Direct Answer: Real estate investors can defer capital gains taxes through five primary strategies: 1031 like-kind exchanges (defer indefinitely by exchanging properties), installment sales (spread gains over multiple years), opportunity zones (defer until 2026 and reduce by 10%), Delaware Statutory Trusts (passive 1031 exchange alternative), and charitable remainder trusts (defer while generating income). The most powerful is the 1031 exchange, which allows unlimited tax deferral by continuously exchanging properties until death, when heirs receive stepped-up basis and eliminate all deferred taxes. Combined federal and state capital gains rates reach 37.1% in high-tax states, making deferral strategies worth $371,000 on a $1 million gain.

A Los Angeles real estate investor called us last year facing a $340,000 tax bill on a $1.2 million property sale. He'd purchased the property in 2010 for $400,000, claimed $145,000 in depreciation over 14 years, and now owed federal capital gains tax (20%), net investment income tax (3.8%), California state tax (13.3%), and depreciation recapture (25% federal). That's a 37%+ combined rate. We structured a 1031 exchange into a Delaware Statutory Trust, deferring all taxes and generating passive income while he transitioned toward retirement. Five years later, those deferred taxes remain unpaid.

Understanding tax deferral strategies separates sophisticated investors from those who unnecessarily pay hundreds of thousands in capital gains taxes. Since 2015, our team has helped 200+ real estate investors defer over $150 million in capital gains through proper strategy selection and execution. The key is matching the right deferral strategy to your investment goals, timeline, and exit plan.

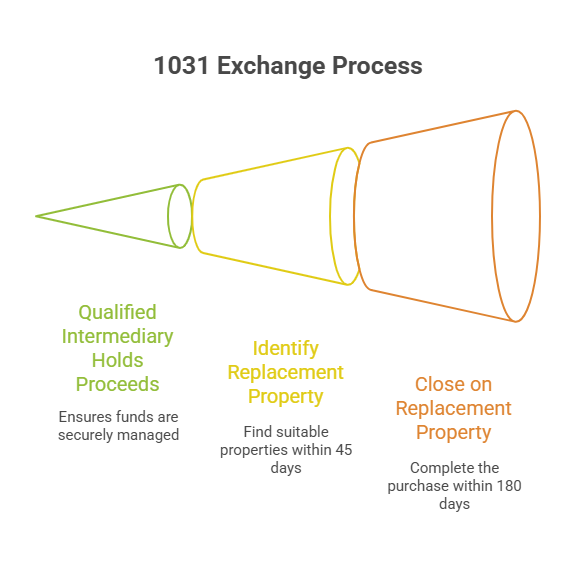

A 1031 exchange, named after Section 1031 of the Internal Revenue Code, allows you to defer all capital gains and depreciation recapture taxes by exchanging one investment property for another of equal or greater value. You sell your relinquished property, use a qualified intermediary to hold the proceeds, and purchase replacement property within strict timelines: identify potential replacements within 45 days, close within 180 days.

The strategy defers taxes indefinitely through continuous exchanges. Sell Property A, exchange into Property B, later exchange B into C, then C into D. Each exchange defers all accumulated gains. Hold the final property until death, and your heirs receive stepped-up basis equal to fair market value, eliminating all deferred taxes permanently. This "swap till you drop" strategy is how multi-generational wealth is built in real estate.

Properties must be like-kind (real property for real property), held for investment or business use, and located in the United States. A rental property in Texas can exchange for raw land in Montana, an apartment building in Florida, or a shopping center in Oregon. The IRS defines "like-kind" broadly for real estate, virtually any real property qualifies to exchange for any other real property.

To defer all taxes, your replacement property must equal or exceed your relinquished property in both value and debt. Sell a property for $800,000 with a $300,000 mortgage, and you must purchase replacement property worth $800,000+ with debt of $300,000+ or add cash to make up the difference. Any cash received (boot) is immediately taxable. Understanding state-specific 1031 exchange requirements prevents withholding surprises in states like California and Oregon.

Real example: An investor purchased a Dallas duplex in 2008 for $250,000, claimed $91,000 in depreciation, and sold in 2024 for $580,000. Capital gain is $330,000 ($580,000 sale - $250,000 purchase) plus $91,000 depreciation recapture. Federal tax would be $89,050 (20% on $330,000 gain + 25% on $91,000 recapture + 3.8% NIIT). A 1031 exchange into a $650,000 Arizona property defers all $89,050 in taxes.

