Most CPA firm owners do not need motivational speeches about improving margins. They need reliable financial analysis they can trust when making decisions. If you run a firm or manage operations, you already know the two pressures that appear every year. Payroll costs climb as you compete for scarce talent in tight labor markets. Clients expect faster turnaround and more responsive service without accepting proportional fee increases. This combination squeezes profitability. Outsourcing can relieve the pressure, but only if the return on investment is real and measurable, not just promised in vendor marketing materials.

This analysis uses concrete numbers with stated assumptions. The goal is to show you how to estimate ROI for your firm's specific situation rather than accepting generic claims about cost savings. Your costs, rates, and efficiency will differ from these examples, but the analytical framework applies universally.

When people claim that outsourcing delivers return on investment, they often blend three distinct benefits without clarifying which they mean. Direct cost savings compared with hiring in-house staff reduce your expense base for equivalent output. Capacity gained means more work gets completed without adding domestic headcount, which improves fixed cost absorption and allows revenue growth. Time reclaimed by seniors and partners can be redirected to billable advisory work and business development, creating revenue opportunities that did not exist when those people were consumed by production tasks.

This analysis focuses primarily on direct cost savings, then demonstrates how capacity gains and time reclamation often follow once the cost foundation is established.

Salary alone is not a complete cost model. The real cost includes salary plus everything that comes with employment: payroll taxes, benefits, workspace, technology, and the hidden costs of recruiting, onboarding, and ongoing management.

A practical framework for estimating fully loaded annual cost includes base salary, payroll taxes and benefits typically calculated as a percentage of salary, software and seat licenses for accounting systems and collaboration tools, and recruiting and onboarding costs spread across the expected tenure. Some firms also include manager review time and rework costs that exist because junior work is never perfect initially, though quantifying these costs requires tracking data many firms do not maintain.

