Direct Answer: Form 8582 is the IRS form you must file to report passive activity losses, including rental real estate losses that exceed your passive income. It calculates how much of your rental loss you can deduct in the current tax year versus what must be carried forward. Most rental property owners with losses exceeding $25,000 (or any loss if your modified adjusted gross income is over $150,000) must file this form.

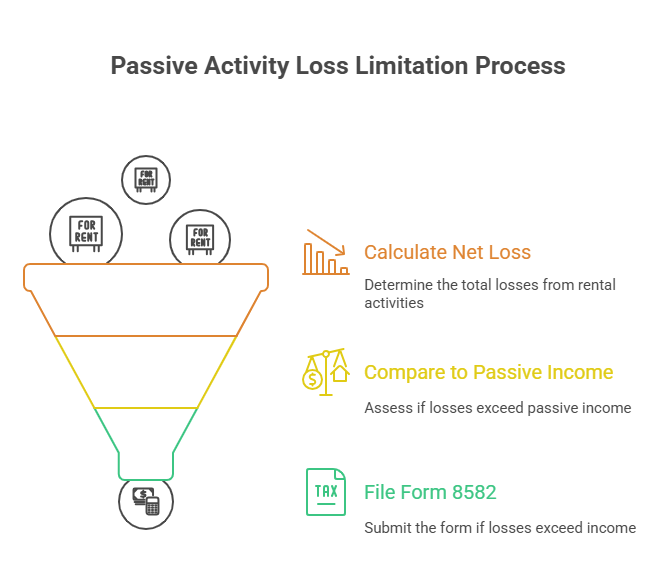

Form 8582 (Passive Activity Loss Limitations) is an IRS tax form that limits the amount of losses you can claim from passive activities, primarily rental properties. The IRS requires this form when your rental real estate activities generate a net loss that exceeds your passive income for the tax year.

You must file Form 8582 if you meet these conditions: you have a loss from rental activities, your modified adjusted gross income exceeds $100,000, or you have losses from multiple passive activities. The form applies to individuals, estates, trusts, and closely held corporations—anyone with passive activity losses must complete this form before claiming deductions on Form 1040.

Here's when you don't need Form 8582: if you have only passive income (no losses), if you actively participated in rental real estate with modified adjusted gross income under $100,000 and losses under $25,000, or if you qualify as a real estate professional under IRS guidelines.

The passive loss rules exist because the IRS wants to prevent taxpayers from using rental losses to offset wages or business income without genuine economic risk. Rental activities are automatically classified as passive activities, regardless of your participation level, unless you meet the real estate professional criteria.

The basic rule: you can only deduct passive losses up to the amount of your passive income. If you have $30,000 in rental losses but only $10,000 in passive income, you can deduct $10,000 this year. The remaining $20,000 becomes an unallowed loss that carries forward to future tax years.

There's one important exception—the $25,000 special allowance for rental real estate. If you actively participated in rental real estate activities (making management decisions, approving tenants, setting rental terms), you can deduct up to $25,000 in losses against your ordinary income. This allowance phases out for married individuals who file separate returns and those with modified adjusted gross income between $100,000 and $150,000.

The special allowance for rental real estate gives qualifying taxpayers a break from strict passive loss limitation rules. You can claim up to $25,000 in rental losses against your non-passive income if you actively participated in rental real estate activities during the tax year.

"Active participation" is easier to meet than you think. You don't need to perform physical work on the property. Making management decisions counts—approving new tenants, deciding on repairs, setting rental rates, or reviewing monthly statements. Most landlords who own and manage their properties (even through a property manager) qualify.

The catch: this allowance phases out dollar-for-dollar when your modified adjusted gross income exceeds $100,000. At $150,000 or higher, the allowance disappears completely. For example, with $120,000 in modified adjusted gross income, your allowance reduces to $15,000 ($25,000 minus half of the $20,000 excess over $100,000).

