Direct Answer: Florida rental properties depreciate over 27.5 years using the straight-line method under IRS rules, providing annual deductions equal to your property's cost basis (excluding land) divided by 27.5. A $550,000 rental property with $150,000 in land value generates $14,545 in annual depreciation deductions ($400,000 ÷ 27.5). Bonus depreciation at 60% in 2024 (phasing to 40% in 2025) applies to personal property and qualified improvement property, while cost segregation studies can accelerate deductions by identifying components that depreciate faster than 27.5 years. Florida has no state income tax, so you only benefit federally from these deductions.

A Miami real estate investor called us last month after his CPA told him he was leaving $8,000 annually on the table. He'd owned a $620,000 rental property for three years but never claimed depreciation because "the property was appreciating in value, not depreciating." That misconception cost him $24,000 in unclaimed deductions over three years. Once we explained that tax depreciation is mandatory whether claimed or not, and that the IRS would eventually recapture it upon sale, he filed amended returns to capture those lost deductions.

Florida's zero state income tax makes it attractive for real estate investors, but federal depreciation rules still apply and provide substantial tax savings. Since 2015, we've helped 200+ Florida real estate investors maximize depreciation deductions through proper cost allocation, bonus depreciation strategies, and cost segregation studies. Understanding these rules means the difference between paying unnecessary federal taxes or keeping more cash flow for your next investment.

Depreciation is an annual tax deduction that recovers the cost of income-producing property over its useful life. The IRS considers buildings to wear out over time, even if market value increases. For residential rental properties, the recovery period is 27.5 years using the Modified Accelerated Cost Recovery System (MACRS) with straight-line depreciation. Commercial properties use a 39-year recovery period instead.

You can only depreciate the building's value, not the land. Land never wears out, so it's not depreciable. When you purchase a Florida rental property for $500,000, you must allocate between building and land value. Property tax assessments typically show this split, if the county values the land at $120,000 and improvements at $380,000, you depreciate the $380,000 over 27.5 years, generating $13,818 in annual deductions.

Depreciation begins when the property is "placed in service", the date it's ready and available for rental, not when you actually secure a tenant. Buy a property on March 15th, complete renovations by April 30th, and list it for rent on May 1st? Your placed-in-service date is May 1st. You claim 8 months of depreciation in year one (May through December), not a full year's worth.

The IRS uses mid-month convention, meaning your property is treated as placed in service in the middle of the month regardless of actual date. A property placed in service on May 3rd or May 29th both use mid-month May calculation. This convention affects your first and last years of depreciation, ensuring you claim exactly 27.5 years total over the property's life.

Real example: A Tampa investor buys a duplex for $440,000 with $100,000 allocated to land. His depreciable basis is $340,000. Annual depreciation is $12,364 ($340,000 ÷ 27.5). If placed in service in June, year one depreciation is $7,212 (7/12 of $12,364 for June-December). Each full year thereafter generates the full $12,364 deduction until the final year.

Property must meet four requirements to qualify for depreciation: you must own the property, you must use it in business or income-producing activity, it must have a determinable useful life, and it must be expected to last more than one year. Rental properties clearly meet all four requirements, making depreciation mandatory, not optional.

Residential rental property includes single-family homes, duplexes, condos, townhouses, and apartment buildings where 80%+ of rental income comes from dwelling units. Mixed-use buildings with both residential and commercial space require separate depreciation calculations, residential portions use 27.5 years, commercial portions use 39 years. A building with ground-floor retail and upper-floor apartments splits depreciation between the two recovery periods.

Properties you occasionally use personally don't qualify for full depreciation. Rent your Florida beach condo for 8 months and use it personally for 4 months? You can only depreciate 8/12 of the building's value. Personal use reduces your depreciable basis proportionally. The IRS defines personal use as any day you, your family, or anyone who doesn't pay fair market rent uses the property.

Land improvements like parking lots, sidewalks, fencing, and landscaping depreciate separately from buildings. These have 15-year recovery periods under MACRS. A $30,000 parking lot addition depreciates over 15 years ($2,000 annually), while the building continues on its 27.5-year schedule. Cost segregation studies identify these shorter-lived assets to accelerate deductions.

