Direct Answer: Landlords overpay taxes by forgetting to claim depreciation, misclassifying repairs as improvements, failing to track expenses properly, and not utilizing cost segregation studies. The average property owner overpays $3,000-$12,000 annually by missing legitimate deductions that the IRS explicitly allows.

You've spent months finding the right rental property. You've navigated financing, tenant screening, and maintenance headaches. But when tax season arrives, you're likely making errors that cost thousands in unnecessary tax payments. While the IRS tax code offers substantial benefits to real estate investors, most landlords leave money on the table because they don't understand which deductions they qualify for or how to properly claim them.

Property owners owe taxes on their rental income, but taxable rental income should be significantly lower than gross rent collected. The gap between what you collect and what you actually owe taxes on depends entirely on how effectively you track and claim deductions.

According to IRS data, rental property owners can legally reduce their tax liability through depreciation, operating expenses, and strategic tax planning. Yet most landlords operate without a systematic approach to tax preparation, resulting in overpayment.

The problem starts with poor record-keeping. When you can't prove an expense occurred or can't demonstrate it's related to your rental property, you forfeit the deduction. The IRS requires documentation, receipts, bank statements, and clear categorization of every dollar spent on rental properties.

Here are the seven mistakes that cause landlords to overpay thousands in taxes annually:

1. Forgetting to Claim Depreciation

Depreciation is the single largest tax deduction available to property owners, yet many landlords forget to claim it. The IRS allows you to depreciate residential rental property over 27.5 years. For a property valued at $275,000 (excluding land), you can deduct $10,000 annually, even if the property is actually appreciating in value.

What makes this mistake particularly costly: If you don't claim depreciation, the IRS still considers you to have taken it when you sell the property. You face depreciation recapture taxes on depreciation you never actually deducted. This creates additional tax liability with zero benefit.

2. Misclassifying Repairs vs. Improvements

The distinction between repairs and improvements determines whether you deduct expenses immediately or depreciate them over 27.5 years. Repairs maintain the property's current condition and are fully deductible in the year incurred. Improvements increase the property's value and must be depreciated.

Examples of repairs: Fixing a leaky faucet, patching drywall, replacing broken windows. Examples of improvements: Installing a new roof, adding a deck, renovating a kitchen.

Many landlords misclassify repairs as improvements, unnecessarily delaying tax benefits. A $5,000 repair provides an immediate $5,000 deduction. The same amount classified as an improvement spreads that deduction over 27.5 years, just $182 annually.

3. Not Tracking All Deductible Expenses

Property owners routinely miss deductions because they don't track income and expenses throughout the year. Common overlooked deductions include:

Mortgage interest payments represent one of the largest deductions for landlords. Property tax payments are fully deductible. Insurance premiums for landlord liability, fire, flood, and theft coverage all qualify. Property management fees, whether you hire a company or pay for property management software, are deductible business expenses.

Travel expenses to and from your rental property for inspections, maintenance, or to collect rent are deductible at $0.70 per mile in 2025. Professional fees for CPAs, attorneys, and consultants who help with your rental business qualify. Advertising costs to find tenants, including listing fees and background check services, reduce your taxable income.

Without proper tracking, these expenses disappear. Working with tax planning professionals who understand rental property taxation helps ensure nothing falls through the cracks.

4. Failing to Use Cost Segregation Studies

Cost segregation accelerates depreciation by identifying property components that qualify for shorter depreciation schedules. While the building structure depreciates over 27.5 years, certain components qualify for 5, 7, or 15-year schedules.

A cost segregation study performed by a qualified professional can reclassify 20-40% of a property's value into faster depreciation categories. For a $500,000 property, this strategy creates immediate tax deductions of $50,000-$75,000 instead of spreading deductions over decades.

This strategy works particularly well for properties with significant improvements or commercial properties with specialized systems.

