What Makes Hawaii Rental Property Bookkeeping Different?

Hawaii rental property bookkeeping requires tracking three separate taxes, General Excise Tax (GET) at 4-4.712%, Transient Accommodations Tax (TAT) rising to 11% in 2026, and county TAT surcharges of 3%, totaling 18-19% on short-term rentals. Unlike mainland states, Hawaii doesn't allow platforms like Airbnb to collect taxes for hosts. Property owners must register separately for GET and TAT licenses, file monthly or quarterly returns, and maintain detailed records separating tax

collections from rental income to avoid cascading tax-on-tax calculations.

You just bought a vacation rental in Maui. Your first guest checks out, pays $3,000 for the week. You think you made $3,000. Wrong. After GET (4.712%), state TAT (10.25%), and Maui County TAT (3%), you owe $537.96 in taxes, 18% of your gross rental income. And because you didn't separately itemize these taxes on the booking, Hawaii's tax-on-tax rules mean you actually owe more.

Welcome to Hawaii rental property bookkeeping. The state's unique tax structure, no sales tax but multiple gross receipts taxes, creates complexity that mainland property accounting never encounters. Miss a filing deadline? There's no statute of limitations on GET or TAT. Those penalties compound indefinitely.

Hawaii rental properties face tax requirements unlike any other state. The General Excise Tax applies to all business activity at 4% statewide plus 0.5% county surcharges (4.5% on Oahu, 4.712% on Maui when calculated correctly). This isn't a sales tax, it's a gross receipts tax on your business activity, meaning it applies to total rental income before expenses.

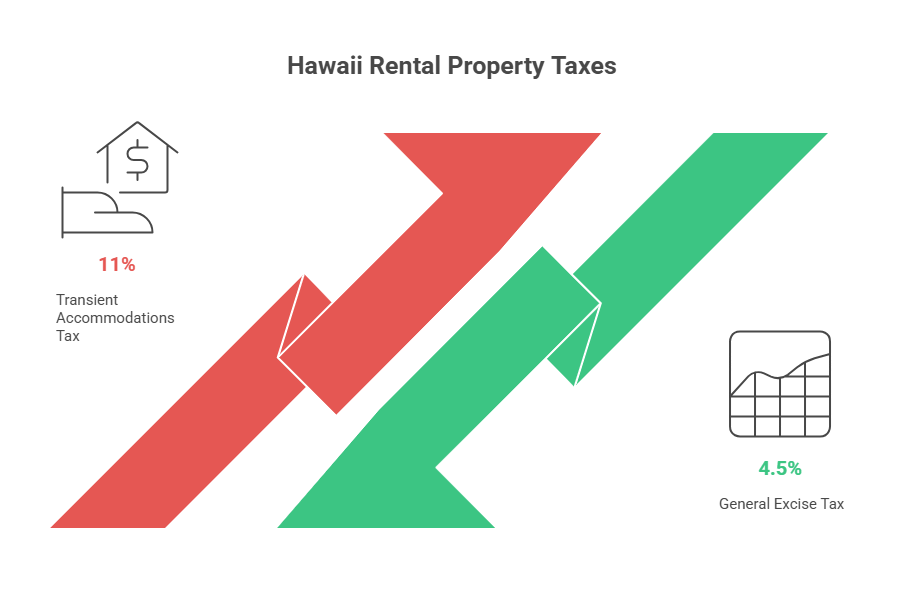

The Transient Accommodations Tax adds another layer. Currently 10.25% statewide, TAT increases to 11% on January 1, 2026, with the extra 0.75% dedicated to an environmental fund. TAT applies to rentals under 180 consecutive days, capturing vacation rentals, Airbnb listings, and short-term property management income. Since 2019, TAT extends to "all required charges and fees," including cleaning fees that many owners mistakenly exclude.

County TAT surcharges compound the burden. Maui County charges 3%, Honolulu County 3%, Kauai County 3%, and Hawaii County 3% on top of state rates. A Maui vacation rental faces combined taxes of approximately 18% (4.712% GET + 10.25% state TAT + 3% county TAT) before the 2026 increase.

