North Carolina real estate bookkeepers specialize in recording rental income, tracking property expenses, managing depreciation schedules, and preparing financial reports specifically for property investors, landlords, developers, and real estate professionals operating in North Carolina.

They understand NC-specific requirements including property tax assessment cycles, local transfer taxes varying by county, and the state's 4.75% flat income tax rate that applies to rental income. This expertise matters because proper bookkeeping separates profitable investments from money-losing properties and protects you during IRS and NCDOR audits.

North Carolina real estate investors face unique challenges: Charlotte's rapid appreciation requiring frequent basis adjustments, Raleigh-Durham's competitive rental market demanding precise cash flow tracking, and coastal properties in Wilmington and the Outer Banks with seasonal income patterns requiring careful planning. Whether you own single-family rentals in Greensboro, manage apartment complexes in Charlotte, or flip houses across the Triangle, specialized bookkeeping determines whether your investments generate sustainable returns or create tax nightmares. Here's what you need to know about working with North Carolina real estate bookkeepers.

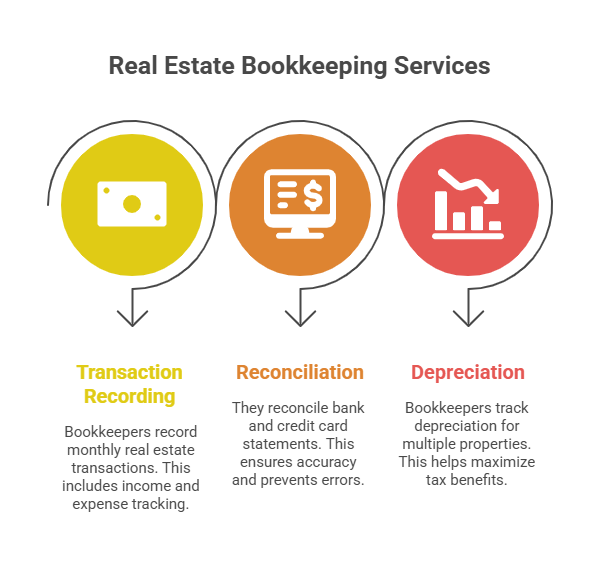

Specialized real estate bookkeepers handle monthly transaction recording, property-level income and expense tracking, bank and credit card reconciliation, accounts payable and receivable management, security deposit accounting, depreciation schedule maintenance, financial reporting for each property, and year-end tax preparation support.

They create systems showing which properties generate profit and which drain resources.

Property-level bookkeeping represents the foundation of effective real estate accounting. Each rental property needs separate tracking for income (rent, late fees, parking charges) and expenses (maintenance, utilities, insurance, property taxes, HOA fees). When you own properties across Charlotte, Asheville, and Wilmington, combined bookkeeping hides performance differences that drive investment decisions. Proper bookkeeping reveals that your Charlotte duplex generates 12% returns while your Wilmington condo barely breaks even after accounting for all costs.

Monthly reconciliation prevents the accumulation of errors that become disasters at tax time. Real estate bookkeepers match bank statements, credit card charges, and vendor invoices to general ledger entries, catching duplicate payments, missed expenses, and unauthorized charges. This discipline identifies issues immediately, discovering a $2,400 duplicate insurance payment in March allows correction before it affects cash flow planning or tax calculations.

Depreciation tracking becomes critical for North Carolina investors managing multiple properties. Residential rentals depreciate over 27.5 years, but improvements have different schedules depending on classification. A $350,000 rental property generates roughly $12,700 in annual depreciation, reducing taxable income significantly. For investors with growing portfolios, understanding depreciation strategies including bonus depreciation helps maximize tax benefits while maintaining accurate records for eventual property sales and recapture calculations.

Professional bookkeepers establish separate accounting classes or divisions for each property, use consistent chart of accounts across the portfolio, generate property-level profit-and-loss statements, create consolidated reports showing total portfolio performance, and maintain detailed transaction records supporting tax deductions. This structure provides both granular detail and big-picture visibility.

