Outsourcing accounting and tax work is legal. There are no regulatory prohibitions against CPA firms working with offshore teams. The confusion and anxiety around compliance does not stem from a ban on outsourcing. It stems from firms implementing outsourcing poorly, without proper controls, documentation, or oversight. When things go wrong, it is not because outsourcing was prohibited. It is because the firm failed to maintain the standards required for any accounting work, regardless of where it is performed.

This is not legal advice. It is a practical compliance overview based on common requirements and professional standards that apply to CPA firms. Every firm should review its specific state board rules, professional liability insurance requirements, and client engagement letters. Use this as a starting checklist, not as a substitute for consultation with your own counsel and compliance advisors.

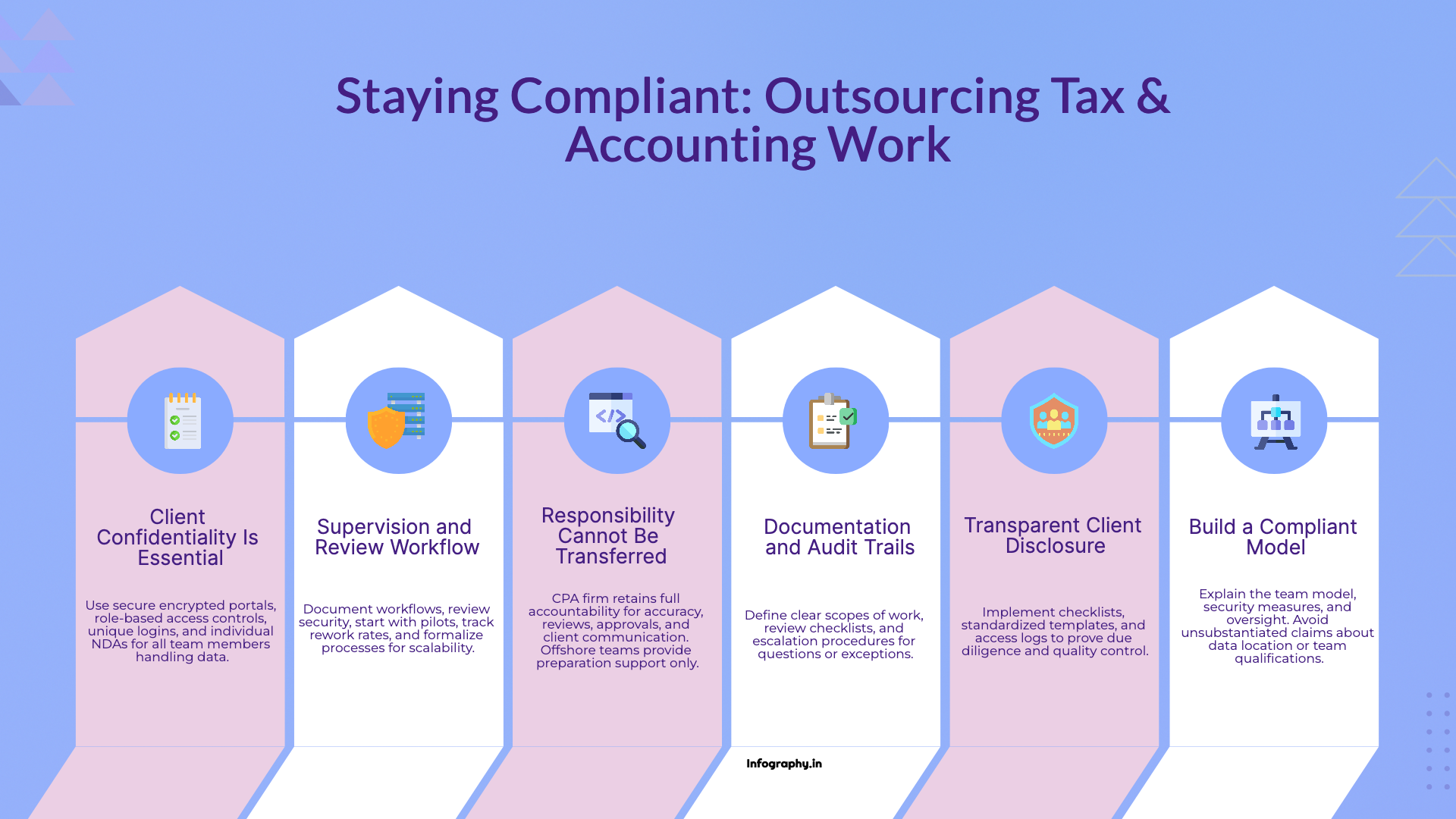

The most fundamental principle of outsourcing compliance is that delegating tasks does not delegate responsibility. The CPA who signs a tax return remains responsible for its accuracy, regardless of who prepared the underlying workpapers. The partner who signs an audit report remains responsible for the conclusions reached, regardless of who performed the fieldwork. The firm that issues financial statements remains responsible for their accuracy, regardless of who handled the bookkeeping.

This means the offshore team cannot make final judgments on technical accounting issues, cannot sign returns or reports, and cannot communicate directly with clients about complex or sensitive matters. Their role is preparation and support. The licensed professionals at the firm retain review, approval, and client communication responsibilities.

