Quick Answer: New York recognizes federal 1031 exchange rules and allows investors to defer both federal and state capital gains taxes when exchanging like-kind investment properties. The state has no specific 1031 requirements except for nonresidents selling New York property, who must file Form IT-2663 to claim withholding exemptions. New York taxes income at the federal level, if you defer federal gains through a 1031 exchange, you defer New York state taxes too.

New York real estate investors face combined capital gains tax rates up to 10.9% at the state and city level plus federal rates approaching 37%. A 1031 exchange defers these taxes indefinitely by reinvesting sale proceeds into replacement properties, following federal Section 1031 rules with one critical state requirement: nonresidents must navigate Form IT-2663 withholding regulations.

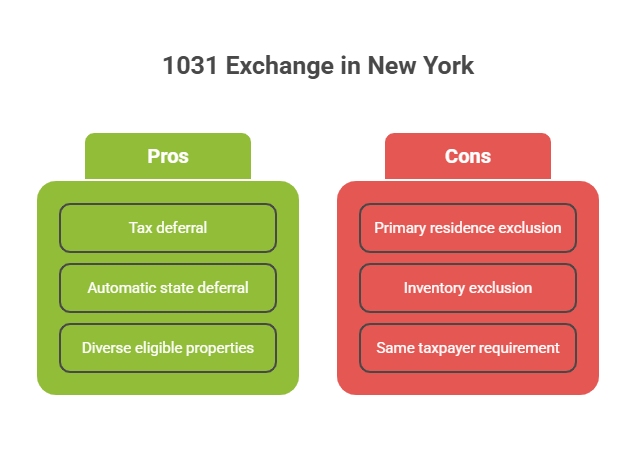

New York follows Internal Revenue Code Section 1031, allowing investors to defer capital gains taxes by exchanging investment or business-use properties for like-kind replacements. The state doesn't add requirements beyond federal law, when you defer federal capital gains, New York automatically defers state income tax because it taxes income reported federally.

Eligible properties include rental apartments, commercial buildings, industrial facilities, vacant land, and mixed-use properties. Primary residences, inventory held for resale, and dealer properties don't qualify. The same taxpayer must hold both the relinquished and replacement properties.

When nonresidents sell New York real estate, they face mandatory income tax withholding at 7.7%, the highest state tax rate. This withholding applies to the gain from the sale and requires payment before the deed can be recorded.

1031 exchanges qualify for withholding exemption. Nonresidents file Form IT-2663 before closing, check box 4B indicating a Section 1031 exchange, and provide a brief summary of the transaction. Recording officers won't accept deeds without either proof of withholding payment or the exemption certification.

This exemption creates a significant advantage: nonresidents who exchange New York property for out-of-state replacement properties effectively avoid New York state tax on the gain. Unlike California's clawback provision that tracks and eventually collects deferred state taxes, New York doesn't pursue gains after granting the exemption. Understanding the difference between legal tax avoidance and evasion helps investors confidently use these strategies.

Federal deadlines apply: identify replacement properties within 45 days of closing, complete the exchange within 180 days. These deadlines are absolute, missing by one day disqualifies the exchange and triggers immediate capital gains taxes. Weekends and holidays don't extend these periods. Smart investors identify multiple backup properties by day 30 and work with qualified intermediaries who manage timelines.

Delayed exchanges (90% of transactions) let investors sell first, then purchase replacement property within 180 days. A qualified intermediary holds proceeds, receiving funds directly disqualifies the exchange.

Reverse exchanges work when investors find replacement property before selling. An Exchange Accommodation Titleholder acquires and holds the replacement property during the sale period. New York provides a benefit: reverse exchanges avoid Real Estate Transfer Tax because the EAT, not the taxpayer, initially purchases the property.

Build-to-suit exchanges allow using exchange proceeds for property improvements. New York's Department of Taxation aggressively audits these transactions, scrutinizing whether improvements truly occurred during the exchange period.

The New York State Division of Tax Appeals aggressively audits 1031 exchanges, reviewing closing statements and financial records to identify unreported income or improper structures. In June 2025, the Division approved "drop-and-swap" transactions where partnerships distribute property to members immediately before sale, allowing individual exchanges.

The state monitors refinancing before and after exchanges. Excess loan proceeds above the relinquished property's debt count as taxable boot. Maintaining proper financial controls and documentation protects against audit challenges.

Yes. Federal law allows 1031 exchanges across state lines without restriction. You can sell Manhattan apartments and buy Florida commercial properties, as long as both properties qualify as investment or business-use real estate. Nonresidents who claim the Form IT-2663 exemption avoid New York state tax entirely on interstate transactions.

However, transfer taxes aren't exempted. New York City's Real Estate Transfer Tax applies regardless of 1031 exchange status, 1.425% to 2.625% depending on property value. Factor these costs into your exchange economics.