5. Ignoring the Real Estate Professional Status

Most rental income is classified as passive, meaning you can't deduct passive losses against earned income like wages. However, if you qualify as a real estate professional under IRS rules, you can deduct rental losses against all income types.

To qualify, you must spend more than 750 hours annually in real property trades or businesses, and more than half your working hours in those activities. You must also maintain detailed records proving material participation in your rental activities.

Real estate professional status can save high-income landlords $15,000-$50,000 annually by unlocking passive loss deductions that would otherwise be suspended until property sale.

6. Not Utilizing 1031 Exchanges

When you sell rental property, capital gains tax on appreciation can consume 15-20% of your profit, plus depreciation recapture at 25%. A 1031 Exchange allows you to defer capital gains taxes by reinvesting proceeds into replacement properties of equal or greater value.

The exchange must involve like-kind properties (residential rental for residential rental, commercial for commercial). You have 45 days after closing to identify replacement properties and 180 days to complete the purchase.

Many landlords sell properties without considering 1031 Exchanges, immediately triggering substantial tax bills. The right CPA who specializes in real estate taxation structures these transactions to maximize tax deferral.

7. Filing Taxes Without Professional Guidance

Rental property taxation is complex. Schedule E reporting requires understanding passive activity rules, depreciation schedules, and proper expense categorization. The tax law changes frequently, bonus depreciation rules, qualified business income deductions, and state-specific regulations all affect your tax bill.

DIY tax preparation software helps with basic returns but lacks the strategic tax planning that reduces liabilities long-term. Tax professionals identify deductions you don't know exist and structure your rental business for maximum tax efficiency.

Start by implementing better systems. Track every rental-related expense from day one. Use dedicated bank accounts for rental activity. Save all receipts, invoices, and documentation that proves expenses relate to your rental business.

Review your depreciation schedules annually. If you've forgotten to claim depreciation in previous years, you can file Form 3115 to catch up on missed deductions. Don't let years of unclaimed depreciation disappear.

Consider your entity structure. Holding properties in an LLC or S corporation may provide liability protection and tax advantages depending on your situation. The right structure varies based on income level, number of properties, and long-term strategy.

Maximize legitimate deductions by understanding what qualifies. The IRS allows deductions that are ordinary, necessary, and directly related to rental property management. When unsure whether something qualifies, consult with professionals who focus on tax preparation for real estate investors.

Plan for tax implications before making major decisions. Selling a property, making improvements, or changing how you use the property all trigger tax consequences. Strategic planning before these events saves substantially more than reactive tax preparation after the fact.

The IRS requires supporting documentation for all deductions claimed. Maintain organized records that prove the amount, date, and business purpose of each expense.

Essential records include: Bank statements showing rental deposits and expense payments. Receipts for repairs, maintenance, improvements, and supplies. Mileage logs documenting trips related to rental properties. Lease agreements and tenant correspondence. Documentation of depreciation calculations and asset purchases. Records of mortgage interest and property tax payments.

Keep these records for at least three years after filing, though seven years provides better protection if the IRS questions older returns. Digital record-keeping systems make organization easier and ensure documents don't disappear.

For landlords managing multiple properties or dealing with complex situations, outsourced bookkeeping services designed for rental property owners maintain accurate records year-round, eliminating the scramble at tax time.

While some landlords with single properties and straightforward situations can handle their own taxes, professional help becomes essential when:

You own multiple rental properties across different locations. You're considering cost segregation studies or 1031 Exchanges. You need to determine if you qualify as a real estate professional. You've made significant improvements requiring capitalization decisions. You're facing IRS audits or questions about previous returns.

Professional tax preparation costs $300-$1,500 annually depending on complexity, but the deductions identified typically far exceed the fee. Tax professionals also provide year-round advice that shapes better business decisions, not just historical tax reporting.

