Rising interest rates can quickly squeeze a company's cash flow and profitability. What was once manageable debt can become a significant burden, while the cost of new capital makes growth more expensive. Businesses that proactively manage their financial strategy can not only weather the storm but also find opportunities. This guide outlines the key steps to protect your business in a high-interest-rate environment.

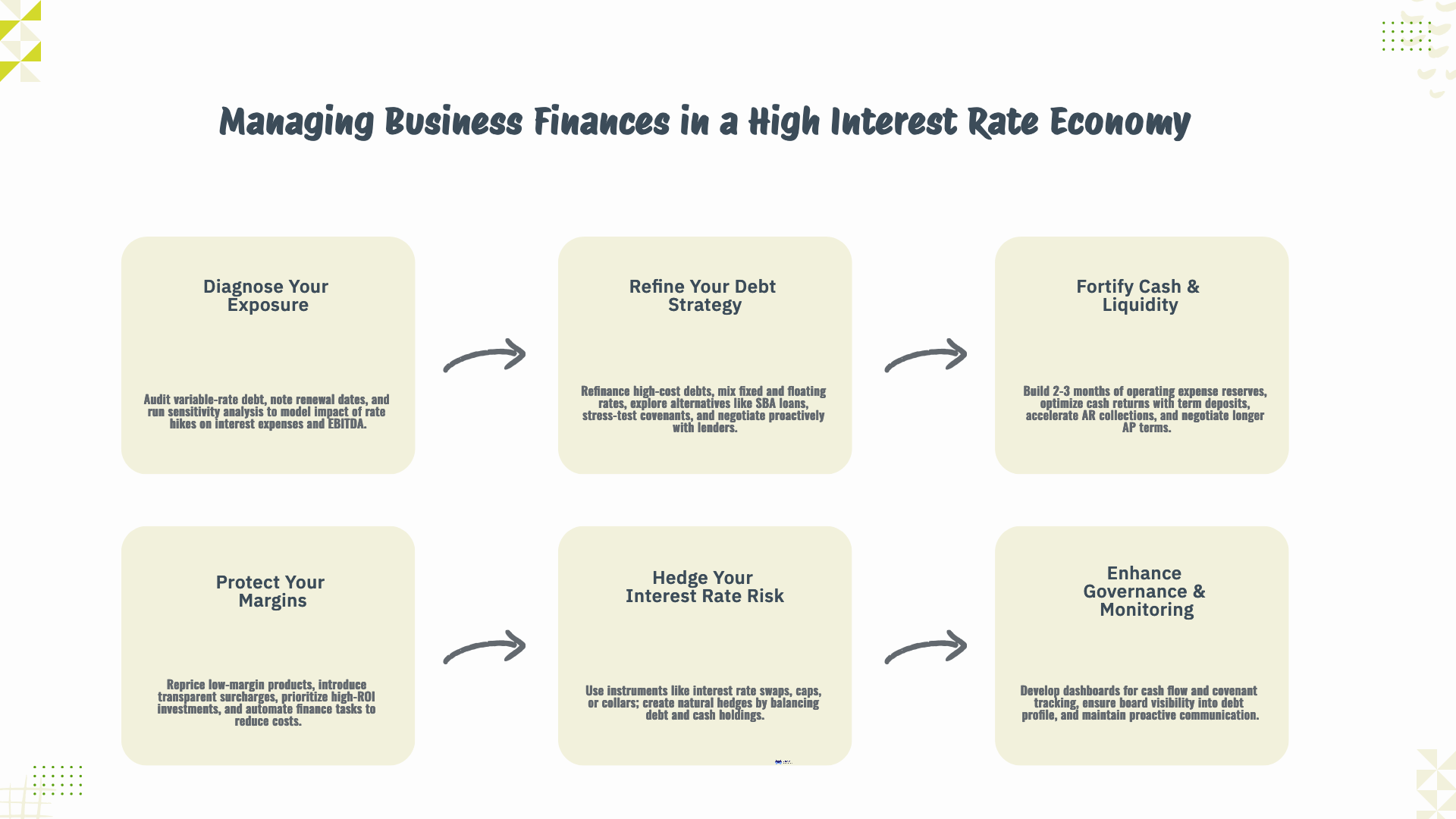

Diagnose Your Exposure

The first step is to understand exactly how vulnerable your business is to rate hikes.