The tax-on-tax problem creates calculation nightmares. If you don't separately itemize GET and TAT from rental charges, Hawaii requires you to calculate tax on the tax amount. Charge $1,000 rent without separation? GET applies to the full $1,000 including TAT, and TAT applies to the full amount including GET. Properly separating these prevents cascading tax calculations that inflate your liability 1-2%.

Registration requirements differ from mainland states. You need separate Hawaii Tax ID numbers for GET and TAT, obtained through the Hawaii Basic Business Application. GET registration costs $20, TAT registration runs $5 for 1-5 units or $15 for 6+ units. Most mainland platforms don't handle Hawaii's split tax registration, forcing manual compliance.

Understanding basic bookkeeping fundamentals becomes essential when Hawaii's unique tax structure requires more sophistication than simple rent tracking.

General Excise Tax functions differently than sales tax despite similar rates. GET taxes your gross rental receipts as business income, not the transaction itself. You pay GET whether you pass the cost to tenants or absorb it yourself. The base rate is 4% statewide, with county surcharges bringing Oahu to 4.5% and Maui to an effective 4.712% when calculated through Hawaii's pyramiding method.

GET applies to all rental income, long-term and short-term. A year-long apartment lease? Subject to GET. A one-night vacation rental? Also GET, plus TAT. The first $2,000 of annual rental income from residential property qualifies for GET exemption, but this rarely applies to active vacation rental businesses generating monthly income well above this threshold.

Transient Accommodations Tax specifically targets short-term lodging. TAT's 10.25% state rate (11% starting January 2026) applies only to rentals under 180 consecutive days. The distinction matters: rent an apartment for seven months, you pay only GET. Rent that same space nightly on Airbnb, you pay both GET and TAT on every booking.

Cleaning fees complicate TAT calculation. Pre-2019, many hosts excluded cleaning fees from TAT, treating them as service charges. Hawaii closed this loophole, all "required charges and fees" now fall under TAT. A $200 cleaning fee on a $1,000 rental means TAT applies to the full $1,200, not just the rental portion.

County TAT surcharges started in 2021 after legislation allowed counties to impose additional transient accommodation taxes. All four counties implemented 3% surcharges, collected separately from state TAT. Hosts file state TAT returns but pay county portions directly to county tax authorities, a split filing process unique to Hawaii creating additional administrative burden.

Filing frequencies depend on your tax liability. Businesses owing under $4,000 annually file GET and TAT semi-annually. Between $4,000-$12,000 annually, you file quarterly. Above $12,000, monthly filing becomes mandatory. Most active vacation rentals hit monthly filing thresholds within 3-4 months of operation.

Separate tax tracking prevents the most expensive Hawaii rental bookkeeping errors. Create distinct accounts for GET collected, state TAT collected, and county TAT collected. Never mix these with rental income. When a guest pays $1,180 for a $1,000 rental ($47.12 GET + $102.50 state TAT + $30 county TAT + $1,000 rent), your books should reflect four separate line items.

Guest payment detail matters more in Hawaii than other states. Record each booking with gross rental amount, cleaning fee amount, GET charged, state TAT charged, and county TAT charged separately. This granularity proves essential during tax filing and protects against IRS scrutiny when expenses exceed income due to high tax pass-through.

Expense categorization requires property-level specificity. Hawaii allows rental property expense deductions against rental income, but categories matter for depreciation and passive activity loss rules. Track mortgage interest, property management fees, maintenance, utilities, insurance, property taxes, and marketing costs separately. Improvements over $2,500 must be capitalized and depreciated rather than expensed immediately.

Monthly reconciliation catches filing errors before they compound. Compare your GET and TAT collected accounts against filed returns monthly. A $50 variance in month one becomes $600 annually plus penalties. Hawaii's no-statute-of-limitations rule on unfiled or underpaid GET/TAT means errors from 2020 remain collectible indefinitely.

Documentation supports deduction claims during audits. Hawaii rental property owners should maintain rental agreements, payment receipts, expense invoices, property management contracts, maintenance records, and annual form 1099s for contractors. The IRS audits vacation rental income aggressively, proper documentation separates legitimate deductions from red flags.

Software integration streamlines Hawaii's complex requirements. Property management platforms like Buildium, AppFolio, or Guesty connect with QuickBooks Online or Xero to automate transaction imports. However, most platforms don't automatically separate Hawaii's three-tier tax structure, requiring manual account mapping during setup.