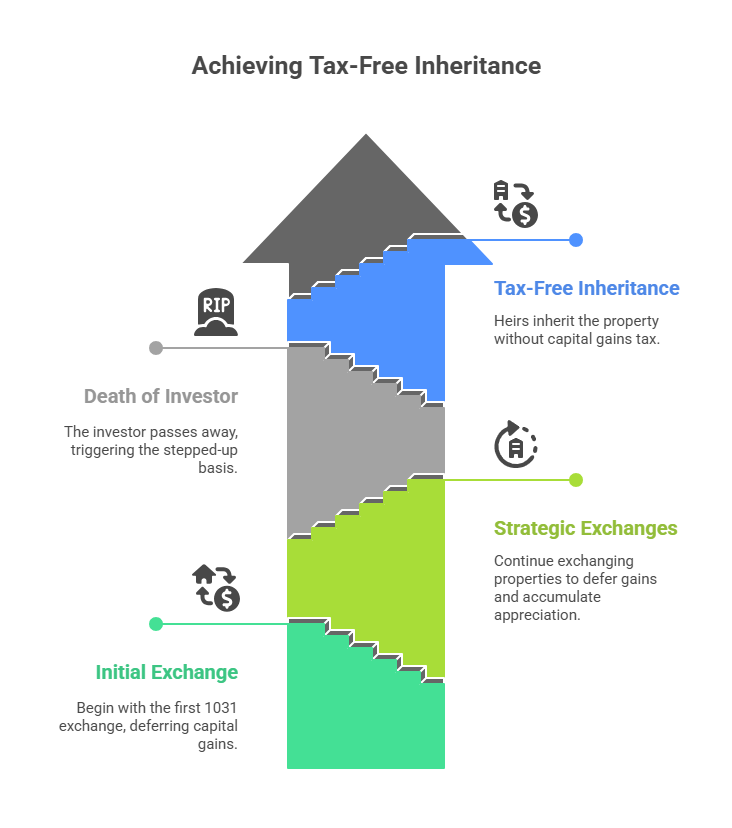

When you finally sell replacement property without another 1031 exchange, all deferred gains become taxable, including the original New York property gain plus subsequent appreciation. Strategic investors continue exchanging until death. The stepped-up basis at death eliminates deferred capital gains for heirs, permanently avoiding taxation through this "swap 'til you drop" strategy.

Alternatively, converting replacement property to a primary residence after two years allows partial exclusion under Section 121. Proper tax planning strategies combine these provisions to minimize eventual tax liability.

Missing the 45-day identification deadline disqualifies exchanges instantly. Start identifying properties the day you list your relinquished property. Receiving proceeds directly, even briefly, invalidates the exchange. All funds must flow through the qualified intermediary.

Underestimating replacement property value requirements causes partial taxable transactions. To defer 100% of gains, the replacement property must equal or exceed the relinquished property's value, and you must reinvest all cash proceeds.

Nonresidents who forget Form IT-2663 face immediate 7.7% withholding plus penalties. File before closing, recording officers won't accept deeds without proper documentation. Working with experienced tax professionals who understand state requirements prevents these errors.

Since 2015, Madras Accountancy has provided comprehensive 1031 exchange accounting support for real estate investors and CPA firms managing multi-state transactions. We prepare Form 8824, calculate adjusted basis, track depreciation schedules, and ensure proper documentation for both IRS and New York State requirements. Our systematic approach to audit preparation and documentation protects clients during examinations, while coordination with closing attorneys ensures timely Form IT-2663 filing for nonresidents.

Yes. New York follows federal 1031 exchange rules and allows investors to defer both federal and state capital gains taxes when exchanging investment properties. If you don't report gain to the IRS, you don't report it to New York. The state taxes income at the federal level, so properly structured 1031 exchanges defer New York's state income tax.

Form IT-2663 is the nonresident estimated income tax payment form required when selling New York real estate. For 1031 exchanges, check box 4B and provide a brief exchange summary. This exempts nonresidents from the mandatory 7.7% withholding that normally applies to property sales.

Yes. Federal law allows interstate 1031 exchanges without restrictions. You can sell New York property and purchase replacement property in any other U.S. state. However, nonresidents must file Form IT-2663 to claim the withholding exemption when conducting the exchange.

While New York doesn't have a statutory clawback provision like California, the Department of Taxation aggressively audits 1031 exchanges, particularly reverse and build-to-suit exchanges. Nonresidents who claim the withholding exemption effectively avoid New York state tax on gains when exchanging out of state, as the state doesn't track deferred gains long-term.

New York follows federal timelines: identify replacement properties within 45 days of selling your relinquished property, and complete the exchange within 180 days. These deadlines are strict, missing them by even one day disqualifies the entire exchange and triggers immediate capital gains tax liability.

Investment properties and business-use properties qualify, including rental apartments, commercial buildings, land, and industrial facilities. Primary residences, inventory held for resale, and properties held primarily for personal use don't qualify. Both the relinquished and replacement properties must be held for investment or productive business use.

Transfer taxes are not exempted in 1031 exchanges. When selling NYC property, you must pay the Real Estate Transfer Tax regardless of whether you're conducting a 1031 exchange. However, reverse exchanges structured with an Exchange Accommodation Titleholder avoid RETT on the replacement property acquisition.

Yes. Madras Accountancy provides comprehensive 1031 exchange support including Form 8824 preparation, basis calculations, depreciation tracking, and state compliance for New York investors. Our offshore accounting teams handle complex multi-state exchanges and ensure proper documentation for both federal and New York state requirements.

Successful 1031 exchanges require planning before listing your property. Identify qualified intermediaries, understand replacement property criteria, and prepare documentation for federal and state compliance. Madras Accountancy offers consultations for New York investors and CPA firms, reviewing transaction structures and providing comprehensive accounting support throughout the exchange process.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.