The savings potential depends on rental income, property values, and how many deductions you're currently missing. Conservative estimates suggest:

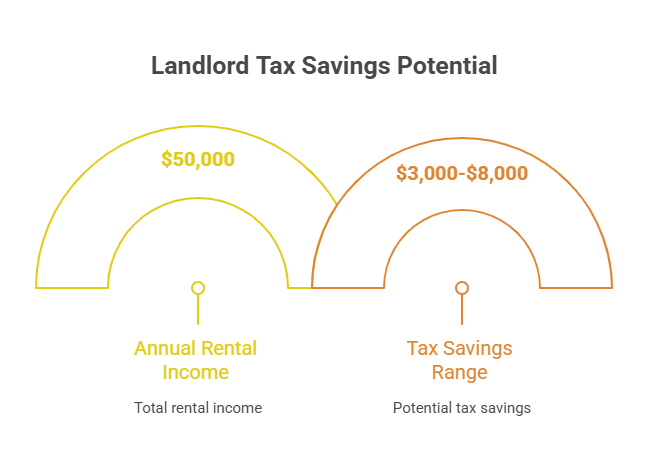

Landlords with $50,000 in annual rental income who properly claim all deductions save $3,000-$8,000 annually compared to incomplete tax filings. Landlords with $100,000+ in rental income using advanced strategies like cost segregation can save $12,000-$25,000 in the first year alone. Real estate professionals who unlock passive loss deductions save $15,000-$50,000 annually depending on income levels.

These aren't hypothetical savings, they represent real tax reductions achieved through legitimate IRS-approved strategies that most landlords simply don't know exist.

Yes, property tax paid on rental properties is fully deductible as a rental expense. This includes real estate taxes imposed by local governments. Report these on Schedule E as part of your annual rental expenses. Keep property tax bills and payment records as documentation.

The IRS still considers you to have taken depreciation even if you didn't claim it, creating a tax liability when you sell. You can file Form 3115 to catch up on missed depreciation for previous years. This prevents paying depreciation recapture taxes on deductions you never actually received.

Generally no, unless you qualify as a real estate professional or your income is below $100,000 (allowing up to $25,000 in passive loss deductions). Otherwise, rental losses can only offset other passive income. Unused losses carry forward to future years.

Repairs maintain current condition and are immediately deductible (fixing a broken window). Improvements enhance value, prolong life, or adapt property to new uses and must be depreciated (new roof). When uncertain, consult a tax professional before tax filing.

Yes, travel expenses for rental property management are deductible. This includes mileage at $0.70 per mile in 2025, or actual vehicle expenses. Deductible trips include inspections, maintenance, rent collection, and showing properties to prospective tenants. Maintain detailed mileage logs.

Cost segregation identifies property components eligible for accelerated depreciation, creating immediate tax savings. It's typically worthwhile for properties valued over $500,000 or with substantial improvements. The study costs $5,000-$15,000 but often saves $50,000+ in first-year taxes.

You can file amended returns for up to three years from the original filing date to claim missed deductions. For depreciation specifically, use Form 3115 to make a change in accounting method. Beyond three years, most opportunities to claim missed deductions disappear.

While not legally required, separate accounts make tracking rental income and expenses dramatically easier. Mixed personal and business transactions create record-keeping nightmares and make IRS audits more complicated. Separate accounts also strengthen the business legitimacy of your rental activity.

Most landlords overpay taxes because they don't fully understand the deductions available or lack systems to track expenses properly. The IRS tax code provides substantial benefits to rental property owners, but you must actively claim them, they don't appear automatically. Start by reviewing your last tax return. Identify which deductions you claimed and which you might have missed. Implement better record-keeping systems now to avoid overpaying on next year's taxes. For properties with significant value or complex situations, professional guidance from tax specialists who understand real estate taxation delivers returns that far exceed the cost. Since 2015, Madras Accountancy has helped property owners and real estate professionals navigate rental property taxation, identifying missed deductions and implementing strategies that legally reduce tax liabilities. Our team understands the specific challenges landlords face and provides year-round support beyond basic tax preparation.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.