Delaware Statutory Trusts (DSTs) are pre-packaged real estate investments that qualify as replacement properties in 1031 exchanges. You own a fractional interest in institutional-grade real estate (apartments, medical offices, industrial warehouses) managed by professional sponsors. DSTs solve the problem of finding and managing replacement properties, especially for investors wanting to exit active management while still deferring taxes.

DSTs provide passive income without landlord responsibilities. The sponsor handles all property management, leasing, repairs, and reporting. You receive monthly or quarterly distributions like dividends, typically 4-6% annually. This makes DSTs attractive for retiring investors who want to defer capital gains while transitioning from active property management to passive income streams.

Investments start at $100,000-250,000 minimums and must be held as part of a 1031 exchange or purchased directly by accredited investors. DSTs are securities offerings requiring accreditation ($200,000+ income or $1 million+ net worth excluding primary residence). The sponsor typically holds properties for 5-7 years, then refinances or sells, triggering another exchange decision for investors.

The biggest limitation is lack of control. You cannot make decisions about property management, refinancing, or sale timing. The DST sponsor controls everything. You're also locked in until the sponsor decides to exit, there's no secondary market to sell your interest early. Additionally, DSTs carry higher fees than direct property ownership: acquisition fees (1-2%), ongoing asset management fees (0.25-1% annually), and disposition fees (1-2% at sale).

However, DSTs provide benefits direct ownership can't: institutional-grade properties you couldn't afford individually ($50 million apartment complex), professional management, geographical diversification across multiple properties, and elimination of active management time. For investors with $500,000+ in exchange proceeds who want to exit landlording, DSTs provide a valuable 1031 exchange solution.

Installment sales spread capital gains taxation over multiple years by financing the sale yourself rather than receiving all proceeds at closing. The buyer makes payments over time (5, 10, even 30 years), and you report gains proportionally as you receive each payment. This defers taxes and potentially keeps you in lower tax brackets by spreading income across multiple years.

Calculate your gross profit percentage (gain ÷ sale price) and apply it to each payment received. Sell a property for $1 million with $400,000 in basis, creating $600,000 in gain. Your gross profit percentage is 60% ($600,000 ÷ $1,000,000). Receive $200,000 down payment? Report $120,000 as taxable gain (60% of $200,000). Receive $100,000 annually for 8 years? Report $60,000 gain annually (60% of $100,000).

Installment sales work particularly well when selling to family members or transitioning businesses. A retiring landlord can sell rental properties to adult children through installment sales, spreading his tax bill over 10-20 years while the kids gradually pay him from rental income. This keeps the seller in lower tax brackets (avoiding 20% capital gains rates by staying in 15% bracket), provides steady retirement income, and facilitates intergenerational wealth transfer.

The strategy carries risk: the buyer might default, leaving you with a partially-paid property you must foreclose on. Interest income from installment notes is taxed as ordinary income (up to 37% federal), not capital gains. If the buyer later resells the property, it doesn't affect your remaining installment obligations, you still report gains as you receive payments from the original buyer. Structuring tax-efficient installment sale terms requires careful planning around interest rates, payment schedules, and default provisions.

Installment sales cannot be combined with 1031 exchanges in the traditional sense. However, you can structure installment sales of the relinquished property if properly documented, though this is complex and requires expert guidance. Most investors choose either installment sale or 1031 exchange, not both simultaneously for the same transaction.

Qualified Opportunity Zones (QOZs) allow you to defer capital gains by investing in economically distressed communities designated by the Treasury Department. Invest your gains into a Qualified Opportunity Fund within 180 days of realizing the gain, and you defer taxes until December 31, 2026, or when you sell your QOZ investment, whichever comes first. Additionally, holding the QOZ investment 5+ years reduces the deferred gain by 10%, and holding 10+ years eliminates all taxes on QOZ appreciation.