Personal property inside rental units depreciates even faster, appliances, furniture, and equipment typically use 5-7 year recovery periods. A furnished rental property separates these items from the building structure. $15,000 in furniture and appliances depreciates over 5 years ($3,000 annually) instead of being buried in the building's 27.5-year schedule. This acceleration creates larger early-year deductions.

Bonus depreciation allows immediate expensing of a percentage of qualified property's cost in the first year. The Tax Cuts and Jobs Act (TCJA) temporarily increased bonus depreciation to 100% for property placed in service between September 27, 2017, and December 31, 2022. This percentage is phasing down: 80% in 2023, 60% in 2024, 40% in 2025, 20% in 2026, and zero in 2027 unless Congress extends it.

Buildings themselves don't qualify for bonus depreciation, but personal property and qualified improvement property do. In a rental property, this includes appliances, furniture, carpeting, HVAC systems, security systems, and certain building improvements made after the building was originally placed in service. A $550,000 rental property purchase in 2025 with $40,000 allocated to appliances and furniture allows $16,000 in bonus depreciation (40% of $40,000) in year one.

Qualified improvement property (QIP) became eligible for bonus depreciation through a technical correction in the CARES Act. QIP includes interior improvements to nonresidential buildings made after the building was placed in service: interior walls, HVAC upgrades, fire protection systems, and security systems. However, residential rental property improvements generally don't qualify as QIP, the provision specifically excludes residential properties. This means most Florida rental property improvements follow standard depreciation rules.

The "one big beautiful bill" passed in early 2025 extended several expiring tax provisions but didn't restore 100% bonus depreciation. The phase-down continues as scheduled: 40% for property placed in service in 2025, 20% in 2026, 0% in 2027. Real estate investors should accelerate purchases of depreciable personal property into 2025 to capture 40% bonus depreciation before it drops further. Managing key tax filing deadlines ensures you don't miss opportunities to claim expiring deductions.

Section 179 expensing provides an alternative to bonus depreciation for tangible personal property. You can immediately expense up to $1,220,000 (2025 limit) of qualifying property, though this phases out dollar-for-dollar once total purchases exceed $3,050,000. Most real estate investors use bonus depreciation instead because Section 179 has income limitations, your expensing can't exceed business income, while bonus depreciation has no such limit.

Cost segregation is an engineering-based tax strategy that identifies property components depreciating faster than the building's 27.5-year schedule. Instead of depreciating your entire $400,000 building basis over 27.5 years, a cost segregation study might identify $120,000 in components that depreciate over 5, 7, or 15 years, creating larger immediate deductions and deferring taxes.

The study separates your property into four categories: personal property (5-7 years), land improvements (15 years), building structure (27.5 years), and land (non-depreciable). Engineers and tax professionals examine construction details, blueprints, and property characteristics to allocate costs properly. A typical study costs $5,000-15,000 depending on property complexity and size, but delivers $30,000-100,000+ in accelerated deductions for properties worth $500,000+.

Common reclassified items in Florida rental properties include: specialized electrical wiring for appliances (5 years), decorative lighting fixtures (5 years), carpeting and vinyl flooring (5 years), window treatments (5 years), swimming pools and patios (15 years), parking lots and sidewalks (15 years), landscaping (15 years), and security systems (5 years). A $600,000 property might have $150,000 reclassified from 27.5 years to shorter periods.

Real example: A Fort Lauderdale investor purchases an 8-unit apartment building for $1.2 million ($1 million building, $200,000 land). Without cost segregation, annual depreciation is $36,364. A cost segregation study identifies $300,000 in 5-15 year property. First-year depreciation jumps to $78,000+, creating $40,000+ in additional deductions. This accelerated depreciation increases cash flow and potentially enables another acquisition sooner.