Most successful NC real estate bookkeepers use QuickBooks Online Plus with class tracking or property management software like Buildium, AppFolio, or Rent Manager. These systems assign every transaction to a specific property, enabling reports showing individual property performance.

When your Charlotte fourplex shows declining net operating income while your Raleigh single-family rentals perform strongly, this data-driven insight guides strategic decisions about selling, refinancing, or repositioning underperforming assets.

For investors managing 5+ properties or those planning rapid growth, outsourcing bookkeeping to specialized providers delivers consistent monthly financial statements without hiring full-time staff. This approach works particularly well for out-of-state investors owning NC properties remotely, professional bookkeepers handle transaction recording, vendor payments, and financial reporting while you focus on acquisitions and tenant management from anywhere.

Consolidated reporting shows portfolio-level metrics essential for growth planning. Total rental income, aggregate operating expenses, combined cash flow, and overall return on investment reveal whether your real estate business achieves financial goals. Banks and lenders reviewing refinancing applications or acquisition financing need these consolidated reports showing stable income and professional management, documentation that separates successful loan applications from rejections.

North Carolina taxes rental income at a flat 4.75% state rate, plus federal obligations. Real estate bookkeepers must track documentation supporting all deductions, maintain records for NC Department of Revenue requirements, handle property tax payments varying significantly by county, and prepare information for both federal Schedule E and NC D-400 state returns.

North Carolina's flat tax simplifies calculations compared to graduated-rate states, but deduction documentation remains critical. Every expense claimed reduces taxable income at the 4.75% state rate plus your federal marginal rate. A $10,000 properly documented repair deduction saves $475 in NC tax plus $2,200-$3,700 in federal tax depending on your bracket. Bookkeepers maintain receipts, invoices, and documentation defending these deductions during audits.

Property tax rates vary dramatically across North Carolina counties. Mecklenburg County (Charlotte) charges roughly $1.03 per $100 of assessed value, while Wake County (Raleigh) charges about $0.72 per $100. Coastal counties like New Hanover (Wilmington) can exceed $0.60 per $100. Bookkeepers track these payments, ensure timely payment avoiding penalties, and categorize them properly as fully deductible operating expenses on both federal and state returns.

Transfer taxes apply when buying or selling NC real estate, with rates varying by jurisdiction. Most counties charge $1 per $500 of consideration ($2 per $1,000), but bookkeepers document these costs as part of acquisition basis or selling expenses, affecting depreciation calculations for purchases and capital gains for sales. Proper categorization ensures you don't miss deductions or miscalculate taxable gains.

Effective tracking requires recording all rent payments with dates and payment methods, photographing and categorizing expense receipts immediately, separating capital improvements from repairs, maintaining security deposit records in liability accounts, and documenting mileage for property-related travel. Organized systems prevent the year-end scramble to recreate records.

Rent collection documentation must show payment dates, amounts, late fees assessed, and partial payment applications. North Carolina law allows landlords to charge late fees if specified in leases, but these fees count as taxable income. Bookkeepers record late fees separately from base rent, ensuring accurate income reporting and providing data showing payment patterns that inform tenant screening and lease renewal decisions.

The repair versus improvement distinction significantly impacts taxes. Repairs maintain property condition and are immediately deductible, fixing a leaky roof, replacing a broken HVAC unit, repainting walls. Improvements add value or extend property life and must be depreciated, installing a new roof, adding a room, complete kitchen renovation. NC bookkeepers properly classify these transactions, ensuring maximum current-year deductions while maintaining accurate depreciation schedules for improvements.

Security deposit accounting creates liability issues if mishandled. North Carolina requires landlords to deposit tenant security deposits in trust accounts at North Carolina-based banks within 30 days of receiving them, and return deposits within 30 days of lease termination with itemized deduction statements. Bookkeepers maintain separate liability accounts tracking deposits, record proper deductions for damages, and ensure compliance with NC General Statutes Chapter 42, Article 6, protecting landlords from penalties and litigation.