The program was created by the Tax Cuts and Jobs Act of 2017 to incentivize investment in underserved areas. There are 8,764 designated opportunity zones across all 50 states, Puerto Rico, and U.S. territories. Zones include areas in downtown Los Angeles, rural Mississippi, industrial Detroit, and growing suburbs in Phoenix. The designation doesn't mean the area is dangerous, many zones are simply lower-income census tracts undergoing revitalization.

You must invest the gain amount, not the entire sale proceeds. Sell a property for $1 million with $400,000 basis and $600,000 gain? You must invest $600,000 in a QOF within 180 days to defer all taxes. You can keep the $400,000 basis without investing it. However, most investors reinvest all proceeds to maximize returns since QOZs can appreciate substantially in developing areas.

The tax benefits are substantial but nuanced. A $600,000 gain invested in 2020 (before the 5-year threshold passed) would be reduced by 10% ($60,000) if held 5+ years, meaning you'd only pay taxes on $540,000 when the deferral ends December 31, 2026. If your QOZ investment appreciates to $1.2 million by 2030, that $600,000 in appreciation is completely tax-free if you've held 10+ years.

QOZs carry significant risks: you're investing in developing areas with uncertain appreciation, you're locked in for 10 years to get maximum benefits, and fund management quality varies dramatically. Some QOZ funds are professionally managed with strong track records, while others are first-time sponsors lacking real estate experience. Due diligence is critical, investigate the sponsor, the specific properties or development plans, and the fund's fee structure (typically 1-2% annual management fees plus 20% performance carry).

Charitable Remainder Trusts (CRTs) eliminate immediate capital gains taxes by donating appreciated real estate to an irrevocable trust that pays you income for life or a set term, then distributes the remainder to charity. The trust sells the property tax-free, invests the proceeds, and pays you annual income (5-50% of trust value annually). You get an immediate charitable deduction, tax-free sale, lifetime income, and a legacy gift to charity.

CRTs work best for highly appreciated property with low basis that you want to convert to income-producing assets. Own a rental property purchased for $100,000 now worth $1 million? Transfer it to a CRT. The trust sells for $1 million with zero capital gains tax (charities are tax-exempt), invests the full $1 million, and pays you 5-7% annually ($50,000-70,000) for life. Without the CRT, you'd pay $200,000+ in taxes at sale, leaving $800,000 to invest and generate $40,000-56,000 annually, substantially less income.

You receive an immediate charitable deduction for the present value of the charity's remainder interest. Using IRS tables based on your age and the trust payout rate, a 65-year-old establishing a $1 million CRT with 6% payout might get a $400,000 charitable deduction, saving $148,000 in federal taxes (37% bracket). This partially offsets the loss of control over the asset and the fact that your heirs won't inherit it.

The main drawback is irrevocability, once you transfer property to a CRT, you cannot get it back. The property will eventually go to charity, not your heirs. This makes CRTs suitable for investors without heirs, those with substantial wealth already passing to family, or individuals with strong charitable intent. Some investors use life insurance to replace the asset value for heirs, use your tax savings and increased income to purchase life insurance equal to the property's value, ensuring heirs receive equivalent wealth.

CRTs require professional setup: legal fees run $3,000-7,000, annual tax return preparation costs $1,000-2,000, and you need a trustee (often a bank or trust company) charging 0.5-1.5% annually. These costs make CRTs economical for property values exceeding $500,000-1,000,000. Below that threshold, the complexity and expense often outweigh the benefits.

Section 121 allows homeowners to exclude up to $250,000 (single) or $500,000 (married) of capital gains when selling their primary residence. To qualify, you must own and live in the home for 2 of the 5 years before selling. This isn't technically "deferral", it's permanent exclusion, meaning you never pay taxes on excluded gains. This creates opportunities for investors who convert rental properties to primary residences.

The strategy involves converting rental property to your primary residence for 2+ years before selling. Buy a rental property, hold it for several years, move in and make it your primary residence for 2 years, then sell and claim the $250,000/$500,000 exclusion. However, the IRS reduced this strategy's effectiveness with "non-qualified use" rules that prorate the exclusion based on rental vs. personal use periods after 2008.

Real example: Purchase a rental property in 2015, rent it until 2020 (5 years non-qualified use), move in from 2020-2023 (3 years personal use), then sell. You have 5 years non-qualified use out of 8 total years (62.5% non-qualified). Your $500,000 exclusion gets reduced to $187,500 (37.5% qualified use). Additionally, you must recapture all depreciation claimed during rental years, that's always taxable regardless of the exclusion.

