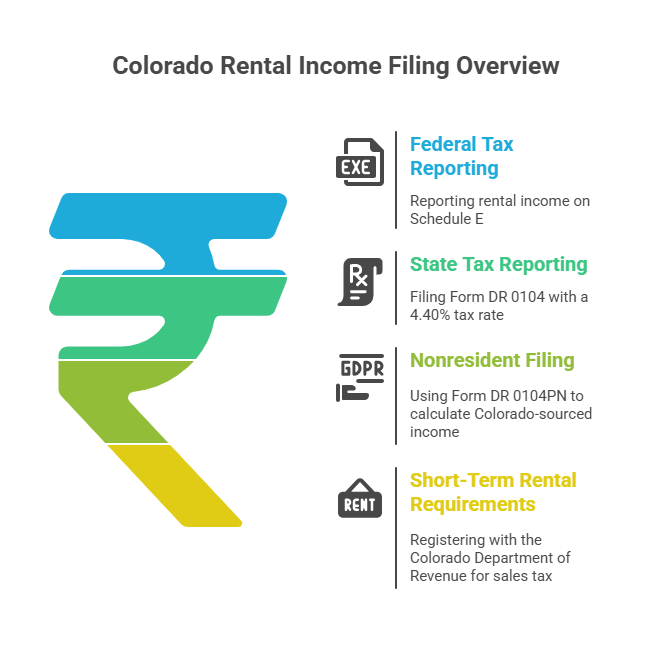

Quick Answer: Colorado landlords must file federal Schedule E to report rental income and Form DR 0104 for state taxes (4.40% flat rate). Short-term rental operators (under 30 days) must register with the Colorado Department of Revenue for sales tax licenses and file regular returns. Nonresidents use Form DR 0104PN to calculate Colorado-sourced income. Long-term rental landlords file annually, while short-term operators file monthly, quarterly, or annually based on assigned frequency.

Colorado rental property owners face a complex web of federal, state, and local filing requirements that vary dramatically based on property type and rental duration. Miss a deadline or file incorrectly, and penalties start at $50 plus accumulating interest.

All Colorado rental property owners report rental income on federal Schedule E (Form 1040), regardless of property type or rental duration. This form captures rental receipts, deductible expenses, and calculates net rental income or loss. For state taxes, file Form DR 0104, Colorado's Individual Income Tax Return, which taxes rental income at the state's flat 4.40% rate.

Nonresidents owning Colorado rental properties must file even if they live out of state. Use Form DR 0104 in combination with Form DR 0104PN (Part-Year Resident/Nonresident Tax Calculation Schedule) to determine Colorado-sourced income. Colorado taxes only the income generated within the state, not your worldwide income.

Short-term rentals (under 30 consecutive days) trigger additional requirements. You must register with the Colorado Department of Revenue to obtain a sales tax license before accepting your first booking. This registration is mandatory even if platforms like Airbnb or VRBO collect taxes on your behalf. Proper tax compliance and deadline tracking prevents costly penalties.

Short-term rental operators face significantly more complex obligations. Register with the Colorado Department of Revenue at Colorado.gov/RevenueOnline to receive your sales tax license. Tax collection includes state sales tax (2.9%), county sales tax (varies), county lodging tax (1-5%), and special district taxes. Combined rates range from 8% to 15.7% depending on location.

Filing frequency depends on revenue, monthly, quarterly, or annual as assigned by the Colorado Department of Revenue. Most hosts file monthly by the 20th. Even months without bookings require zero-dollar returns. Most cities and counties require separate STR licenses costing $50-$350 annually, with specific local requirements varying by jurisdiction.

Colorado follows federal deduction rules. Common deductions include mortgage interest, property taxes, insurance, repairs, property management fees (8-12% of rent), and utilities. Depreciation provides substantial benefits, residential properties depreciate over 27.5 years (roughly 3.6% annually). A $300,000 property generates approximately $10,900 in annual depreciation deductions.

Travel expenses are deductible under specific rules. Track mileage at 67 cents per mile (2025 rate), lodging costs for property management trips, and meals at 50% deductibility. Maintain receipts, mileage logs, and business purpose notes. Cost segregation studies accelerate depreciation by identifying components with faster schedules. Understanding depreciation strategies and equipment deductions maximizes tax benefits.

Nonresidents with Colorado rental income must file state returns even when living elsewhere. File Form DR 0104 and Form DR 0104PN (nonresident calculation schedule). Calculate total taxable income as if you were a Colorado resident, then use DR 0104PN to determine Colorado-sourced percentages.

Property sales trigger 2% withholding of sales price or net proceeds at closing. File a Colorado return after the sale to claim refunds if withholding exceeds actual capital gains. Deductions work the same as for residents but apply only against Colorado income. Working with experienced tax professionals familiar with multi-state returns ensures proper filing.

Colorado's flat 4.40% state income tax applies to net rental income. Short-term rental rates vary by location, 2.9% state sales tax plus county (0.5-5%), county lodging (1-5%), and local taxes. Total rates climb from 8% to 15.7%. Annual income tax returns follow federal deadlines (April 15, extensions through October 15). Short-term rental returns follow assigned schedules: monthly filers submit by the 20th of the following month, quarterly filers face January 20, April 20, July 20, and October 20 deadlines.

Late filing penalties start at $50 or 5% of unpaid taxes, whichever is greater, plus monthly interest (currently 3-4% annually). Repeated violations trigger escalating consequences. Colorado aggressively audits rental properties, scrutinizing closing statements, bank records, and platform payment histories.

Tax evasion, deliberately avoiding taxes, constitutes a criminal offense with potential criminal charges, additional penalties, or imprisonment. Understanding legal tax avoidance versus illegal evasion protects landlords from serious consequences. STR license termination occurs after one year of non-filing, with some jurisdictions imposing $150-$500 daily fines for operating without valid licenses.