Cost segregation makes sense for properties exceeding $500,000 in value, especially when combined with high current-year income needing offset. Properties under $500,000 often don't justify the study cost unless you own multiple properties that can be studied together at volume discounts. The benefits compound when you're in higher tax brackets, a 37% federal bracket makes every $1,000 in additional depreciation worth $370 in tax savings.

Depreciation recapture taxes you on all claimed (or claimable) depreciation when you sell. If you claimed $100,000 in depreciation deductions over 10 years, the IRS taxes that $100,000 at sale as "unrecaptured Section 1250 gain" at 25% federal rate. This is on top of capital gains taxes on your actual property appreciation. Many investors forget about recapture and get shocked by their tax bill at closing.

The IRS treats depreciation as mandatory, whether you claim it or not. Fail to claim depreciation for five years? When you sell, the IRS assumes you took it and calculates recapture accordingly. This creates a terrible scenario, you lose the annual deductions but still pay recapture tax. Always claim depreciation you're entitled to, because you'll pay recapture taxes regardless.

Florida's zero state income tax means you only pay federal recapture at 25%, unlike states like California (25% federal + 13.3% state = 38.3% combined rate). Buy a Florida rental property for $400,000 (building basis), claim $145,455 in depreciation over 10 years, and sell for $600,000. Your recapture tax is $36,364 (25% of $145,455) plus long-term capital gains tax on the remaining appreciation. Understanding tax planning strategies to minimize capital gains helps structure your sale optimally.

1031 exchanges defer both capital gains and depreciation recapture taxes. Sell your Florida rental property and exchange into a replacement property within IRS timelines (45 days to identify, 180 days to close), and you defer all federal taxes. Florida has no state taxes to defer, making 1031 exchanges purely a federal tax strategy for Florida investors. The deferred depreciation rolls into your new property's basis, continuing the cycle.

Dying with depreciated rental property provides a strategy to eliminate recapture taxes entirely. Your heirs receive a stepped-up basis equal to fair market value at death, erasing all accumulated depreciation and capital gains. A property purchased for $400,000, depreciated to $250,000 basis, and worth $800,000 at death gives heirs an $800,000 basis with zero recapture taxes owed. This strategy requires holding until death and proper estate planning.

Bonus depreciation continues phasing down to 40% in 2025 from 60% in 2024. This affects personal property and qualified improvements but not building depreciation schedules. Real estate investors should accelerate purchases of appliances, furniture, and equipment into 2025 before the rate drops to 20% in 2026. The difference between 40% and 20% bonus depreciation on $50,000 of personal property is $10,000 in first-year deductions, worth $3,700 in federal tax savings at the 37% bracket.

The "one big beautiful bill" extended several expiring provisions but didn't restore 100% bonus depreciation or make it permanent. Congress continues debating various tax extenders, but real estate investors should plan based on current law: 40% in 2025, 20% in 2026, 0% in 2027. Don't count on extensions that haven't passed.

Section 174 research and experimental expenditure rules don't directly affect rental property depreciation but impact real estate developers and investors in certain improvement projects. This mainly affects commercial development rather than residential rental property owners. However, investors who develop properties should understand how R&E rules affect improvement costs.

Interest deduction limitations under Section 163(j) continue affecting larger real estate investors. Business interest deductions are limited to 30% of adjusted taxable income for businesses exceeding $30 million in gross receipts. Most individual Florida rental property owners fall below this threshold and aren't affected. However, large-scale investors and real estate funds need careful tax planning around these limitations.

Standard deduction increases for 2025 ($15,000 single, $30,000 married filing jointly) don't directly affect depreciation but influence whether itemizing makes sense for taxpayers who own rental properties. Rental property depreciation flows through Schedule E regardless of whether you itemize, so these changes don't impact your rental deductions. However, they affect your overall tax picture and planning strategies.

