The quality concern about outsourcing is legitimate. When a client is upset about errors in their financial statements or tax return, they do not care where the work was performed. They care that it was wrong, that it wasted their time, and that it damaged their trust in your firm. Quality problems are quality problems regardless of geography. Outsourcing does not inherently lower quality, but it can if the firm treats it like a shortcut rather than a structured workflow with appropriate controls and review processes.

Quality in outsourced accounting comes from the same sources as quality in onshore work: clear standards, documented procedures, systematic review, and continuous improvement based on error tracking. The difference is that outsourcing requires making these elements more explicit because the team is remote, the work crosses time zones, and verbal clarifications are less practical than in-person supervision.

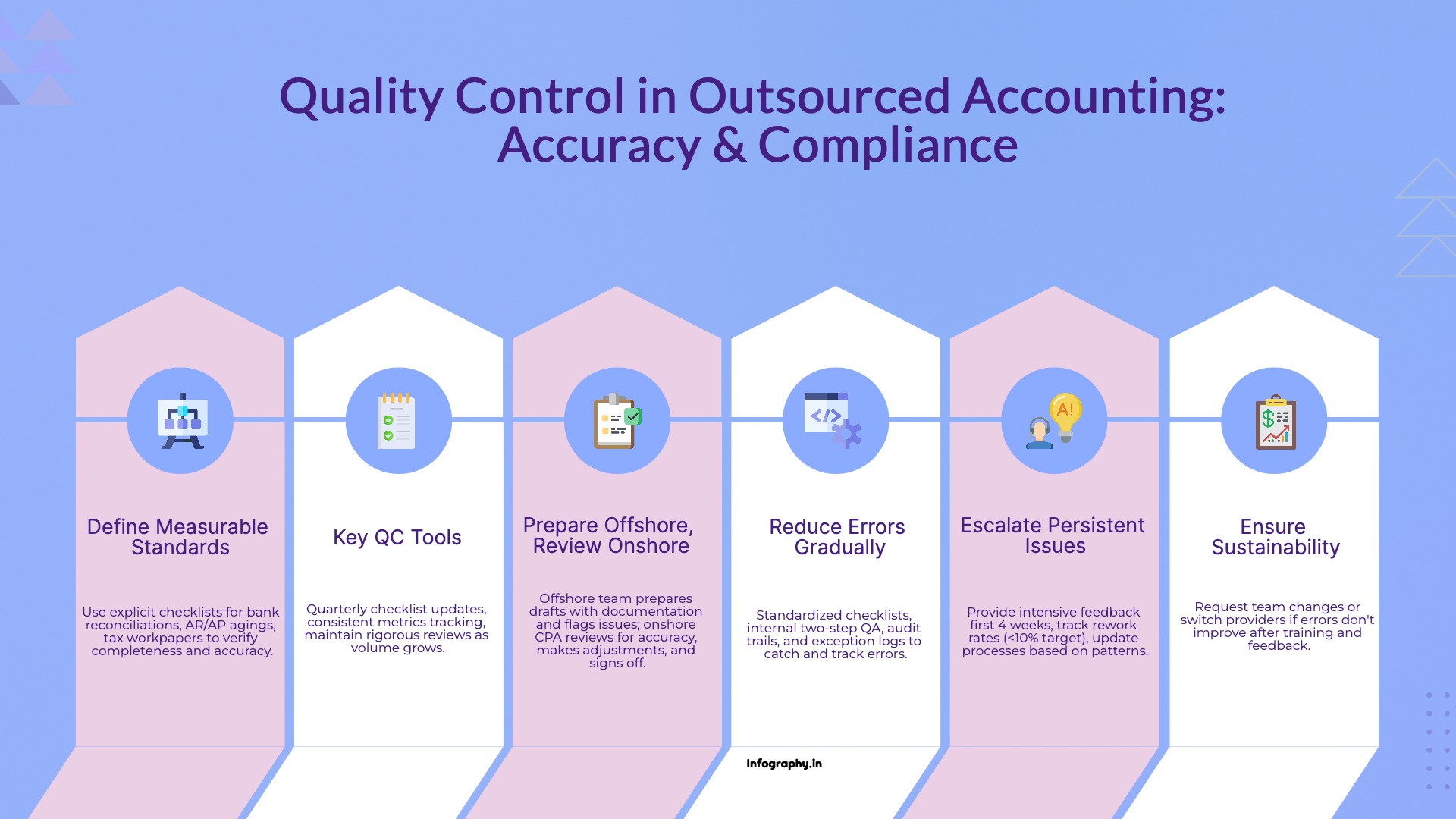

For most CPA firms, the model that maintains quality while gaining efficiency is straightforward. The offshore team prepares the first draft, attaches supporting documentation, and flags any exceptions or unusual items they encountered. The onshore staff reviews the work for accuracy and completeness, investigates flagged exceptions, makes any required adjustments, and signs off before the deliverable goes to the client or gets filed with an agency.