Despite limitations, converting rental properties to primary residences before selling can save substantial taxes, especially on highly appreciated properties. An investor with a $700,000 gain on a former rental property might owe $150,000+ in federal taxes. Moving in for 2 years and claiming even a partial $250,000 exclusion saves $50,000+ in taxes. Understanding the complex interaction between state rental property tax rules and federal exclusions maximizes your savings.

Choose 1031 exchanges when you want to continue owning investment real estate and indefinitely defer all taxes. This works for investors in wealth accumulation phase who plan to hold properties long-term or exchange multiple times. The strategy provides maximum tax deferral with no immediate recognition of any gain. It's the default choice for most active real estate investors under age 60 who aren't ready to exit real estate entirely.

Choose Delaware Statutory Trusts when you want passive income without management responsibilities while still deferring taxes through 1031 exchanges. DSTs suit retirees or investors with $500,000+ in exchange proceeds who are tired of tenant calls, maintenance issues, and active management. The trade-off is loss of control and higher fees, but you gain professional management and institutional-quality properties.

Choose installment sales when selling to family members, need steady retirement income, or want to spread gains over multiple years to stay in lower tax brackets. This strategy works well for investors with moderate gains ($100,000-500,000) who have creditworthy buyers willing to pay over time. The risk is buyer default, but proper security instruments (mortgages, deeds of trust) mitigate this concern.

Choose Opportunity Zone funds when you're willing to lock in capital for 10 years and invest in developing areas for potential tax-free appreciation. This suits investors with risk tolerance for emerging markets and ability to commit capital long-term. The 2026 deferral deadline is approaching fast, making QOZ decisions time-sensitive. Only invest in QOZ areas where you believe in the development potential, tax benefits alone don't justify bad investments.

Choose Charitable Remainder Trusts when you have substantial wealth, strong charitable intent, and want to convert appreciated property to lifetime income. CRTs work for investors 60+ with properties worth $1 million+ who don't need to preserve that specific asset for heirs. The immediate charitable deduction, tax-free sale, and increased income often provide better financial outcomes than simply selling and paying capital gains taxes.

The biggest mistake is waiting until after selling to explore deferral options. You cannot initiate a 1031 exchange after closing, you must use a qualified intermediary before closing, and your contract should include exchange language. Investors who sell properties, receive proceeds, then call asking about 1031 exchanges have lost the opportunity forever. Deferral strategies require advance planning, not reactive tax minimization after the fact.

Violating 1031 exchange timelines disqualifies the entire transaction. Miss your 45-day identification deadline by even one day? Full taxable sale. Close on day 181 instead of 180? Full taxable sale. These deadlines are absolute with virtually no extensions granted. Calendar management is critical, we've seen investors lose $100,000+ in deferred taxes because they missed deadlines by 24 hours. Proper tax deadline tracking prevents these expensive mistakes.

Receiving proceeds directly invalidates 1031 exchanges. Even touching the money for one second disqualifies the exchange. You must use a qualified intermediary to hold all proceeds from sale until purchasing replacement property. Some investors try to use their attorney or CPA as intermediary, this creates disqualified person issues. Use an independent, bonded qualified intermediary, and never have sale proceeds deposited into accounts you control.

Underestimating complexity leads to failed executions. Each strategy has nuanced rules, timing requirements, and documentation needs. DIY attempts at 1031 exchanges, CRTs, or installment sales often fail due to technical errors. A $50,000 gain might justify self-execution risk, but $500,000+ gains warrant professional guidance. The cost of expert help ($2,000-10,000) pales compared to losing six-figure tax deferral opportunities through execution errors.

Choosing strategies based solely on tax benefits without considering investment quality creates losses that exceed tax savings. A bad Opportunity Zone investment that loses 30% of your capital costs more than the 20% capital gains taxes you deferred. A 1031 exchange into overpriced property because you're racing a 180-day deadline destroys wealth. Tax deferral is valuable, but sound investment fundamentals must come first, never let the tax tail wag the investment dog.

