Most trends in the accounting industry are just old problems with new labels. Staffing remains difficult. Clients still demand faster turnaround times. Quality still matters more than marketing promises. But beneath the noise and the buzzwords, a few genuine changes are reshaping how CPA firms think about outsourcing in 2026. These changes show up not in conference presentations, but in the tools providers are building, the workflows firms are implementing, and the expectations clients are setting.

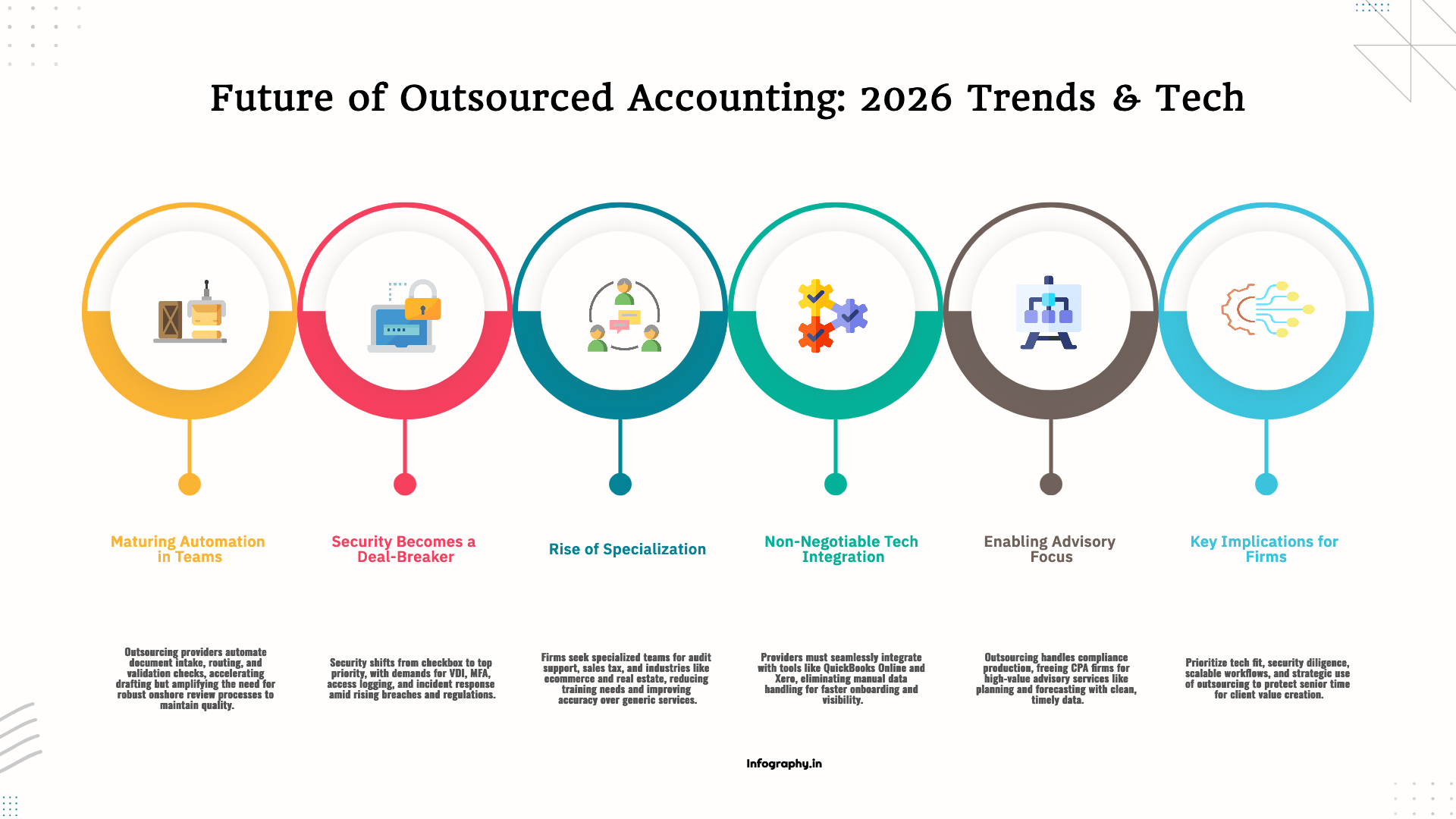

Outsourcing providers are embedding more automation into their workflows for document intake, routing, and routine validation checks. This is not the automation that replaces accountants. It is the automation that handles repetitive tasks like extracting data from PDFs, checking whether all required documents were uploaded, and flagging missing items before work begins. The practical benefit for firms is faster initial drafting and fewer instances of work being returned because a document was missing.

The risk is the same as it has always been with automation. Volume increases. When intake is automated and drafting is faster, the offshore team can produce more deliverables in less time. If the onshore review process does not keep pace, the firm ends up with a larger backlog of work to review and potentially more errors to fix. Automation amplifies the efficiency of the process, but it also amplifies any weaknesses in quality control.

Firms that benefit most from automated outsourcing workflows are those that have already built strong review processes. They know what to look for, they have checklists that guide the review, and they measure rework rates so they can catch quality issues early. Automation makes their good processes better. Firms without strong review processes find that automation just gives them more low-quality work to deal with.

Five years ago, security was a box to check during vendor selection. Does the provider have firewalls? Do they encrypt data? Yes and yes. Good enough. In 2026, security is a primary buying criterion that determines whether a provider is even considered. Clients ask detailed questions about where their data lives and who has access to it. Firms ask providers about virtual desktop infrastructure, access logging, multi-factor authentication, and incident response procedures.

