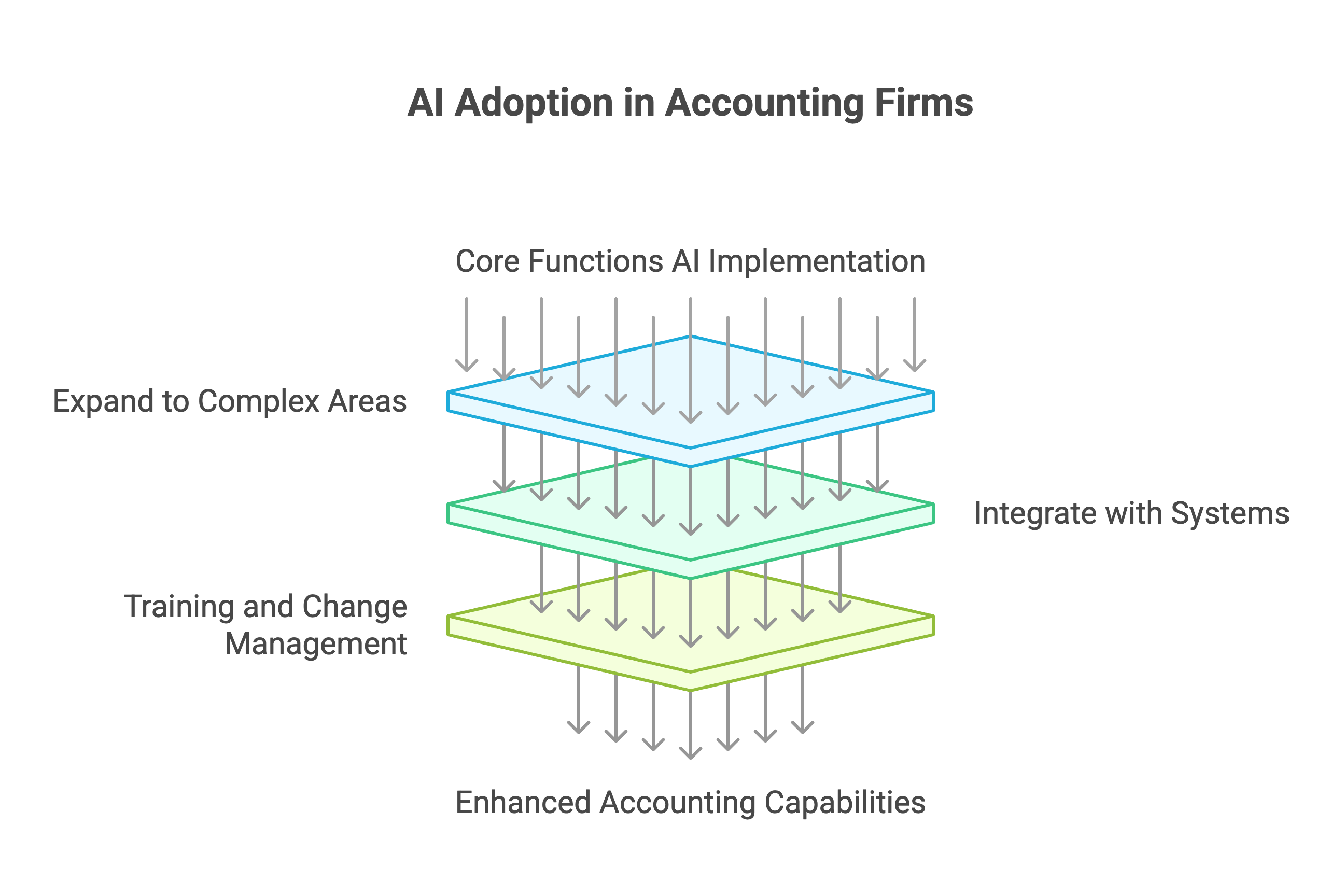

Smaller accounting firms can begin their AI adoption journey by implementing AI tools for basic functions like expense categorization, invoice processing, and bank reconciliations. These applications provide immediate benefits and help teams become comfortable with AI technology.

As comfort and expertise grow, firms can expand AI usage to more complex areas like financial analysis, tax preparation, and audit procedures. This gradual approach allows for proper training and system integration without overwhelming existing workflows.

Modern AI accounting solutions are designed to integrate with popular accounting software platforms. This integration capability means firms don't need to replace their entire technology stack to benefit from AI capabilities.