Indefinitely. You can perform unlimited sequential 1031 exchanges throughout your lifetime, deferring capital gains from Property A to B to C to D continuously. The taxes don't accumulate or compound, they simply defer. Hold your final property until death, and your heirs receive stepped-up basis equal to fair market value, permanently eliminating all deferred gains and depreciation recapture. This "swap till you drop" strategy is how generational real estate wealth is built.

Yes, 1031 exchanges work across state lines. You can sell property in California and buy replacement property in Florida, Texas, or any other state. However, some states like California and Oregon require withholding at closing even on 1031 exchanges, California withholds 3.33%, Oregon 8%. You'll need to file state tax returns to recover the withholding. The property must be located within the United States, no foreign property qualifies.

Deferring means postponing taxes to a future date, you'll eventually pay unless you hold until death for stepped-up basis. Avoiding means permanently eliminating taxes through exclusions like the $250,000/$500,000 primary residence exclusion or holding Opportunity Zone investments for 10+ years. Most real estate tax strategies defer rather than eliminate taxes, though proper planning can convert deferred taxes into permanent avoidance through death or exclusions.

Not immediately. The IRS requires replacement property to be held for investment or business use, not personal residence. Most tax advisors recommend holding 1031 exchange property as a rental for at least 2 years before converting to personal use. Converting too quickly (within 1 year) triggers IRS scrutiny and potential disqualification. After sufficient holding period, you can convert to personal residence and later qualify for the $250,000/$500,000 primary residence exclusion with prorated adjustments.

Qualified intermediary fees typically range from $800-1,500 for standard exchanges. This covers document preparation, escrow services, and compliance support through both sale and purchase. Complex exchanges involving multiple properties or reverse exchanges cost $2,000-5,000+. These fees are small compared to the taxes deferred, a $500,000 gain defers $100,000-185,000 in federal and state taxes, making $1,200 in QI fees insignificant.

DSTs are as safe as the underlying real estate and sponsor quality. They're not FDIC insured or guaranteed. DSTs own real property subject to market risks, tenant defaults, and economic downturns. Due diligence on the sponsor's track record, property quality, and debt levels is critical. Well-structured DSTs with experienced sponsors and quality properties provide stable returns, but poorly structured DSTs can lose value. Always review the Private Placement Memorandum and work with advisors before investing.

Yes, but you'll pay taxes on any cash received (called "boot"). The boot is taxed as capital gain up to the total gain realized. For example, sell property for $800,000 with $300,000 gain, exchange into $700,000 replacement property, and receive $100,000 cash. You'll pay capital gains tax on $100,000 of your $300,000 total gain. The remaining $200,000 gain defers. Minimize boot to maximize deferral.

Absolutely, especially for gains exceeding $100,000. One mistake in 1031 exchange timing, qualified intermediary selection, or documentation can disqualify your entire deferral, triggering six-figure tax bills. Professional guidance costs $2,000-10,000 but protects $50,000-500,000+ in deferred taxes. The complexity of combining federal rules, state requirements, and investment decisions justifies expert help. Since 2015, our team has helped 200+ investors successfully defer over $150 million in capital gains through proper strategy selection and execution.

Real estate tax deferral strategies provide legal methods to postpone or eliminate capital gains taxes that would otherwise consume 20-37% of your investment profits. The 1031 exchange remains the most powerful tool for active investors, offering unlimited deferral through sequential exchanges until death provides stepped-up basis. Delaware Statutory Trusts, installment sales, Opportunity Zones, and Charitable Remainder Trusts each serve specific investor circumstances and goals.

The key to successful deferral is advance planning, waiting until after closing eliminates most options. Start exploring strategies 6-12 months before anticipated sales, understand the timing requirements and limitations of each approach, and work with qualified intermediaries and tax professionals who specialize in real estate transactions. A $200,000 capital gain defers $40,000-74,000 in federal and state taxes, money you can reinvest to compound wealth.

Since 2015, Madras Accountancy has guided 200+ real estate investors through successful tax deferral strategies, from basic 1031 exchanges to complex multi-property transactions and trust structures. If you're planning to sell investment property and want expert guidance on maximizing tax deferral while maintaining investment quality and liquidity goals, our team can help you navigate the options and execute strategies that preserve your wealth for future growth rather than unnecessary tax payments.

Related read: tax states.

Related read: 3 3.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.