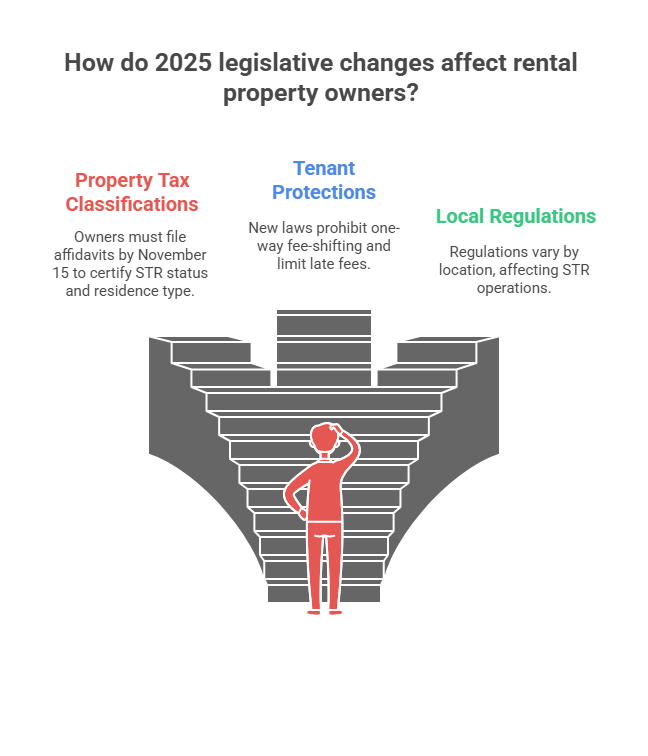

House Bill 24-1299 created new property tax classifications for short-term rentals. Owners must file annual affidavits by November 15 certifying STR status and whether properties are primary or secondary residences. Senate Bill 21-173 strengthened tenant protections, prohibiting one-way fee-shifting and limiting late fees to $50 or 5% of past-due rent. Local regulations evolve rapidly, with Summit County capping licenses, Lakewood requiring primary residence use, and Aspen limiting STRs to 120 days annually.

Since 2015, Madras Accountancy has provided comprehensive rental property tax services for Colorado landlords and CPA firms managing rental portfolios. Our offshore teams handle Schedule E preparation, Form DR 0104 filing, and complex multi-state returns for nonresident investors at 40% lower costs than traditional accounting firms.

We manage short-term rental tax compliance including Colorado Department of Revenue registration, monthly sales and lodging tax returns, and local jurisdiction filings. Our systematic approach tracks deductible expenses, maintains proper documentation, and ensures deadline compliance across multiple filing schedules. Experience with comprehensive tax planning and preparation helps landlords maximize deductions while maintaining full compliance.

Colorado landlords file federal Schedule E (Form 1040) to report rental income and expenses. For state taxes, file Form DR 0104 (Colorado Individual Income Tax Return). Short-term rental operators (rentals under 30 days) must register with the Colorado Department of Revenue for a sales tax license and file regular returns. Nonresidents file Form DR 0104PN to calculate Colorado-sourced income.

Yes. All short-term rental operators must register with the Colorado Department of Revenue to obtain a sales tax license, even if platforms like Airbnb collect taxes. Most cities and counties require separate local STR licenses or permits, typically costing $50-$350 annually. Registration requirements vary by jurisdiction, check with your local government for specific rules.

Colorado charges a flat 4.40% state income tax on rental income. Short-term rentals also face sales tax (2.9% state plus local rates), lodging taxes (varies by county, typically 1-5%), and potential special district taxes. Total combined rates for short-term rentals range from 8% to 15.7% depending on location.

Yes. Nonresidents deduct the same expenses as residents, mortgage interest, property taxes, insurance, repairs, property management fees, and travel expenses related to property management. However, deductions apply only against Colorado-sourced income when filing Form DR 0104PN. Proper documentation is essential for audit protection.

Long-term rental landlords file annually with their income tax returns. Short-term rental operators file sales and lodging tax returns monthly, quarterly, or annually based on revenue, the Colorado Department of Revenue assigns your filing frequency when you register. Even months without rental income require zero-dollar returns to maintain compliance.

Late filings trigger penalties starting at $50 or 5% of unpaid taxes, whichever is greater, plus interest accruing monthly. Repeated violations increase fines substantially. Tax evasion, deliberately avoiding taxes, can result in criminal charges, additional penalties, or imprisonment. Colorado aggressively audits rental properties, particularly short-term rentals.

Colorado doesn't require state-level rental licenses for long-term properties (30+ days). However, some cities like Denver and Boulder have local registration requirements. Written lease agreements are mandatory for terms of 12 months or longer. Check with your city or county for specific local requirements beyond state law.

Yes. Madras Accountancy provides comprehensive rental property tax services including Schedule E preparation, Form DR 0104 filing, multi-state compliance for nonresidents, and quarterly short-term rental tax returns. Our offshore teams handle complex deduction tracking and ensure proper documentation for Colorado Department of Revenue requirements at 40% lower costs than traditional firms.

Successful rental property management requires proactive tax planning and systematic record-keeping. Start by organizing income documentation, expense receipts, and property records by calendar year. For short-term rentals, register with the Colorado Department of Revenue immediately, operating without proper licenses triggers substantial penalties.

Madras Accountancy offers consultations for Colorado rental property owners and CPA firms managing rental portfolios. We'll review your filing requirements, identify missed deductions, and implement systems ensuring ongoing compliance with federal, state, and local regulations.

Related read: sales tax.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.