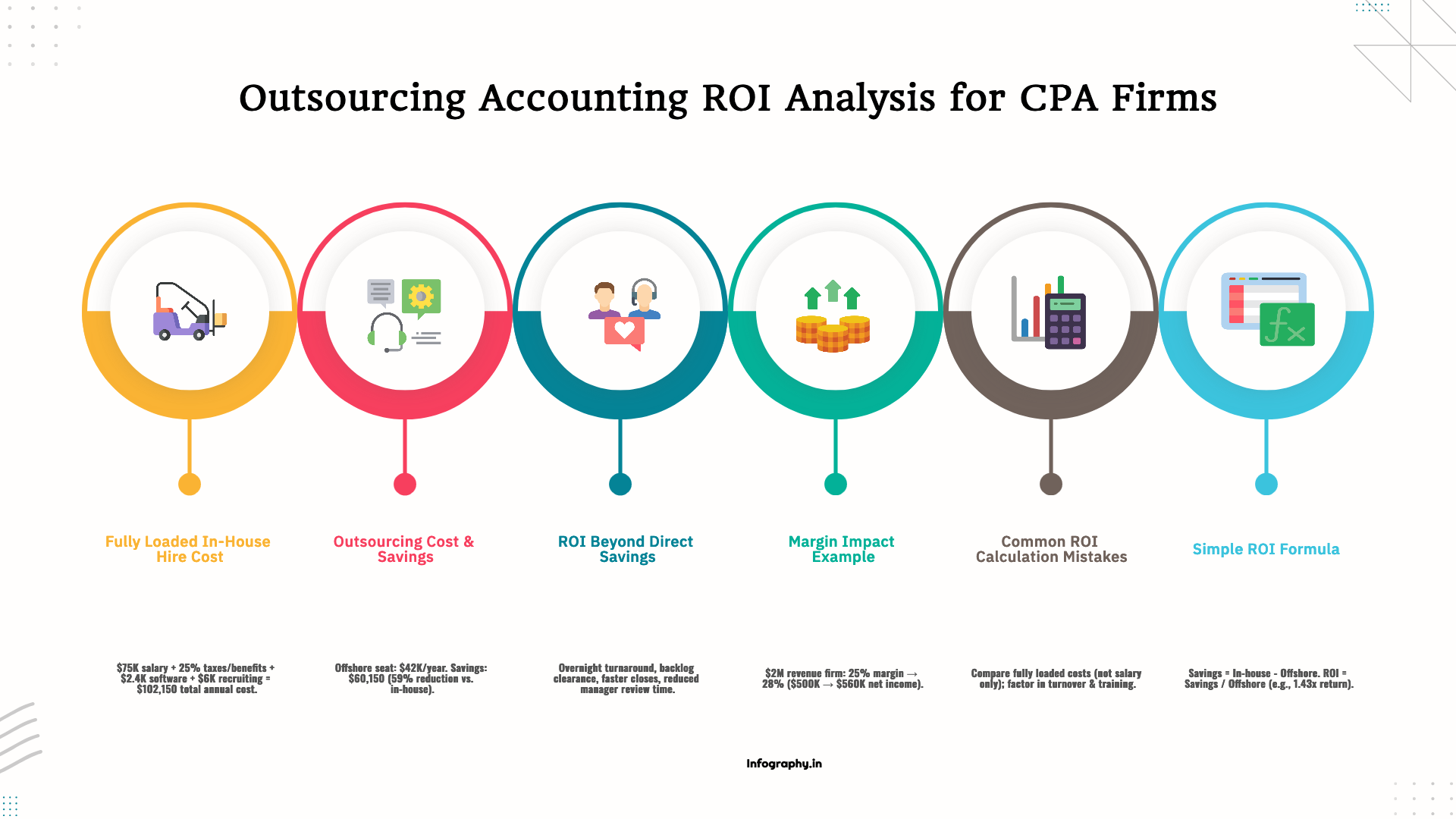

Consider a worked example. A firm hires an experienced staff accountant at seventy-five thousand dollars annual salary. Payroll taxes and benefits add approximately twenty-five percent, or eighteen thousand seven hundred fifty dollars. Software tools and licenses add twenty-four hundred dollars annually. Recruiting and onboarding costs, including job postings, interview time, and training, spread across one year add approximately six thousand dollars.

The fully loaded first-year cost totals one hundred two thousand one hundred fifty dollars. This estimate does not include office space, hardware, or the opportunity cost of partner and manager time spent interviewing and training. If you include those elements, the cost rises further. If you exclude them, the comparison understates the true burden of domestic hiring.

Outsourcing costs vary widely based on scope, experience level, turnaround requirements, and how well your processes are documented. Poorly documented workflows require more provider time for clarification and training, which increases costs. Clear processes with standardized templates reduce the time investment and lower costs.

Most CPA firms structure offshore support with the provider handling draft preparation and the in-house team performing review and sign-off. This model maintains quality control where it belongs while shifting time-intensive production work to a lower cost base. Pricing for this model typically falls substantially below domestic hiring costs for equivalent output.

Industry discussions suggest offshore costs are often thirty to fifty percent lower than hiring domestic staff with comparable skills. This range is an estimate based on comparing offshore provider fees to fully loaded domestic employment costs, not just salary. The specific savings depend on what you are comparing, the provider's pricing model, and the complexity of work being delegated.

Using a worked example, assume an offshore accounting seat costs forty-two thousand dollars annually for a dedicated resource performing bookkeeping, reconciliations, and tax workpaper preparation. Compare this to the one hundred two thousand one hundred fifty dollar fully loaded cost of the domestic hire calculated above. The estimated annual savings are sixty thousand one hundred fifty dollars. The estimated savings rate is approximately fifty-nine percent.

This is not a guarantee. It is a calculation based on specific assumptions. Change the salary, the burden rate, or the offshore pricing, and the result changes. The analytical approach remains valid even as inputs vary.

Some firms evaluate outsourcing and conclude that the hourly cost is not dramatically different from what they pay domestic contractors. This can happen when comparing specialized offshore roles to part-time domestic arrangements. Even in these cases, return on investment can appear through operational improvements rather than pure wage arbitrage.

Work progresses overnight because of time zone handoffs, compressing turnaround from two business days to twenty-four hours. Clients receive deliverables faster, which strengthens satisfaction and retention. Faster cycle times also allow the firm to handle higher volume without increasing headcount.

Backlogs get cleared once offshore capacity is added. The accumulated work that has been causing close delays and deadline slippage finally gets processed. Once the backlog clears, monthly close timelines improve from day eighteen to day ten, freeing onshore capacity that was previously consumed by catching up.