Implementing proper cash flow management helps vacation rental owners handle Hawaii's high tax burden alongside seasonal booking fluctuations common in resort markets.

Failing to register for GET and TAT before first rental. Many new investors collect rent before obtaining Hawaii Tax IDs, creating immediate non-compliance. Hawaii requires registration before you furnish your first transient accommodation. Operating without licenses subjects you to penalties from day one, with no statute of limitations on collection.

Mixing personal and rental finances. Using personal accounts for rental income and expenses creates audit disasters. Hawaii tax authorities expect clear separation between personal and business transactions. Co-mingled funds complicate expense deduction substantiation and raise red flags during examinations.

Not separately stating taxes on invoices. Charge one lump sum of $1,180 without itemizing $47.12 GET, $102.50 TAT, $30 county TAT, and $1,000 rent? Hawaii considers this a $1,180 rental subject to GET on the full amount, creating tax-on-tax calculations increasing your liability 15-18%. Always separately state each tax component.

Excluding cleaning fees from TAT. The 2019 rule change requiring TAT on all required fees catches many hosts. Cleaning fees, resort fees, and mandatory service charges all fall under TAT now. Excluding them from TAT calculations creates underpayment that compounds with penalties and interest over time.

Missing county TAT filing deadlines. State TAT returns file with Hawaii Department of Taxation, but county TAT payments go directly to county treasurers. This split filing creates missed deadlines when owners file state returns but forget separate county payments. Each county has distinct payment portals and procedures.

Incorrect filing frequency. Underestimating annual tax liability leads to filing semi-annually when monthly filing is required. Hawaii assesses penalties for wrong filing frequencies, not just late payments. Review your total annual GET and TAT quarterly to ensure you're on the correct schedule.

Not tracking basis for depreciation properly. Hawaii rental properties depreciate over 27.5 years for residential or 39 years for commercial. Your depreciable basis includes purchase price plus improvements, minus land value. Many owners fail to track improvement costs separately, losing deductions when properties sell.

Property management companies handling your bookkeeping should demonstrate Hawaii-specific expertise. Ask how they handle GET/TAT separation, county TAT filing, and tax-on-tax avoidance before signing contracts.

GET and TAT filing frequencies tie to your annual tax liability. Calculate expected annual GET and TAT combined:

Annual reconciliation happens on Form TA-2 for TAT, due April 20 for calendar-year filers. This reconciliation compares your monthly/quarterly filings against actual annual gross rental proceeds. Underpayments require payment with the reconciliation, while overpayments generate credits for future filings.

County TAT surcharge timing varies by county. Most follow state TAT filing frequencies but require separate payments to county treasurers. Maui County uses form HCTAT-RV for annual reconciliation. Hawaii County, Honolulu County, and Kauai County have similar county-specific forms and payment portals.

Federal tax reporting adds another layer. Rental income on Schedule E, depreciation calculations, and passive activity loss limitations all apply to Hawaii rentals. Form 1099-MISC goes to any contractor or property manager paid $600+ annually, due January 31 (to recipient) and February 28 (to IRS).

State income tax hits both residents and non-residents. Hawaii residents report all rental income on Hawaii state returns. Non-residents pay Hawaii state income tax only on Hawaii-source rental income, filing Form N-15 (nonresident return) annually. Hawaii's progressive tax rates range from 1.4% to 11% based on income brackets.

Penalty calculations compound quickly. Late filing penalties start at 5% of tax due per month, maxing at 25%. Late payment penalties add another 20%. Interest accrues daily at rates adjusted quarterly. A $5,000 underpayment from six months prior could cost $2,000+ in penalties and interest.

Managing small business tax compliance becomes critical when juggling Hawaii's state GET, state TAT, county TAT, federal, and state income tax deadlines across multiple properties.