Investors should consider professional bookkeeping when acquiring their second rental property, if spending 10+ hours monthly on financial record-keeping, when facing late filing penalties or estimated tax issues, if unable to answer basic questions about property performance, or when planning portfolio expansion requiring investor-ready financial statements.

Single-property landlords can often manage basic bookkeeping using property management software with accounting features. Once you own 2-3 properties, complexity increases exponentially, multiple bank accounts, numerous vendor payments, property-specific expense categorization, and consolidated reporting requirements justify professional help. The 12-15 hours monthly you'll save redirects toward finding deals, managing tenants, or growing your business, activities generating more value than data entry.

Chronic estimated tax payment issues signal the need for professional bookkeeping. North Carolina requires quarterly estimated payments if you expect to owe $1,000+ in state tax. Real estate investors with variable income, large capital gain one quarter, rental losses the next, need accurate quarterly projections preventing underpayment penalties. Understanding proactive tax planning strategies helps investors minimize quarterly payments while avoiding penalties through proper timing and documentation.

Investors seeking financing for acquisitions or refinancing need professional financial statements. Banks reviewing loan applications expect property-level income statements, consolidated portfolio summaries, detailed rent rolls, and trend analysis showing stable or growing income. DIY bookkeeping in spreadsheets doesn't meet lender standards. Professional bookkeepers using recognized accounting software produce financial statements that satisfy underwriters and improve approval odds.

Growth-focused investors planning to scale from 5 properties to 15-20 units need systems supporting expansion. Professional bookkeepers establish scalable processes, standardized charts of accounts, and reporting templates that accommodate portfolio growth without requiring system overhauls. This foundation supports strategic planning, showing how many properties you need to quit your W-2 job or when portfolio income justifies hiring property management help.

North Carolina real estate bookkeeping costs vary by portfolio complexity. Single-property landlords typically pay $150-$300 monthly for basic bookkeeping. Investors with 3-5 properties spend $400-$700 monthly. Larger portfolios (8-15 properties) cost $800-$1,500 monthly. Property management companies with 50+ doors might invest $2,000-$4,000 monthly for comprehensive bookkeeping and financial reporting.

Pricing models include per-property monthly fees ($75-$150 per property), hourly rates ($40-$75/hour for basic bookkeepers, $75-$150/hour for CPAs), or flat monthly retainers covering specified services. Most NC bookkeepers use monthly retainers for predictable budgeting, with per-property pricing for larger portfolios providing cost transparency and scalability.

Tax preparation adds separate costs beyond monthly bookkeeping. Single Schedule E with one rental property costs $300-$600. Investors with 3-5 properties on Schedule E pay $600-$1,200. Complex returns involving multiple LLCs, partnerships, or S-corporations range from $1,500-$4,000+ depending on entity count and transaction complexity. Combined bookkeeping and tax packages often provide better value than separate services.

Charlotte and Raleigh rates typically run 10-20% higher than smaller markets like Greenville or Fayetteville, reflecting higher local business costs. However, location matters less now with remote bookkeeping capabilities. Many NC investors use bookkeepers outside their local market, accessing specialized expertise at competitive rates. For complex portfolios requiring significant monthly work, reviewing comprehensive outsourcing cost structures helps investors evaluate value and identify potential savings.

Madras Accountancy provides specialized real estate bookkeeping and accounting services for North Carolina investors, landlords, property managers, and developers. We handle monthly property-level bookkeeping, multi-entity tax preparation, financial reporting, and strategic advisory for clients across Charlotte, Raleigh, Greensboro, and throughout North Carolina.

Our team understands NC-specific requirements including state tax compliance, varying property tax rates across counties, security deposit trust accounting rules, and local transfer tax documentation. We work with investors owning 2-50 properties, managing everything from single-family rentals to commercial developments. Monthly financial reporting shows property-level performance, consolidated portfolio views, and key metrics informing investment decisions.

