QuickBooks has done a brilliant job of convincing the world that accounting software can be friendly. Invoices that don’t look like they were printed in 1997, bank feeds that magically pull in transactions overnight – it’s hard not to be impressed the first time you see it all humming.

But there’s a persistent question underneath that glossy dashboard: if you use QuickBooks, do you still need an accountant? Or are you, in theory, sorted?

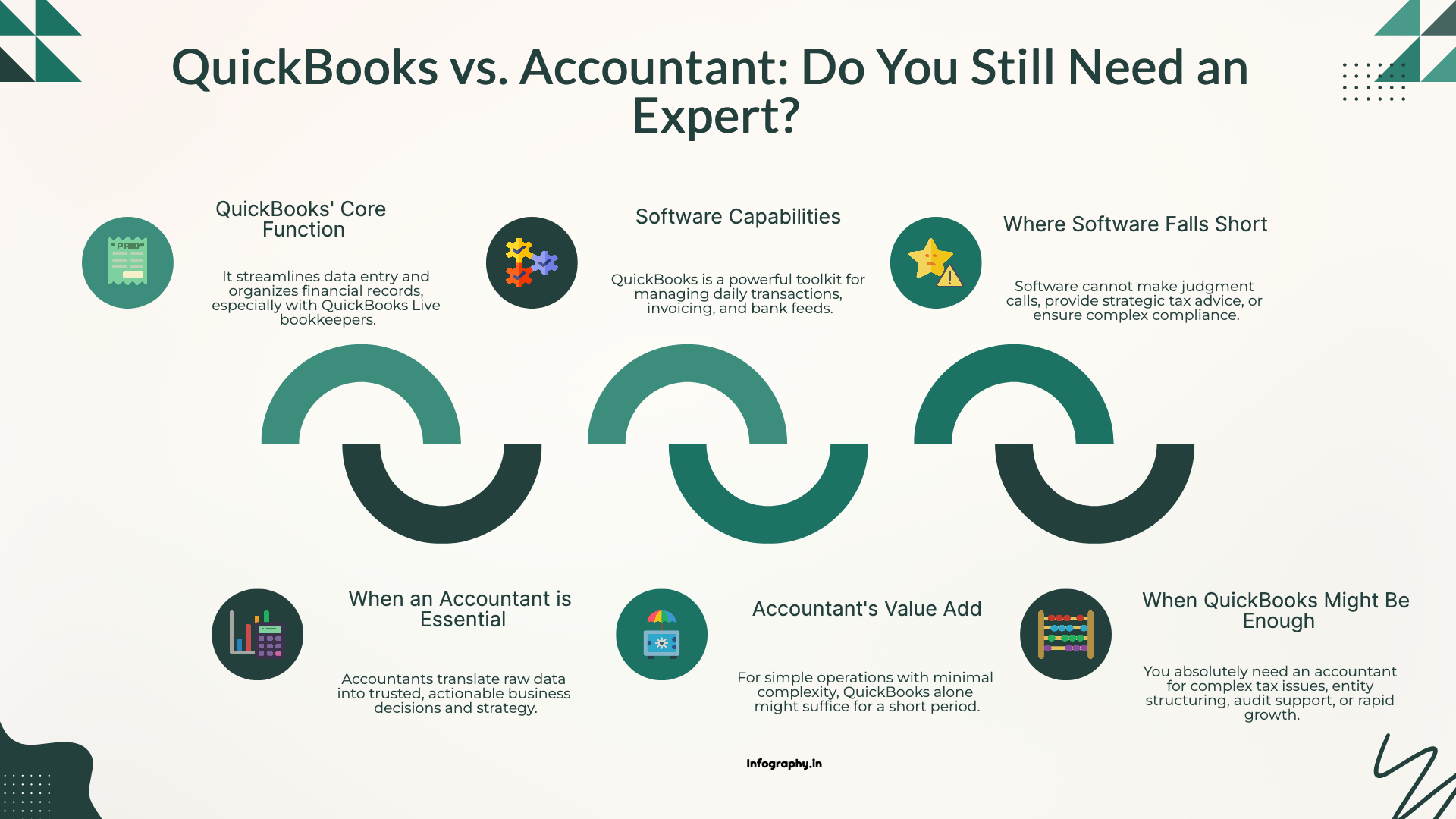

QuickBooks Online is, at heart, a toolkit. A very useful one, granted. It helps you:

With QuickBooks Live, you can even add a remote bookkeeper to keep the data tidy. For many micro-businesses, that’s a huge step up from shoeboxes and spreadsheets.

What QuickBooks doesn’t do – and never pretended to do – is make judgement calls for you. It doesn’t

QuickBooks’ own content gently nudges you toward this reality: they repeatedly recommend working with an accountant for complex tax and compliance matters. The marketing is slick, but the small print is honest.

An accountant – whether that’s a local CPA, a virtual firm, or an offshore-backed team – sits in the space between raw data and real decisions.

They help you answer questions like:

In other words, they turn QuickBooks outputs into something you – and other stakeholders – can trust.

Now zoom out a bit. Many businesses don’t work directly with a single local accountant anymore. They work with a stack:

Madras Accountancy lives in that last category. Their teams are trained on major cloud tools – QuickBooks, Xero, Sage – and plug in beneath CPAs and controllers to handle bookkeeping, close, tax prep, audit support, and even fractional CFO work.

If you imagine your finance function as a theatre, QuickBooks is the stage, your CPA is the director, and Madras is the backstage crew making sure the lights work and the props are in the right place.

There are scenarios where QuickBooks (with or without Live) might carry you for a while:

In those cases, using QuickBooks well and checking in with a tax preparer at year-end may be a rational choice, at least in the short term.

The line gets crossed when complexity shows up. Examples:

At that point, not having an accountant feels a bit like driving a sports car with no dashboard. Technically, the engine still runs. You just can’t see what’s happening until something starts smoking.

So, do you need an accountant if you use QuickBooks? Here’s the awkward but honest answer:

In that second camp, the question stops being “software or accountant?” and becomes “which combination of software, accountant, and possibly offshore team (like Madras Accountancy) gives us reliable numbers and good advice at a cost we can live with?”

QuickBooks is a powerful tool. But it’s still just that: a tool. The real leverage comes from the people who know how to use it, interpret it, and push back when the numbers are quietly trying to tell you something uncomfortable.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.