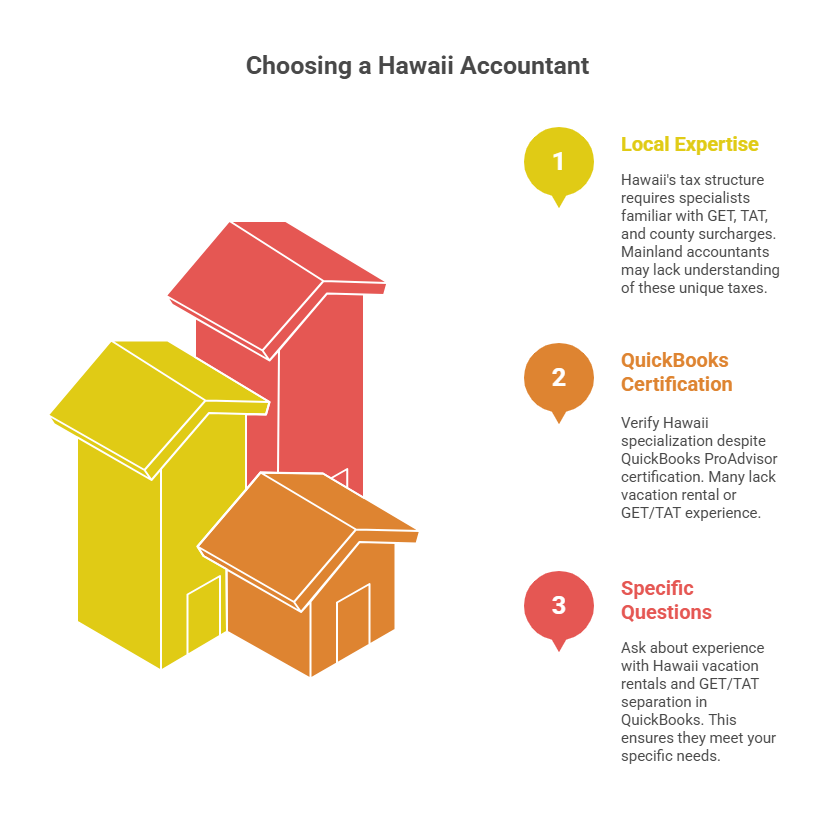

Local expertise matters more than national accounting firm size. Hawaii's unique tax structure, GET, TAT, county surcharges, requires specialists who handle these taxes daily. A mainland accountant familiar with sales tax won't understand GET's gross receipts application or tax-on-tax prevention strategies.

QuickBooks ProAdvisor certification indicates platform expertise, but verify Hawaii specialization. Many bookkeepers hold ProAdvisor status without vacation rental or GET/TAT experience. Ask specifically: "How many Hawaii vacation rental clients do you serve?" and "How do you handle GET/TAT separation in QuickBooks?"

Property management companies often include bookkeeping but verify scope. Full-service property managers typically handle guest payments, tax collection, and basic income/expense tracking. However, many don't prepare monthly financial statements, manage owner distributions, or handle annual tax return preparation. Clarify what's included versus what requires separate accounting fees.

Pricing structures vary significantly across providers. Hourly billing ($75-150/hour) creates unpredictable costs. Fixed monthly fees ($200-500/property) provide budget certainty for ongoing bookkeeping. Annual tax preparation adds $500-1,500 depending on entity complexity and property count. Multi-property portfolios often negotiate volume discounts.

Technology capabilities separate efficient from outdated providers. Cloud-based systems (QuickBooks Online, Xero) allow real-time access from anywhere. Integration with property management platforms (Hostfully, Guesty, Hospitable) automates transaction imports. Providers still requesting monthly spreadsheets or using desktop software create unnecessary manual work.

Review sample financial statements before committing. Quality bookkeepers deliver property-level income statements, balance sheets, and tax summary reports showing GET/TAT collected versus filed. Reports should clearly separate rental income from tax collections and provide enough detail for tax preparation and investment analysis.

Response time expectations matter for vacation rental operations. Monthly bookkeeping services typically close books by the 10th of the following month. Tax preparation should provide draft returns at least two weeks before filing deadlines, allowing review time. Emergency questions during tax season should receive responses within 24-48 hours.

Local Hawaii bookkeepers offer in-person consultations and deep market knowledge. They understand county-specific regulations, maintain relationships with Hawaii tax authorities, and often handle multiple properties in your area. Local providers attend Hawaii real estate events, stay current on county rule changes, and can visit properties if documentation issues arise.

However, local providers cost 40-60% more than remote alternatives. Hawaii's high cost of living translates to $100-150 hourly rates versus $60-90 for mainland providers. Monthly bookkeeping for a single vacation rental costs $300-500 locally versus $150-250 remotely. The premium buys local expertise but may not justify costs for straightforward properties.

