Publication 946 is the IRS's comprehensive guide that explains how businesses and property owners can recover the cost of business or income-producing property through depreciation deductions. For 2025, the maximum Section 179 expense deduction is $1,250,000, and bonus depreciation has dropped to 40% for most qualifying property. This publication provides the framework for calculating depreciation using the Modified Accelerated Cost Recovery System (MACRS) and helps you maximize tax savings while staying compliant with IRS regulations.

IRS Publication 946, titled "How to Depreciate Property," is your authoritative resource for understanding depreciation rules. Depreciation lets you recover the cost of business assets over their useful life, reducing your taxable income year after year.

Think of it this way: when you buy a $50,000 delivery truck for your business, you don't take the full deduction in year one. Instead, you spread that cost over the truck's useful life, typically 5-7 years. This matches the expense with the years you actually use the asset.

The publication covers three main deduction methods: regular MACRS depreciation, the Section 179 deduction, and the special depreciation allowance (bonus depreciation). Each method has different rules, limits, and strategic advantages depending on your business situation.

The tax landscape has shifted significantly. The Section 179 deduction limit increased to $1,250,000 for tax years beginning in 2025, up from $1,220,000 in 2024. The phase-out threshold also rose to $3,130,000. However, bonus depreciation continues its scheduled phase-down, dropping to 40% for qualified property placed in service during 2025.

CPA firms working with business clients need to stay current on these changes. Many accounting practices outsource complex depreciation calculations to offshore accounting teams to ensure accuracy and compliance with the latest IRS regulations.

Not everything qualifies for depreciation deductions. The IRS requires property to meet specific tests before you can claim depreciation.

The Three Qualifying Tests:

Depreciable Property Includes:

Non-Depreciable Property:

Most accounting firms encounter complex depreciation scenarios with rental properties requiring specialized tax treatment. Understanding these distinctions prevents costly errors during tax season.

The Section 179 deduction lets you expense qualifying property immediately rather than depreciating it over several years. This is your most powerful tool for upfront tax savings.

For 2025, you can deduct up to $1,250,000 on qualifying property placed in service during the tax year. However, this deduction begins phasing out dollar-for-dollar once your total equipment purchases exceed $3,130,000. If you buy $3,500,000 in qualifying property, your Section 179 limit drops to $880,000.

Qualifying Property for Section 179:

Income Limitation Rule: Your total Section 179 deduction cannot exceed your business's taxable income for the year. If your deduction exceeds your income, you must carry the excess forward to future tax years. This rule prevents businesses from creating losses through equipment purchases alone.

The actual Section 179 deduction you claim depends on your specific situation. Understanding when to elect the Section 179 deduction versus taking regular depreciation requires analyzing your current-year income, expected future profits, and overall tax strategy.

MACRS is the standard depreciation method for most business property placed in service after 1986. Publication 946 dedicates several chapters to explaining how this system works.

MACRS operates under two systems: the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). Most property falls under GDS, which uses shorter recovery periods and accelerated depreciation methods.

Common Recovery Periods Under GDS:

When ADS Applies: You must use the Alternative Depreciation System for property used predominantly outside the United States, tax-exempt use property, and property financed with tax-exempt bonds. ADS uses longer recovery periods and the straight-line method, resulting in smaller annual deductions.

The year you place the property in service matters significantly. MACRS applies a half-year convention for most property, assuming you placed it in service at the midpoint of the year regardless of the actual date. For real property, a mid-month convention applies.

The special depreciation allowance, commonly called bonus depreciation, allows an additional first-year deduction for qualified property. For property placed in service in 2025, you can claim a 40% bonus depreciation on the property's adjusted basis.

This represents a significant decline from previous years. The rate was 100% through 2022, dropped to 80% for 2023, 60% for 2024, and now 40% for 2025. It continues falling to 20% in 2026 before expiring completely in 2027 under current law.