The key is choosing AI tools that complement existing workflows rather than requiring complete process overhauls. The best implementations enhance current capabilities rather than forcing dramatic changes in how work gets done.

Successfully implementing AI in accounting requires proper training and change management. Team members need to understand how AI tools work, what they can and cannot do, and how to interpret AI-generated results effectively.

The goal is building AI literacy within accounting teams so they can leverage these tools effectively while maintaining professional judgment about results and recommendations.

Modern AI systems designed for accounting applications incorporate robust security measures including encryption, access controls, and audit trails. Reputable providers understand the sensitive nature of financial data and implement appropriate safeguards.

However, it's important to evaluate the security practices of any AI tool provider and ensure they meet your firm's standards for data protection and client confidentiality.

AI excels at processing data and identifying patterns, but professional judgment remains essential for interpreting results and making recommendations. The ethical use of AI requires accountants to understand AI capabilities and limitations while maintaining responsibility for professional decisions.

AI should enhance professional judgment, not replace it. The most effective implementations combine AI processing power with human expertise and ethical reasoning.

While AI tools require investment, the return on investment typically comes through time savings, improved accuracy, and the ability to serve more clients effectively. Many firms find that AI pays for itself within months through increased efficiency and reduced error correction costs.

The key is starting with applications that provide clear, measurable benefits and expanding AI usage as the value becomes evident.

As AI becomes more common in accounting, clients increasingly expect real-time insights, predictive analytics, and proactive advice rather than just historical reporting. Accounting firms that embrace AI are better positioned to meet these evolving expectations.

The firms that thrive in the AI era will be those that use technology to enhance their advisory capabilities and provide more strategic value to their clients.

AI technology continues to evolve rapidly, with new capabilities and applications emerging regularly. Successful accounting professionals and firms will be those that commit to continuous learning and adaptation as AI capabilities expand.

This includes staying current with new AI tools, understanding their applications in accounting, and continuously evaluating how they can improve service delivery and client outcomes.

What are the main benefits of AI in accounting for small firms?

AI helps small accounting firms automate routine tasks like data entry and transaction categorization, improve accuracy, reduce errors, and free up time for higher-value advisory services. This allows smaller firms to compete more effectively and serve more clients efficiently.

How does artificial intelligence improve accuracy in accounting processes?

AI systems process data consistently without fatigue or distraction, reducing computational errors and human oversight mistakes. They can identify patterns and anomalies that humans might miss, leading to more accurate financial records and reporting.

What accounting tasks can AI tools automate effectively?

AI excels at automating data entry, invoice processing, expense categorization, bank reconciliations, transaction matching, basic reporting, and document analysis. These automations typically save 60-80% of the time previously required for manual processing.

Is AI in accounting secure for handling sensitive financial data?

Modern AI accounting solutions incorporate enterprise-grade security measures including encryption, access controls, and audit trails. However, firms should carefully evaluate security practices of any AI provider to ensure they meet professional standards for data protection.

How should accounting firms start implementing AI technologies?

Start with basic applications like expense categorization or invoice processing, choose AI tools that integrate with existing software, provide proper training for staff, and gradually expand usage as comfort and expertise develop. Focus on clear ROI applications first.

Will AI replace accountants or just change their roles?AI enhances rather than replaces accountants by automating routine tasks and enabling focus on strategic advisory work, complex problem-solving, and client relationship building. The accountant's role evolves from data processor to strategic advisor and AI-enhanced professional.

What are the costs associated with adopting AI in accounting practice?

Costs vary widely based on firm size and chosen solutions, typically ranging from $50-500+ monthly per user. However, most firms see positive ROI within 6-12 months through time savings, improved accuracy, and increased capacity to serve clients.

How can accounting professionals prepare for an AI-driven future?

Develop AI literacy by learning about available tools and their capabilities, focus on building advisory and analytical skills that complement AI automation, stay current with technology developments, and embrace continuous learning as AI capabilities expand.

The benefits of AI in accounting extend far beyond simple automation. By embracing artificial intelligence, accounting professionals can transform their practices, deliver greater value to clients, and build more sustainable and profitable businesses. The question isn't whether AI will impact accounting, but rather how quickly and effectively you'll harness its power to enhance your professional capabilities and serve your clients better. The future of accounting is here, and it's powered by the intelligent combination of human expertise and artificial intelligence.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.