Remote bookkeeping services deliver competitive pricing through lower overhead and often offer specialized vacation rental expertise from serving clients nationwide. Cloud-based platforms make geography irrelevant, a Boise-based bookkeeper accesses your QuickBooks Online as easily as a Honolulu provider. Remote teams often provide faster turnaround, leveraging multiple time zones for 24-hour coverage.

The trade-off involves Hawaii-specific knowledge gaps. Mainland bookkeepers may not immediately recognize GET/TAT separation requirements or county TAT filing procedures. They might miss Hawaii-only deductions like general excise tax expense write-offs or mishandle the first $2,000 GET exemption. Verify any remote provider's Hawaii rental experience before onboarding.

Hybrid approaches combine benefits of both. Some investors use local Hawaii CPAs for annual tax strategy and return preparation ($1,500-3,000 annually) while outsourcing monthly bookkeeping to remote providers ($150-250/month). This balances cost efficiency with access to Hawaii expertise for complex tax planning.

Offshore accounting teams represent the cost-effective extreme, delivering specialized vacation rental bookkeeping at 40-50% below U.S. rates. Providers like Madras Accountancy (established 2015) serve U.S. property investors with bookkeeping teams handling QuickBooks setup, monthly reconciliation, and financial reporting for Hawaii and mainland rentals. The model works through U.S. CPA oversight of offshore execution, maintaining quality while reducing costs.

Understanding the ROI of outsourcing accounting services helps Hawaii rental owners evaluate whether cost savings from remote or offshore bookkeeping justify any trade-offs in local market knowledge.

QuickBooks Online remains the most common platform for Hawaii vacation rental bookkeeping, offering property management integrations, mobile access, and accountant collaboration. The Plus plan ($90/month) handles most single-property needs with class tracking for multiple units. Advanced plan ($200/month) adds inventory tracking and project profitability for larger portfolios.

Xero provides similar capabilities at competitive pricing ($13-70/month) with particularly strong bank reconciliation features. Xero's unlimited user access benefits property management teams, allowing bookkeepers, owners, and CPAs simultaneous access without per-user fees. The platform integrates with major vacation rental channels through third-party apps.

Property-specific platforms like Guesty, Hostfully, and Hospitable manage bookings, guest communications, and channel distribution while syncing financial data to accounting software. These typically cost $30-50 per property monthly but eliminate manual transaction entry. They don't handle GET/TAT calculations automatically, you'll configure rules within your accounting software.

Separate tax tracking apps address Hawaii's complexity. Some bookkeepers build custom spreadsheets for GET/TAT calculations before importing to QuickBooks. Others use rental-specific software like Stessa (free for basic tracking) or Baselane ($10-25/month) that attempts Hawaii tax separation but requires verification given frequent rule changes.

Automated bank feeds reduce reconciliation time by 10-15 hours monthly. Connect checking accounts, credit cards, and property management platforms directly to your accounting software. Transactions import automatically for categorization rather than manual entry. This automation matters more for Hawaii rentals given the tax separation requirements on every booking.

Custom reporting requirements often exceed out-of-box capabilities. Hawaii investors need reports showing NET rental income after GET/TAT (not gross), property-level profitability, and tax summary reports tracking GET/TAT collected versus filed. Most platforms require custom report configuration or third-party apps like Fathom or LivePlan for sophisticated analytics.

Security considerations matter when granting bookkeeper access. Cloud platforms offer granular permission controls, accountants can access financial data without ability to approve payments or modify core settings. Two-factor authentication protects against unauthorized access to sensitive tax information and financial records.

Do I need separate bank accounts for each Hawaii rental property?

Not legally required, but strongly recommended for properties owned in separate LLCs or with different partners. Separate accounts simplify bookkeeping by providing clear transaction trails per property. For multiple properties under one ownership entity, you can use a single bank account with class tracking in QuickBooks or Xero to separate income and expenses by property. The key is maintaining clear records that allocate every transaction to specific properties.

How do platforms like Airbnb and VRBO handle Hawaii GET and TAT?