We specialize in serving out-of-state investors owning NC properties remotely. Our systems provide the visibility and control needed when managing properties from California, New York, or internationally. Cloud-based accounting delivers real-time access to financial data, monthly statements, and documentation supporting tax planning conversations with your CPA or financial advisor.

Our offshore partnership model delivers CPA-supervised bookkeeping at costs significantly below traditional NC firms. We provide the same quality and accuracy as local accountants but at 40-50% lower monthly costs. This efficiency allows us to serve mid-sized portfolios (3-15 properties) that larger firms consider too small, while offering better value than local practices charging premium rates. We've processed thousands of rental property returns since 2015, developing expertise in real estate bookkeeping that drives client results.

Yes, property-level bookkeeping is essential for tax compliance and investment analysis. The IRS allows aggregating multiple properties on Schedule E, but you must track income and expenses separately for each property to properly calculate depreciation, evaluate performance, and support deductions during audits. Property-level detail also helps identify underperforming assets and informs decisions about selling, refinancing, or improving specific properties.

Keep tax returns and supporting documentation for at least seven years. The IRS can audit up to six years back for substantial underreporting. For records related to property acquisition, improvements, and depreciation, maintain files until seven years after you sell the property, these documents affect capital gains calculations and depreciation recapture. North Carolina doesn't impose additional retention requirements beyond federal guidelines.

Yes, bookkeeping fees are fully deductible as ordinary and necessary business expenses for rental property operations. Whether you pay a local bookkeeper, use online services, or engage a CPA firm, these costs reduce your taxable rental income on both federal Schedule E and your NC D-400 state return. The same applies to tax preparation fees directly related to your rental properties.

Bookkeepers handle daily transaction recording, bank reconciliation, financial statement preparation, and accounts payable/receivable management. CPAs provide tax planning, prepare tax returns, offer strategic advisory, represent you during IRS audits, and make complex tax elections. Most real estate investors use bookkeepers for monthly work and CPAs for tax preparation and planning. Many firms, including Madras Accountancy, offer both services in an integrated package.

Most small landlords use cash basis accounting, recognizing income when received and expenses when paid. This simpler method works well for straightforward rental operations and is acceptable to the IRS for most real estate investors. Accrual accounting, which recognizes income when earned and expenses when incurred, provides more accurate monthly financial pictures but adds complexity. Larger landlords or property management companies might benefit from accrual accounting for better financial visibility.

Short-term rentals (less than 7 days average stay) require different tax treatment. Income reports on Schedule C instead of Schedule E, changing how expenses and losses are treated. NC bookkeepers track rental days versus personal use days, if personal use exceeds 14 days or 10% of rental days, deductions are limited. They also monitor occupancy tax obligations varying by jurisdiction, many NC coastal counties and mountain areas charge 6% occupancy tax on short-term rentals, requiring separate registration and remittance.

QuickBooks Online Plus handles multiple properties well with class tracking and works seamlessly with most CPAs. Property management platforms like Buildium, AppFolio, or Rent Manager combine tenant management with integrated accounting. Stessa offers free investor-focused accounting for smaller portfolios. The best choice depends on property count, whether you self-manage or use property managers, and integration needs with banking and tax preparation software.

Yes, we provide integrated bookkeeping and tax services for North Carolina real estate investors. Our monthly bookkeeping ensures accurate, audit-ready records throughout the year. This seamless data flow to tax preparation prevents year-end surprises, enables proactive tax planning, and delivers completed returns efficiently. Clients working with one provider for both services benefit from consistent record-keeping, better communication, and lower combined costs compared to using separate bookkeepers and tax preparers.

Madras Accountancy specializes in bookkeeping and accounting for North Carolina real estate investors, landlords, and property managers. Our team provides property-level financial tracking, monthly reporting, tax preparation, and strategic guidance for clients across Charlotte, Raleigh, Greensboro, and statewide. We deliver CPA-supervised bookkeeping at competitive rates through our efficient offshore model, serving portfolios from 2 to 50+ properties. Schedule a free consultation to discuss how we streamline your bookkeeping, improve financial visibility, and support your North Carolina real estate investment goals.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.