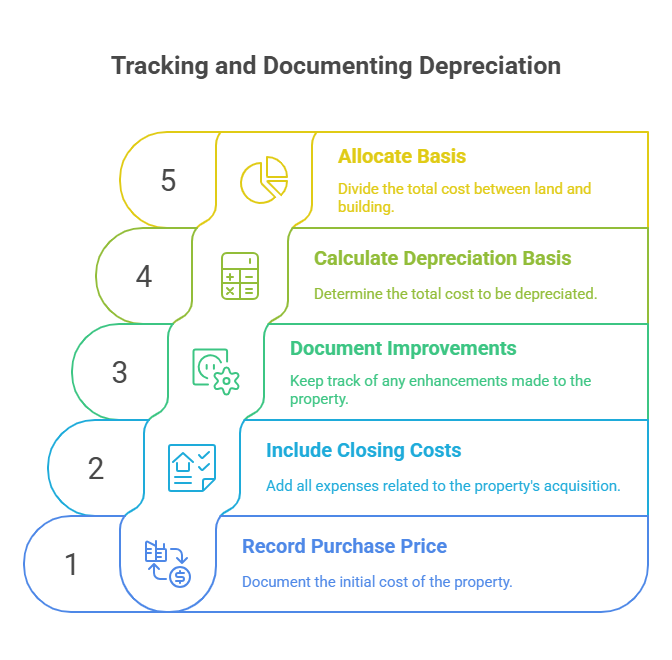

Maintain detailed records of your property's purchase price, closing costs, and all improvements. Your depreciation basis includes purchase price plus acquisition costs like title insurance, recording fees, legal fees, and appraisal costs. A $500,000 purchase with $8,000 in closing costs gives you a $508,000 total basis to allocate between land and building.

Document the land-building allocation using property tax assessments, independent appraisals, or assessed values from county records. Keep these documents with your tax records to support your depreciation calculations during IRS audits. County property appraiser websites in Florida show assessed values split between land and improvements, screenshot or save these pages as documentation.

Track all improvements separately from repairs. Improvements get capitalized and depreciated, while repairs are immediately deductible. Replace a broken air conditioner with a similar unit ($5,000)? That's a repair, deduct immediately. Install a complete HVAC system upgrade ($18,000)? That's an improvement, depreciate over its applicable recovery period. The distinction significantly affects your current-year tax liability. Proper categorization of expenses and understanding financial statement preparation ensures accurate tax reporting.

Use depreciation software or work with tax professionals who specialize in real estate. Manual depreciation calculations become complex with mid-month conventions, partial years, and varying recovery periods for different components. Professional tax software automates these calculations, reducing errors and ensuring you claim maximum legal deductions.

File Form 4562 (Depreciation and Amortization) with your tax return for any year you place property in service or claim depreciation on new acquisitions. This form calculates and reports depreciation amounts, including bonus depreciation and Section 179 expensing. Many investors file returns without Form 4562, missing depreciation deductions entirely or calculating them incorrectly.

The biggest mistake is not claiming depreciation at all. Some investors think depreciation is optional or that they shouldn't claim it if the property is appreciating in market value. Tax depreciation is mandatory, the IRS will recapture it upon sale whether you claimed it or not. Failing to claim depreciation means losing the annual tax benefits but still paying recapture taxes later. Always claim what you're entitled to.

Incorrectly allocating between land and building creates problems. Overallocating to land (non-depreciable) reduces your annual deductions. Underallocating to land and over-depreciating the building triggers IRS scrutiny during audits. Use reasonable allocation methods based on county assessments or independent appraisals. Don't just guess or use arbitrary percentages without documentation.

Missing the placed-in-service date calculation costs investors months of depreciation. The property is placed in service when ready and available for rent, not when a tenant moves in. A property renovated and listed for rent on July 15th begins depreciating in July, even if the first tenant doesn't arrive until September. Claiming only 4 months instead of 6 months loses depreciation you can't recover.

Failing to segregate personal property from building structure wastes acceleration opportunities. Treating $40,000 in appliances and furniture as part of the building's 27.5-year schedule instead of 5-7 year personal property loses thousands in early-year deductions. Cost segregation studies identify these items, but even self-performed segregation (tracking appliance costs separately) provides benefits for smaller properties.