Unlike most states, Hawaii doesn't allow Airbnb or VRBO to collect and remit taxes on your behalf. You must collect GET and TAT from guests yourself and file returns with Hawaii tax authorities. Platforms provide booking management but tax compliance remains your responsibility. Many hosts use platform integrations with accounting software to automate tax calculations on each booking, then file returns directly with the state and counties.

What happens if I miss a Hawaii GET or TAT filing deadline?

Hawaii assesses penalties of 5% per month for late filing (maxing at 25%) plus 20% for late payment. Interest accrues daily at quarterly-adjusted rates. More concerning: Hawaii has no statute of limitations on GET or TAT. Unfiled returns from 2015 remain collectible in 2025 with accumulated penalties and interest. The state regularly audits vacation rental properties and can assess taxes retroactively for all years without filings. File and pay on time, always.

Can I deduct GET and TAT as business expenses on my federal return?

Yes. GET and TAT you pay (not collect from guests) are deductible business expenses on Schedule E. If you pass these taxes to guests as separate charges, those amounts are rental income to you and the taxes you remit are deductible expenses, they offset each other. If you absorb the taxes without passing them to guests, they're deductible business expenses reducing your net rental income. Track these carefully, $10,000 in annual taxes creates $2,500-3,500 in federal tax savings at typical marginal rates.

Do long-term Hawaii rentals avoid TAT requirements?

Yes. Leases of 180 consecutive days or longer avoid TAT entirely, you only pay GET on long-term residential rentals. However, the GET rate differs: long-term residential rentals pay 0.5% GET (plus county surcharge) after a $2,000 annual exemption, versus 4% GET for commercial and vacation rental activities. If you switch a property between long-term and short-term use, track rental periods carefully to apply correct tax treatment.

Should Hawaii vacation rentals be in separate LLCs?

Most real estate attorneys recommend separate LLCs for asset protection, lawsuits against one property don't threaten others. This creates bookkeeping complexity requiring entity-level accounting and separate GET/TAT registrations per LLC. The accounting cost ($500-1,000 per entity annually) usually justifies the protection for properties with significant equity. Some owners use umbrella insurance instead for lower-value properties, avoiding multi-entity accounting costs.

How do offshore bookkeeping services work for Hawaii rentals?

Offshore providers like Madras Accountancy assign dedicated bookkeepers familiar with Hawaii GET/TAT requirements. You grant cloud accounting software access, connect bank feeds and property management platforms, and the offshore team handles monthly reconciliation, transaction categorization, and financial statement preparation. U.S. CPAs review deliverables for quality control. The model reduces bookkeeping costs 40-50% versus local providers while maintaining Hawaii compliance expertise through systematic processes and U.S. oversight.

What records should I keep for Hawaii rental property audits?

Maintain all rental agreements, guest booking confirmations, payment receipts, monthly GET/TAT filing confirmations, expense invoices, bank and credit card statements, property management contracts, and annual 1099 forms. Hawaii and IRS both recommend keeping records 7+ years given audit windows. Cloud storage (Google Drive, Dropbox) provides secure backup cheaper than physical files. During audits, Hawaii tax authorities specifically request GET/TAT calculation worksheets showing how you separated taxes from rental income.

Hawaii rental property bookkeeping demands more sophistication than mainland investments due to GET, dual TAT layers, and no-statute-of-limitations collection authority. The complexity creates opportunities for costly errors, tax-on-tax calculations, missed county TAT filings, wrong filing frequencies, that compound indefinitely under Hawaii law.

The investment in proper bookkeeping systems and expertise pays dividends through accurate tax compliance, maximized deduction claims, and audit protection. Whether choosing local Hawaii specialists, remote mainland providers, or offshore accounting teams, prioritize demonstrated Hawaii rental experience over generic bookkeeping capabilities.

Start with solid foundations: separate business accounts, proper GET/TAT registration, cloud accounting software with property management integration, and monthly reconciliation habits. These basics prevent the expensive errors that create problems years later when Hawaii tax authorities conduct compliance reviews.

For investors managing multiple Hawaii properties or those seeking cost-effective specialized support, offshore accounting partnerships deliver Hawaii rental expertise at reduced costs through systematic processes and technology integration. The key is matching service sophistication to your portfolio complexity while ensuring providers demonstrate specific Hawaii GET/TAT knowledge through client references and sample deliverables.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.