This shift is driven by increasing regulatory scrutiny, higher-profile data breaches, and more sophisticated client awareness. Clients are less willing to accept vague assurances about security. They want to know that their tax returns and financial statements are not sitting on someone's laptop in an unsecured location. Firms are less willing to take on the liability risk of working with providers that cannot demonstrate robust security controls.

Providers that invested in security infrastructure early have a competitive advantage. Those that treated security as an afterthought are losing deals or being forced to make expensive upgrades to meet the new baseline expectations. For firms evaluating providers, security due diligence is no longer optional. It is the first filter, not the last consideration.

General bookkeeping support is widely available and increasingly commoditized. Many providers can handle basic accounts receivable, accounts payable, and bank reconciliations. But more firms are looking for specialized support that understands specific workflows and industry nuances. This demand is pushing providers to develop specialized teams rather than treating all work as generic accounting tasks.

Audit support teams that understand assurance workpapers, testing procedures, and documentation standards are in demand from firms that want to offload fieldwork preparation without sacrificing quality. These teams know how to prepare lead schedules, test samples, and document findings in a format that meets audit standards. This specialization reduces the training burden on the firm and improves the quality of deliverables.

Sales tax teams that can handle multi-state filing calendars, nexus determinations, and rate changes are valuable for firms with clients operating in multiple jurisdictions. Sales tax is complex, and errors are expensive. A specialized team that stays current on rate changes and filing requirements reduces the risk of penalties and client dissatisfaction.

Industry-focused teams for real estate, ecommerce, and professional services bring knowledge of common transactions, chart of account structures, and reporting needs specific to those industries. A team that has worked with dozens of ecommerce clients understands platform integrations, sales channel reconciliations, and inventory accounting in ways that a general bookkeeping team does not. This experience translates into faster onboarding, fewer questions, and higher-quality output.

Firms are less tolerant of manual workarounds and data export-import gymnastics. When they adopt an outsourcing provider, they expect the provider to work inside the same technology stack the firm already uses. QuickBooks Online, Xero, cloud-based document portals, and workflow tracking tools are standard. Providers that require firms to change their tools or manually transfer data between systems are losing deals to competitors that offer native integrations.

This trend is driven by the maturity of cloud-based accounting platforms and the proliferation of workflow management tools. Firms have invested time and money in building their tech stacks, training their staff, and integrating their systems. They do not want to start over just to work with an outsourcing provider. The expectation is that the provider will adapt to the firm's technology, not the other way around.

Providers that build integrations with popular platforms and offer training on how to configure those integrations for different workflows have a competitive advantage. Firms can onboard faster, reduce manual data handling, and maintain visibility into work progress without requiring constant status update meetings.

The shift from compliance-only services to advisory services has been talked about for years, but 2026 is seeing more firms actually make that transition. Outsourcing is one of the key enablers. When the offshore team handles the production layer of compliance work, partners and managers have capacity to focus on planning, forecasting, and strategic conversations with clients.

This is not about outsourcing advisory work. Advisory work stays onshore, handled by CPAs who understand the client's business, industry, and goals. What gets outsourced is the data preparation, financial statement drafting, and workpaper assembly that needs to happen before advisory conversations can occur. Clean, timely financial data is the foundation of advisory work, and outsourcing helps produce that foundation more efficiently.

Firms that successfully make this transition are deliberate about protecting the time that outsourcing frees up. They schedule regular advisory calls with clients, develop standard advisory agendas, and train their staff on how to have advisory conversations. Firms that fail to make this transition simply absorb the freed capacity into more compliance work, and the advisory vision remains aspirational.

Choose providers that can work inside your existing tool stack. Evaluate their integrations, ask for demonstrations of how they handle data sync and workflow tracking, and confirm that their approach minimizes manual workarounds. Technology fit is as important as skill fit.

Demand clear security controls and evidence. Request documentation of their security infrastructure, ask about incident response procedures, and confirm that access controls and logging meet your standards. If a provider cannot provide detailed answers, move on.

Build workflows that scale before you start outsourcing. Create review checklists, document your processes, and standardize your templates. Outsourcing amplifies the quality of your workflows. If your workflows are unclear or inconsistent, outsourcing will amplify that too.

Use outsourcing strategically to protect senior time for review and client work. The goal is not just to reduce costs or fill staffing gaps. The goal is to enable your team to do the work that creates the most value for clients and the firm. If outsourcing does not achieve that, the scope or workflow needs adjustment.

Audit your current workflow for bottlenecks, not just staffing gaps. Identify where work gets stuck, where rework is most common, and where senior staff are spending time on tasks that do not require their expertise. Those are the areas where outsourcing can have the most impact.

Standardize intake packets and review checklists before you start working with a provider. Clear expectations at the front end prevent confusion and quality issues down the road. If you cannot articulate what a good deliverable looks like, the offshore team will struggle to produce it.

Measure the impact of outsourcing on senior capacity, not just on cost savings. Track whether partners and managers are actually spending more time on advisory work, or whether the freed capacity is just getting absorbed by administrative tasks. If the time is not being used strategically, something needs to change.

Trends do not matter if the workflow is unclear. But when the workflow is clear, documented, and well-managed, new tools, better providers, and specialized teams can make the work calmer, faster, and more valuable to clients. That is the real promise of outsourcing in 2026.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.