- Audit Your Debt: Create a detailed inventory of all variable-rate debt. Note the current rates, outstanding balances, and, most importantly, the upcoming renewal dates. This will show you when you're most exposed to new, higher rates.

- Run a Sensitivity Analysis: Model the financial impact of potential rate increases. Calculate how a 100, 200, or 300 basis point (1-3%) hike would affect your interest expense and, consequently, your EBITDA. This analysis quantifies your risk and provides a clear picture of what's at stake.

Refine Your Debt Strategy

Once you understand your exposure, you can take steps to mitigate it.

Refinance & Structure

- Consolidate and Refinance: Actively seek opportunities to refinance high-cost, variable-rate debts into more favorable terms.

- Mix Your Debt: Don't rely solely on one type of debt. A healthy structure might include a mix of fixed and floating-rate tranches to balance stability with potential future rate decreases.

- Explore Alternatives: Look into options like SBA loans or asset-based lending, which may offer lower, more stable rates than traditional bank loans.

Protect Your Covenants

- Stress-Test Covenants: Model your covenant headroom (the buffer between your actual performance and the required metrics) under worst-case interest rate scenarios.

- Negotiate Proactively: If you anticipate a breach, talk to your lenders early. You may be able to negotiate cure rights or add equity cushions to provide more flexibility.

Fortify Cash & Liquidity

Cash is your primary defense in a volatile economy.

Build Reserves

- Target a Buffer: Aim to hold cash reserves equivalent to 2–3 months of operating expenses.

- Optimize Returns: Instead of letting cash sit in a low-yield account, ladder term deposits or explore treasury alternatives to earn a better return while maintaining liquidity.

Manage Working Capital

- Accelerate Collections: Tighten your Accounts Receivable (AR) collection processes and consider adjusting payment terms for new customers.

- Optimize Payments: Negotiate longer payment terms (AP days) with your suppliers or explore supplier financing options to improve your cash conversion cycle.

Protect Your Margins

Higher costs must be offset by stronger profitability.

Strategic Pricing

- Review Your Portfolio: Identify and reprice low-margin SKUs or services that are no longer profitable in the current cost environment.

- Be Transparent: If you need to raise prices, consider introducing surcharges for fuel or financing costs. Communicating this with transparency can help maintain customer goodwill.

Strict Cost Discipline

- Prioritize Investments: Scrutinize all expenses and prioritize projects with a clear, positive ROI. Delay non-essential spending.

- Automate to Save: Invest in technology to automate manual finance tasks like invoicing and expense reporting. This reduces administrative overhead and frees up your team for more strategic work.

Hedge Your Interest Rate Risk

For businesses with significant exposure, formal hedging can be a powerful tool.

- Consider Hedging Instruments: Explore financial products like interest rate swaps (to exchange a variable rate for a fixed one), caps (to set a ceiling on your rate), or collars (to confine your rate within a specific range).

- Use Natural Hedges: You can also create "natural" hedges through your financial structure, such as balancing your mix of debt and holding significant cash balances that earn more as rates rise.

Enhance Governance & Monitoring

You can't manage what you don't measure.

- Create Dashboards: Your FP&A team should develop monthly dashboards that track cash flow, interest expenses, and covenant compliance.

- Improve Board Visibility: Ensure your board of directors has clear visibility into your debt profile and upcoming refinancing windows. Proactive communication is key to strategic alignment.

Protect Your Financial Runway

Need help modeling interest sensitivity and refinancing paths? Our fractional CFO team can build scenarios and negotiate lender terms to protect your runway.

%2075-100%20(12).png)

%2075-100%20(9).png)