Start with Worksheet 1 from the IRS Form 8582 instructions. List each rental property separately, showing the current year's net income or loss from Schedule E. Calculate your prior year unallowed losses—these are losses from previous years that you couldn't deduct because they exceeded your passive income.

Move to Part I of Form 8582. Enter your total loss from all passive activities on line 1. Lines 2 and 3 calculate your special allowance based on modified adjusted gross income. The form automatically reduces your allowance if your income falls between $100,000 and $150,000. Line 4 shows the allowable passive activity loss limit—this is the maximum deduction you can claim this year.

Part II handles rental real estate activities with active participation. This is where most rental property owners calculate their allowed losses. Report losses from rental activities on the appropriate lines, and the form determines how much flows through to your Form 1040. Understanding common IRS audit triggers can help ensure you're documenting your active participation correctly and avoiding red flags.

Complete Part III only if you have passive income to offset losses. This section allocates allowed losses among your various passive activities when you can't deduct everything. Part IV handles dispositions—when you sell or dispose of a passive activity, you can typically deduct all unallowed losses from that activity.

Unallowed losses don't disappear—they carry forward to future tax years indefinitely. The IRS tracks these losses on Form 8582, and you can deduct them when you generate passive income or when your modified adjusted gross income drops below the phase-out range.

You'll also use these carried-forward losses when you sell the rental property. In a taxable disposition, you can deduct all suspended passive losses from that specific activity against the gain from the sale. This often creates significant tax savings in the year of sale.

Keep detailed records of unallowed losses for each rental property separately. You'll need this information every year you file Form 8582. Most tax software tracks carryover losses automatically, but maintaining your own records provides backup documentation if questions arise.

The biggest mistake is not filing Form 8582 when required. Some taxpayers claim rental losses directly on Form 1040 without completing Form 8582 first. This creates a mismatch in IRS systems and can trigger correspondence or audits. Before claiming any rental loss deduction, verify whether Form 8582 applies to your situation.

Another frequent error involves calculating modified adjusted gross income incorrectly. This number determines your special allowance phase-out and must include specific additions to adjusted gross income listed in Form 8582 instructions. Missing these adjustments can cause you to claim more or less than your actual allowable deduction.

Many taxpayers also fail to properly document active participation. While the standard seems straightforward, the IRS may question your participation level during an audit. Maintain records of management decisions, tenant communications, and repair approvals. Our guide on preparing for a tax audit outlines the documentation standards the IRS expects.

Finally, taxpayers often incorrectly group activities or fail to track prior year unallowed losses by property. Each rental property is generally a separate activity for passive loss purposes. Mixing properties on Form 8582 can result in incorrect loss allocations and compliance issues.

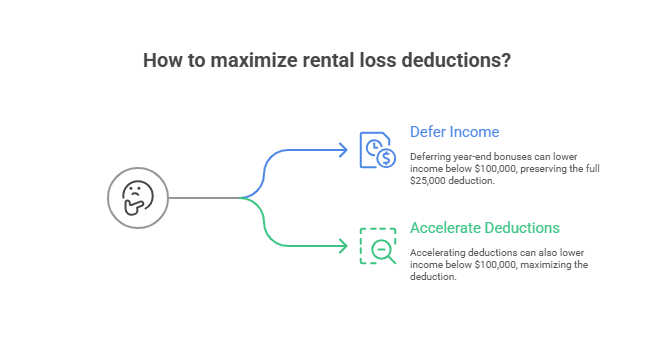

If your modified adjusted gross income hovers near the $100,000-$150,000 phase-out range, consider income-timing strategies. Deferring year-end bonuses or accelerating deductions can keep your income below $100,000, preserving your full $25,000 allowance. Even a $1 difference in modified adjusted gross income affects your deduction limit.

Real estate professionals can bypass passive activity loss limitations entirely by meeting the IRS criteria: spending more than 750 hours annually in real property trades or businesses, with that time representing more than half of all working hours. This classification allows you to deduct all rental losses against ordinary income without Form 8582 limits.