In practical terms, this division of labor looks like the offshore team preparing tax workpapers, calculating schedules, and assembling documentation. The US CPA reviews the work, investigates any unusual items, makes technical determinations where judgment is required, and signs the return. If the IRS later questions the return, the CPA is accountable, not the person who prepared the workpapers. This is no different from how firms have always worked with staff accountants and administrative support. The principle is the same whether the support is in the next cubicle or halfway around the world.

Professional standards require CPA firms to protect client information. This obligation does not change when work is outsourced. The firm remains responsible for ensuring that client data is handled securely, access is restricted to those who need it, and breaches are prevented through appropriate technical and administrative controls.

Secure file portals are essential. Email is not a secure transmission method for sensitive financial documents. Client tax returns, bank statements, and financial records should be transmitted through encrypted portals with access logging and audit trails. The portal should track who accessed which files and when, creating a record that can be reviewed if questions arise.

Role-based access controls ensure that each person only has access to the information they need for their assigned tasks. If an offshore team member is working on payroll for five clients, they should not have access to files for clients they are not supporting. Unique logins for each team member, rather than shared credentials, make it possible to track individual access and enforce accountability.

Non-disclosure agreements should be signed by every individual who will have access to client information. The agreement should specify data handling requirements, confidentiality obligations, and consequences for violations. While the outsourcing provider typically has master agreements covering these points, individual NDAs create an additional layer of accountability and make expectations explicit.

Offshore staff should work under supervision, with clear review steps built into the workflow. This is not unique to outsourcing. Supervision and review are standard practice for any accounting work performed by less experienced staff. The same principles apply when the staff happens to be offshore.

Define what the offshore team prepares. Create a written scope of work that lists the specific tasks, deliverables, and quality standards. If the offshore team is handling bank reconciliations, the scope should specify which accounts, what documentation is required, how discrepancies should be flagged, and what format the deliverable should take. Clarity at the front end prevents confusion and quality issues later.

Define what the onshore team reviews. The review should not be a rubber stamp. It should be a substantive examination of the work product, checking for accuracy, completeness, and compliance with firm standards. Document the review steps in a checklist so the review is consistent regardless of who performs it.

Define escalation procedures for exceptions and technical questions. The offshore team will encounter situations where they are unsure how to proceed. There should be a clear path for raising questions, a defined response time, and a designated person responsible for answering. Without an escalation process, the offshore team may make assumptions that lead to errors, or they may stop working while they wait for guidance, creating delays.

Compliance is easier to demonstrate when workflows are documented and activity is logged. If a regulator, client, or insurance carrier asks how the firm maintains quality when outsourcing, documented processes and audit trails provide clear answers.

Checklists for each workflow ensure consistency and provide evidence that standard procedures were followed. When a bank reconciliation checklist shows that uncleared items were investigated, supporting documentation was obtained, and the reconciliation was reviewed by a senior accountant, that checklist serves as proof of due diligence.

Templates for recurring workpapers standardize the format and content of deliverables. If every tax return preparation includes the same set of workpapers in the same format, review is faster and omissions are easier to spot. Templates also make training more efficient because new team members have a clear model to follow.

Access logs and change tracking provide visibility into who did what and when. If a client questions when their financial statements were prepared or who worked on their file, the logs provide definitive answers. This transparency is valuable not just for compliance, but for resolving disputes and managing client relationships.

Some clients will ask whether their work is being outsourced. This is a reasonable question, and the answer should be straightforward. Explain that the firm uses a team model where preparation work is handled by specialized staff, and review and final approval are handled by licensed CPAs at the firm. Emphasize that responsibility remains with the firm, that security controls are in place, and that the workflow includes multiple quality checks.

Do not make claims you cannot prove. If you tell a client that their data never leaves the United States, that claim must be true. If you tell them that all team members are CPAs, that must be accurate. Misrepresenting the outsourcing arrangement is not just poor client management. It is a potential ethical violation and a liability risk if the misrepresentation is discovered.

Most clients care less about where the work is performed and more about whether it is done correctly, on time, and securely. If you can demonstrate that your outsourcing model includes proper controls and oversight, most clients will be satisfied. The few who have strong objections to any outsourcing can be accommodated through alternative staffing arrangements if necessary.

Start by documenting the workflow and the review chain. Write down who prepares what, who reviews it, and who has final approval authority. This documentation serves as both an operational guide and compliance evidence.

Review security controls before sharing any client data with the offshore team. Confirm that secure portals are in place, that access controls are configured properly, and that NDAs are signed. Do not shortcut security setup in the interest of speed. A security breach or data loss incident can destroy client relationships and create regulatory problems that take years to resolve.

Start with a pilot scope and measure rework rates. A small pilot allows you to test the workflow, identify compliance gaps, and refine procedures before scaling. Track how often work needs to be returned for corrections, how long reviews take, and whether the offshore team is following procedures consistently. If the pilot reveals compliance concerns, address them before expanding.

Most compliance issues with outsourcing arise when firms treat it as informal, ad hoc help rather than a formal part of their operating model. Informal arrangements lack documentation, oversight, and quality controls. Formal workflows with clear roles, documented procedures, and regular review create a compliant outsourcing model that regulators, clients, and insurers can understand and accept.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.