Ignoring improvements made after acquisition creates missed deduction opportunities. Add a $25,000 screened porch to your rental property? That's a separate depreciable improvement with its own placed-in-service date and depreciation schedule. Many investors lump all improvements into their original basis and never properly depreciate post-acquisition additions. Each improvement should be tracked separately with its own Form 4562 entry.

Annual depreciation equals your building's cost basis divided by 27.5 years. A $550,000 property with $150,000 in land value has $400,000 depreciable basis, generating $14,545 annually in depreciation deductions. First and last years are prorated based on your placed-in-service month using mid-month convention. Florida has no state income tax, so depreciation only reduces federal taxes, not state taxes.

No, land is never depreciable because it doesn't wear out. You must allocate your purchase price between land and building using county property tax assessments, appraisals, or other reasonable methods. In Florida, county property appraiser websites show assessed values split between land and improvements. Only the building/improvement portion depreciates over 27.5 years for residential rental property.

Bonus depreciation in 2025 is 40% of qualifying property's cost, down from 60% in 2024. This applies to personal property like appliances and furniture, not the building structure. A $30,000 appliance package qualifies for $12,000 in bonus depreciation (40% of $30,000) in year one, with remaining basis depreciated over 5 years. Buildings themselves use standard 27.5-year straight-line depreciation with no bonus depreciation.

Yes, depreciation is mandatory for tax purposes. Whether you claim it or not, the IRS assumes you did and will charge depreciation recapture tax when you sell. Failing to claim depreciation means losing the annual tax benefits while still paying recapture taxes later. Always claim depreciation you're entitled to, there's no advantage to skipping it.

Cost segregation studies identify property components that depreciate faster than the 27.5-year building schedule. Engineers reclassify items like carpeting, appliances, landscaping, and parking lots to 5-15 year recovery periods. This accelerates deductions into early years. Studies cost $5,000-15,000 but typically generate $30,000-100,000+ in accelerated deductions for properties worth $500,000+, creating substantial immediate tax savings.

You pay depreciation recapture tax at 25% federal rate on all claimed depreciation. If you claimed $100,000 in depreciation over 10 years, you owe $25,000 in recapture tax when you sell, plus capital gains tax on appreciation. Florida has no state income tax, so you only pay federal recapture. You can defer all taxes through a 1031 exchange or eliminate them by holding until death for stepped-up basis.

Yes, cost segregation can be performed retroactively through a "look-back study." You file Form 3115 (Change in Accounting Method) to claim missed depreciation from prior years in your current tax return. This captures all unclaimed accelerated depreciation without amending prior returns. The catch-up adjustment appears as a one-time deduction in the year you file Form 3115, potentially creating a large current-year deduction.

Yes, especially for properties exceeding $300,000 or portfolios with multiple properties. Proper depreciation requires correct basis allocation, placed-in-service calculations, and component segregation. Mistakes cost thousands in lost deductions or trigger IRS audits. Professional tax preparation for real estate investors costs $500-1,500 annually but typically saves 5-10x that amount through proper depreciation optimization, bonus depreciation strategies, and cost segregation recommendations.

Florida rental property depreciation provides substantial federal tax savings through annual deductions that reduce taxable income over 27.5 years. While Florida's zero state income tax means depreciation only benefits you federally, the savings still significantly improve cash flow and investment returns. A $500,000 property generates roughly $15,000-18,000 annually in depreciation deductions, worth $5,500-6,600 in federal tax savings at typical investor brackets.

The keys to maximizing benefits are: properly allocating between land and building at acquisition, claiming depreciation starting the month placed in service, segregating personal property for accelerated deductions, and considering cost segregation studies for properties exceeding $500,000. With bonus depreciation phasing down to 40% in 2025 and 20% in 2026, accelerate personal property purchases while these benefits remain valuable.

Since 2015, Madras Accountancy has helped 200+ Florida real estate investors optimize depreciation strategies, from basic residential rentals to complex commercial properties and multi-state portfolios. If you're managing Florida rental properties and want expert guidance on depreciation maximization, cost segregation analysis, or comprehensive real estate tax planning, our team can help you capture every available deduction while staying fully compliant with IRS requirements.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.