Property Must Meet These Requirements:

You can claim a special depreciation allowance on qualifying property without dollar limits, unlike Section 179. However, you cannot claim a section 179 deduction and bonus depreciation on the same property basis, Section 179 reduces basis first, then bonus depreciation applies to the remaining amount.

Businesses navigating complex depreciation scenarios often benefit from fractional CFO services that provide strategic tax planning guidance to maximize available deductions.

Calculating depreciation involves several steps outlined in Publication 946. Here's the process most businesses follow:

Step 1: Determine Your Basis Your basis is typically the property's cost, including the purchase price, sales tax, freight charges, installation, and testing fees. For property received in an exchange, inherited, or gifted, special basis rules apply.

Step 2: Choose Your Recovery Period Use the property class tables in Pub 946 to determine how many years you'll depreciate the asset. A delivery truck falls into the 5-year property class, while a commercial building uses a 39-year recovery period.

Step 3: Determine Your Depreciation Method Most businesses use MACRS with the 200% declining balance method for 3-, 5-, 7-, and 10-year property. For 15- and 20-year property, use 150% declining balance. Residential rental property and nonresidential real property use straight-line depreciation.

Step 4: Apply the Applicable Convention The half-year convention applies to most property, treating all property as placed in service at the year's midpoint. Real property uses a mid-month convention. A mid-quarter convention applies if you place more than 40% of your property in service during the final quarter.

Step 5: Use the Depreciation Tables Publication 946 includes extensive tables showing the depreciation percentage for each year of an asset's recovery period. These tables incorporate the depreciation method and convention automatically.

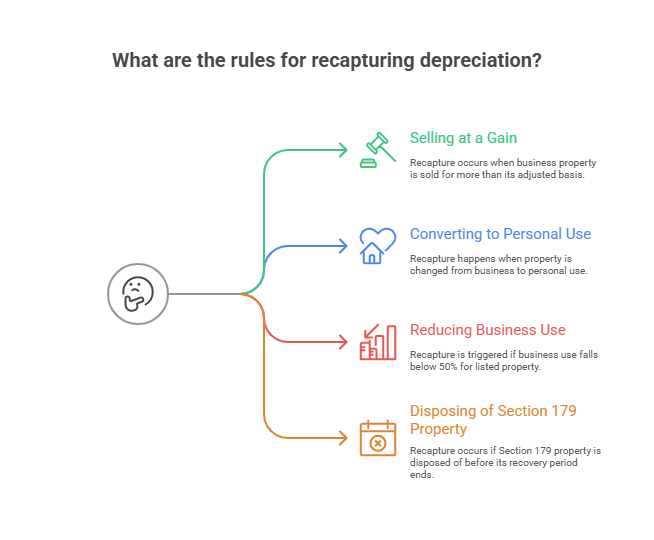

When you sell or dispose of depreciated property, you may need to recapture some or all of the depreciation you claimed. Publication 946 explains the rules for recapturing depreciation in Chapter 3, with additional details on recapturing excess depreciation in Chapter 5.

Depreciation recapture treats your gain as ordinary income up to the amount of depreciation you previously deducted. This prevents you from converting ordinary deductions into lower-taxed capital gains.

Common Recapture Situations:

The recapture rules become especially complex with rental properties requiring careful tracking of all depreciation deductions. If you claimed depreciation on residential rental property, the portion of gain equal to depreciation gets taxed at a maximum 25% rate rather than the regular capital gains rate.

Listed property refers to certain types of property with high potential for personal use. Publication 946 imposes additional recordkeeping requirements and restrictions on these assets.

Property Classified as Listed Property:

For listed property, you can only use accelerated depreciation (including Section 179 and bonus depreciation) if you use the property more than 50% for qualified business purposes. If business use drops to 50% or less in a later year, you must recapture the excess depreciation and switch to the straight-line method.

You must maintain detailed records showing the amount of each business and personal use, the date of the use, and the business purpose for each use. Most businesses find that maintaining proper accounting records for depreciation and tax compliance requires either dedicated staff or outsourced accounting support.