Manager review time decreases when offshore teams follow standardized checklists consistently. Review of standardized work is faster than review of work that varies in format and completeness. This time savings multiplies across every engagement and allows managers to handle more review volume or redirect time to client advisory work.

These operational gains create value even when direct cost savings are modest. The question is whether your firm has the discipline to measure and capture these benefits rather than letting them dissipate into unstructured activity.

Consider a small firm with two million dollars in annual revenue operating at a twenty-five percent net margin, which translates to five hundred thousand dollars in net income. The firm faces capacity constraints and is considering whether to hire another domestic staff accountant or implement offshore support.

If the firm replaces one planned domestic hire that would cost one hundred two thousand one hundred fifty dollars fully loaded with an offshore seat at forty-two thousand dollars, the net income increases by approximately sixty thousand one hundred fifty dollars, assuming other costs remain constant.

The new net income becomes five hundred sixty thousand one hundred fifty dollars. The new net margin calculates as twenty-eight percent. This three percentage point margin improvement is significant for a small firm. It can fund partner compensation increases, staff bonuses, technology investments, or pricing flexibility that wins competitive bids.

Comparing outsourcing costs to salary alone rather than fully loaded employment costs understates the savings. If you compare a forty-two thousand dollar offshore seat to a seventy-five thousand dollar salary, the calculated savings are thirty-three thousand dollars. If you compare to the fully loaded cost of one hundred two thousand dollars, the savings increase to sixty thousand dollars. Both comparisons can be mathematically correct, but only the fully loaded comparison reflects the real economic benefit to the firm.

Ignoring turnover costs misses a significant expense that outsourcing can reduce. Staff turnover disrupts client work, requires hiring cycles, demands training time from seniors and managers, and creates periods of reduced capacity while positions are vacant. If outsourcing reduces turnover by making workloads more manageable, these savings are real even though they do not appear clearly in annual cost comparisons.

Use this framework to estimate ROI with your firm's actual numbers. Calculate in-house fully loaded annual cost as salary multiplied by one plus your burden rate for taxes and benefits, plus annual software and tools costs, plus estimated recruiting and training costs. Calculate offshore annual cost as the monthly retainer multiplied by twelve or the annual contract value. Estimated savings equal in-house cost minus offshore cost. Estimated ROI equals estimated savings divided by offshore cost.

Using the worked example numbers, in-house cost is one hundred two thousand one hundred fifty dollars, offshore cost is forty-two thousand dollars, savings are sixty thousand one hundred fifty dollars, and ROI is 1.43, meaning each dollar spent on offshore support returns $1.43 in direct cost savings under these assumptions.

Outsourcing can fail to produce ROI even when the cost structure looks favorable if work is poorly scoped or managed. The disciplines required to capture the value are straightforward but require execution.

Start with tasks that have clear inputs and outputs. Bookkeeping cleanup, reconciliations, accounts payable processing, and financial statement drafting are common choices because quality can be verified quickly and objectively. Avoid starting with ambiguous work that requires extensive judgment or client interaction.

Document procedures in writing, preferably as checklists. If the firm does not have a month-end close checklist, build one. If procedures exist but are inconsistent, standardize them. Written procedures are essential for training, quality control, and consistent output.

Define what done means for each deliverable type. If a reconciled bank account requires supporting documentation attached, specify that. If an adjusting entry needs an explanatory note, document that requirement. Clear definitions reduce review cycles and rework that consume the time savings outsourcing was supposed to create.

Pick one workflow to outsource initially, not five. Focus creates clarity and allows you to measure results accurately. Build a simple cost model using your actual burden rate, tool costs, and recruiting expenses. Set a specific target metric for the first month, whether that is closing five days faster, clearing three months of backlog, or reducing manager cleanup time by ten hours per month. Review results after thirty days and decide whether to expand scope based on actual performance data rather than assumptions.

If the financial analysis shows positive ROI and the workflow delivers the operational improvements, the margin impact follows. The benefit appears quietly in improved profitability, reduced overtime costs, and freed partner capacity for revenue-generating activities. That is how outsourcing boosts the bottom line when implemented with discipline and measured honestly.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.