This division preserves professional responsibility where it belongs. The licensed CPA retains accountability for accuracy, compliance, and client communication. The offshore team provides production capacity that allows the CPA to review more work in less time than it would take to prepare everything from scratch. The quality control happens at the review stage, not at the delegation stage.

Quality is not a subjective feeling or a vague aspiration. It is a set of specific criteria that can be documented, measured, and verified through checklists. When quality standards are explicit, both the preparer and the reviewer know exactly what complete and acceptable looks like.

For monthly close work, quality might be defined as bank accounts reconciled to statement end date with all reconciling differences explained and supported by documentation, accounts payable and accounts receivable aging reports that tie out to general ledger balances, and balance sheet accounts with appropriate supporting schedules or analyses attached to the file.

For tax workpapers, quality standards might include organizer complete with all requested information and client signature, source documents labeled consistently and filed in the appropriate sections, recurring items compared to prior year with notes explaining changes, and calculations cross-checked to source documents with references documented.

When these standards are written down as checklists, the offshore team can self-check their work before submission. The reviewer can verify compliance systematically rather than trying to remember what should be checked. Deviations from the standard become immediately obvious rather than subjective judgment calls about whether work is good enough.

Standardized checklists are the foundation. Use one checklist per workflow type. Keep it focused and actionable. If the checklist is ten pages long, no one will use it. If it is ten items that can be verified in minutes, it becomes part of the workflow rather than an administrative burden.

Two-step internal quality assurance means the provider reviews work before sending it to your firm. Many providers have internal reviewers who check for common errors, missing documentation, and compliance with client-specific requirements before submission. This internal review catches obvious issues and reduces the rework burden on your team. Ask providers whether they have internal QA and what their review process includes.

Audit trails in the accounting system provide visibility into who made what changes and when. If an entry is moved or an account balance changes, the system log shows who made the edit and ideally includes a note explaining why. This accountability prevents silent errors and makes troubleshooting faster when discrepancies are discovered.

Exception logs track errors and recurring issues in a centralized location. When the same type of error appears on multiple engagements, that is a signal that training or documentation needs improvement. The exception log reveals patterns that individual file reviews might miss. If three bank reconciliations in one week all miss the same type of reconciling item, the checklist needs to be updated to address that gap.

Error reduction does not happen through hope or increased effort. It happens through systematic feedback and process improvement. The first few weeks of an outsourcing relationship will have higher error rates as the offshore team learns your standards, your clients, and your software. This calibration period is normal and expected.

During weeks one through four, review more heavily than you will long-term. Provide detailed feedback with clear examples of what was wrong and what the correct approach should have been. When the same issue appears on multiple files, update the checklist to prevent recurrence. This intensive early feedback accelerates learning and sets clear quality expectations.

Track error rates and rework percentages weekly. If errors are declining, the system is working. The offshore team is learning from feedback and improving their output. If errors stay flat or increase, something is wrong with training, documentation, or personnel. Diagnose the problem quickly rather than hoping it resolves itself.

After the calibration period, error rates should stabilize at acceptable levels. Define what acceptable means for your firm. Some firms target less than 10 percent rework. Others aim for less than 5 percent for routine workflows. The specific target matters less than having a target and measuring against it.

If error rates are not improving after four to six weeks of intensive feedback, escalate to the provider's management. This is not normal learning curve. It indicates a mismatch between the team's skills and your requirements, or a fundamental problem with how training is being conducted.

If the same team member repeatedly makes the same errors despite feedback and updated checklists, request a personnel change. Not everyone is suited for the precision and attention to detail that accounting work requires. Providers should be willing to swap team members who are not performing.

If structural issues emerge, such as the provider lacking internal review processes or being unable to follow your documentation standards, consider changing providers. Quality problems caused by provider inadequacy rather than normal learning curves are not problems you can fix through better training or clearer feedback.

Quality control is not a one-time setup. It is an ongoing discipline that requires regular attention and refinement.

Review your checklists quarterly and update them based on error patterns, client feedback, and changes in accounting standards or firm procedures. Checklists that never evolve become outdated and lose effectiveness.

Measure quality metrics consistently and track trends. Are error rates stable, improving, or declining? Are certain workflows more error-prone than others? Is quality consistent across different clients or does it vary? This data reveals where to focus improvement efforts.

Protect review time and standards as volume increases. The temptation when capacity expands is to rush through review or reduce quality checks to keep up with higher volume. This is a mistake. Quality standards should remain constant or tighten as the firm scales. If review becomes a rubber stamp, errors will slip through and client satisfaction will decline.

Quality in outsourced accounting is achieved through structure, measurement, and discipline, not through luck or heroic individual effort. Firms that build quality into their workflows through checklists, review processes, error tracking, and continuous improvement see high-quality output regardless of where preparation happens. Firms that wing it and hope for the best get inconsistent results and end up convinced that outsourcing compromises quality when the real problem was inadequate process design.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.