Real property depreciation follows special rules outlined in Publication 946. Residential rental property uses a 27.5-year recovery period, while commercial property depreciates over 39 years.

You can only depreciate the building itself, not the land. When you purchase rental property, you must allocate the purchase price between land and building based on their relative fair market values. Many buyers use the property tax assessment as a reasonable allocation method.

Key Points for Rental Property Depreciation:

If you convert personal property to rental use (like renting out your former residence), your depreciable basis is the lesser of the property's adjusted basis or fair market value on the conversion date. This prevents you from depreciating any decline in value that occurred during personal use.

What is the difference between Section 179 and bonus depreciation?

Section 179 lets you immediately deduct up to $1,250,000 of qualifying property in 2025, but it's limited by your taxable income and phases out if you buy more than $3,130,000 in assets. Bonus depreciation has no dollar limit and allows a 40% first-year deduction in 2025 for qualifying property regardless of how much you purchase or your income level. Section 179 reduces your basis first, then bonus depreciation applies to what remains.

Can I use Publication 946 depreciation methods for personal property?

No. Depreciation only applies to property used in a business or income-producing activity. You cannot depreciate property you use purely for personal purposes, even if it wears out or loses value. However, if you use property for both business and personal purposes, you can depreciate the business-use percentage.

What happens if I don't claim depreciation on qualifying property?

Even if you don't claim depreciation deductions on eligible property, the IRS considers the depreciation as "allowed or allowable" when you sell the asset. This means you must reduce your basis by the depreciation you could have claimed, potentially increasing your taxable gain. To correct missed depreciation, file Form 3115 to change your accounting method.

How does Publication 946 explain what property qualifies for Section 179?

Pub 946 defines qualifying property as tangible personal property used actively in your trade or business, including machinery, equipment, furniture, and certain vehicles. Off-the-shelf computer software also qualifies, along with qualified improvement property like HVAC systems, fire protection, and security systems added to nonresidential buildings. Most buildings themselves don't qualify, nor does property used outside the U.S. or property you inherit.

Can you deduct under Section 179 and also claim bonus depreciation on the same property?

Yes, but Section 179 reduces your basis first. For example, if you buy a $100,000 machine, claim $50,000 under Section 179, and elect bonus depreciation, you'll get 40% bonus depreciation on the remaining $50,000 basis. This stacking strategy maximizes your first-year deductions, though it leaves less basis for regular MACRS depreciation in future years.

What is the cost of qualifying property for Section 179 purposes?

The cost includes the property's purchase price plus any amounts you paid to get the property ready for use. This includes delivery charges, installation fees, sales tax, and testing costs. However, you reduce the cost by any Section 179 recapture from prior years before calculating your current-year deduction.

Do I need IRS approval to change my depreciation method?

For most depreciation method changes, you must file Form 3115, Application for Change in Accounting Method. However, Publication 946 explains that certain changes receive automatic consent without IRS approval by filing the appropriate form with your tax return. Examples include changing from an incorrect to a correct recovery period or changing to the straight-line method for property.

How does Publication 946 treat compliance with IRS regulations for depreciation?

The publication emphasizes accurate recordkeeping as essential for compliance with IRS regulations. You must maintain records showing the property's cost, the date you placed the property in service, the recovery period, the depreciation method used, and the depreciation deduction claimed each year. For listed property, you need detailed logs proving business use percentages. Proper compliance protects you during audits and ensures you don't miss available deductions.

Complex depreciation calculations, Section 179 elections, and bonus depreciation strategies require careful analysis and precise execution. Since 2015, Madras Accountancy has helped over 200 U.S. CPA firms navigate complicated tax scenarios through our offshore accounting partnership model.

Our team stays current with every Publication 946 update and IRS regulation change. We process 50,000+ tax returns annually, maintaining a 98% same-day error resolution rate while reducing client overhead by 40%.

Whether you need support with depreciation schedules, tax preparation, or fractional CFO services, our expertise ensures your business maximizes every available deduction while maintaining full compliance with IRS regulations.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.