Generating passive income from other sources—such as limited partnership interests or passive business investments—gives you additional offset capacity for rental losses. Since passive losses can offset passive income dollar-for-dollar, diversifying your passive income streams can unlock otherwise suspended losses. Comprehensive tax planning strategies should evaluate your entire income portfolio, not just individual properties.

Consider a cost segregation study for larger rental properties. This tax strategy accelerates depreciation deductions by reclassifying building components with shorter recovery periods. While it doesn't change the passive loss rules, it increases your loss in early years when you might have more passive income or lower modified adjusted gross income.

Form 8582 becomes complex quickly when you own multiple rental properties, have passive income from various sources, or sold a rental property during the tax year. Professional tax preparers handle the intricate calculations and ensure you're maximizing available deductions while maintaining IRS compliance.

You should definitely consult a tax professional if your situation includes: modified adjusted gross income near phase-out thresholds, real estate professional status questions, or passive activity dispositions. These scenarios require nuanced interpretations of passive loss rules and accurate Form 8582 completion. Our tax planning and preparation services specialize in rental property taxation for real estate investors and CPA firms serving property owners.

The cost of errors on Form 8582 can be substantial. Claiming deductions without proper Form 8582 support creates audit risk, while miscalculating your allowable loss means you either pay more tax than necessary or face penalties for under-reporting. Professional preparation typically costs $200-500 but saves thousands in proper deduction optimization and audit protection.

No, you don't need to file Form 8582 if your rental activities generated only passive income without losses. The form only applies when you have losses from passive activities that need limitation calculations.

Yes, but only against passive income, not ordinary income. Without active participation, you lose access to the $25,000 special allowance. Your rental losses carry forward until you have passive income to offset them or until you dispose of the property.

Modified adjusted gross income starts with your adjusted gross income from Form 1040, then adds back certain deductions including IRA contributions, student loan interest, and passive loss deductions. Form 8582 instructions provide the complete calculation worksheet. This number determines whether you qualify for the special allowance phase-out.

When you dispose of a rental property in a fully taxable transaction, you can deduct all suspended passive losses from that specific activity. Report the disposition on Form 8582 Part IV, which releases prior year unallowed losses. These losses offset the gain from the sale or reduce your tax liability for the year.

Married individuals who file separate returns and lived with their spouse at any time during the tax year can only claim a maximum $12,500 special allowance, and it phases out starting at $50,000 modified adjusted gross income. If you lived apart the entire year, you each qualify for the full $25,000 allowance with the standard phase-out.

Filing an amended return with Form 8582 corrects the omission. The IRS may adjust your return if they discover the missing form during processing, typically disallowing rental loss deductions that required Form 8582 support. File Form 1040-X with the correct Form 8582 as soon as you discover the error.

It depends on rental duration and your participation level. If your average rental period is seven days or less and you provide substantial services, the rental might not be a passive activity. However, most short-term rentals without significant services still require Form 8582 for loss limitations unless you meet the real estate professional criteria.

We provide comprehensive tax preparation services for rental property owners and CPA firms serving real estate investors. Our team handles Form 8582 calculations, passive loss tracking, and tax planning strategies to maximize your deductions while ensuring IRS compliance. With 200+ U.S. accounting partnerships since 2015, we've processed thousands of rental property returns and understand the nuances of passive activity loss rules.

Form 8582 determines how much of your rental losses you can deduct each year based on passive activity loss limitations. Most rental property owners with losses exceeding the $25,000 special allowance or modified adjusted gross income above $100,000 must file this form. The calculation involves your income level, participation in rental activities, and prior year unallowed losses.

Getting Form 8582 right protects you from IRS scrutiny while maximizing legitimate deductions. Track your losses by property, maintain documentation of active participation, and consider professional tax preparation for complex rental portfolios. Proper planning around the passive loss rules can save thousands annually in tax liability and ensure compliance with IRS requirements.

Related read: irs tax.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.