An IRS 1031 exchange (named for Internal Revenue Code Section 1031) allows real estate investors to defer capital gains taxes when selling investment property by reinvesting proceeds into like-kind replacement property. You must identify replacement properties within 45 days and complete the purchase within 180 days, use a qualified intermediary to hold funds, and ensure both properties qualify as business or investment real estate.

Section 1031 of the Internal Revenue Code permits real estate investors to defer capital gains taxes when exchanging one investment property for another. The tax isn't eliminated, it's postponed until you eventually sell without exchanging again.

The law states "no gain or loss shall be recognized if property held for use in a trade or business or for investment is exchanged solely for property of like kind." This provision has existed since 1921, making it one of the tax code's oldest wealth-building tools still available to investors.

After the Tax Cuts and Jobs Act of 2017, 1031 exchanges apply only to real property, not personal property, equipment, or vehicles. The change took effect January 1, 2018, limiting exchanges to real estate held for investment or business use.

The tax benefit is substantial. A $500,000 gain on an investment property could trigger $100,000-$150,000 in combined federal and state capital gains taxes. A proper 1031 exchange defers that entire tax liability, leaving more capital working for you in the replacement property.

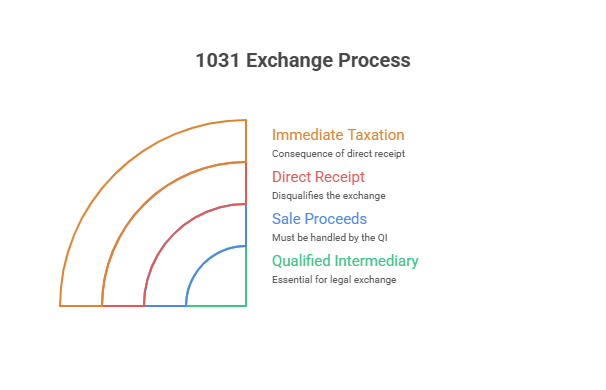

The IRS imposes strict, non-negotiable timelines on 1031 exchanges. Missing these deadlines by even one day disqualifies your exchange and triggers immediate taxation on your gain.

The 45-day identification period begins the day you close on selling your relinquished property. Within these 45 days, you must identify potential replacement properties in writing to your qualified intermediary. You can identify up to three properties regardless of value, or any number of properties as long as their combined fair market value doesn't exceed 200% of your relinquished property's value.

The 180-day exchange period also starts when you close on your sale. You must complete the purchase of your replacement property within 180 days or by your tax return due date (including extensions) for that year, whichever comes first. The 180 days includes the initial 45-day identification period.

For example, if you sell your rental property on March 1st, you must identify replacement properties by April 15th (45 days later) and close on the replacement purchase by August 28th (180 days from March 1st). The IRS grants no extensions except for federally declared disasters.

The "like-kind" requirement is broader than most investors realize. Properties are considered like-kind if they're of the same nature or character, even if they differ in quality or grade. Essentially, any U.S. real estate held for investment or business use is like-kind to other U.S. investment or business real estate.

You can exchange an apartment building for a shopping center, vacant land for a warehouse, or a single-family rental for a multi-unit apartment complex. The IRS doesn't require matching property types, just that both properties serve investment or business purposes.

Properties that don't qualify include real estate held primarily for sale (like fix-and-flip inventory), your primary residence (though exceptions exist), property outside the United States (U.S. property isn't like-kind to foreign property), and partnership interests or corporate stock.

Vacation homes can qualify under strict conditions outlined in Revenue Procedure 2008-16. The property must be rented at fair market rates for at least 14 days annually, and your personal use can't exceed 14 days or 10% of rental days, whichever is greater. These rules apply for two years before and after the exchange.

For investors managing multiple properties and considering exchanges, understanding comprehensive tax planning strategies helps you evaluate whether a 1031 exchange makes sense for your specific situation.

IRS regulations require using a qualified intermediary (QI) for virtually all 1031 exchanges. You cannot receive the proceeds from your sale directly, doing so disqualifies the exchange and triggers immediate taxation.

A qualified intermediary is an independent third party who facilitates the exchange by holding your sale proceeds in a segregated account, preparing required exchange documents, transferring funds directly to purchase your replacement property, and ensuring compliance with IRS requirements throughout the process.

You must engage your QI before closing on the sale of your relinquished property. Your purchase agreement should assign your contract rights to the QI, allowing them to handle the exchange funds without you taking constructive receipt.

Disqualified persons cannot serve as your QI. This includes your agent, accountant, attorney, broker, or anyone who's provided services to you within the past two years (with limited exceptions). The IRS also prohibits family members from acting as qualified intermediaries.

Choose an established QI carefully. They'll hold hundreds of thousands or millions of your dollars. Look for companies with fidelity bonds, errors and omissions insurance, and segregated client accounts. Many investors work with fractional CFO services to evaluate QI options and structure exchanges as part of broader portfolio strategy.

Understanding basis calculations prevents unexpected tax bills. Your adjusted basis in the replacement property equals your basis in the relinquished property, plus any additional cash you invest, minus any debt relief you receive.

"Boot" refers to any non-like-kind property you receive in the exchange, typically cash or debt relief. Boot is immediately taxable as capital gains. To avoid boot, your replacement property must be equal or greater in value than your relinquished property, and you must reinvest all proceeds from the sale.

Here's a practical example: You sell a rental property for $500,000 with a $100,000 mortgage. Your net proceeds are $400,000. To avoid boot, you must purchase replacement property worth at least $500,000 and either assume at least $100,000 in new debt or add $100,000 cash to the exchange. If you buy a $450,000 replacement with no debt, the $50,000 difference creates taxable boot.

Depreciation recapture also matters. When you eventually sell your replacement property without exchanging, you'll pay depreciation recapture taxes on all depreciation claimed on both the original and replacement properties. The 1031 exchange doesn't eliminate this liability, it defers it indefinitely as long as you keep exchanging.

Proper accounting throughout the exchange process is critical. Many real estate investors rely on specialized bookkeeping services to maintain accurate basis records, track depreciation schedules, and prepare documentation for Form 8824 filing requirements.

Every 1031 exchange must be reported to the IRS using Form 8824 (Like-Kind Exchanges), filed with your tax return for the year you transfer the relinquished property. The form details both properties, calculates any recognized gain (boot), and determines your basis in the replacement property.

Form 8824 requires specific information including description and dates of properties transferred and received, relationship between parties, value of like-kind and other property received, adjusted basis of properties relinquished, amount of liabilities assumed or relieved, and calculation of recognized gain and deferred gain.

Critical documentation to maintain includes the qualified intermediary agreement signed before closing, written identification of replacement properties within 45 days, closing statements for both sale and purchase, assignment agreements transferring contract rights to the QI, and contemporaneous records proving investment or business use of both properties.

The IRS can challenge exchanges lacking proper documentation. If you can't prove you met the timing requirements, properly identified replacement properties, or used a qualified intermediary, the entire exchange may be disqualified years later during an audit.

Even experienced investors make errors that disqualify their exchanges. The most costly mistakes include missing the 45-day identification deadline (no exceptions granted), touching the proceeds from the sale directly instead of using a QI, failing to reinvest all proceeds or reduce debt (creating taxable boot), and using property for personal use when it should be investment property.

Another frequent error involves related-party exchanges. If you exchange property with a related party (family member, controlled corporation, or partnership), special rules under Section 1031(f) apply. Both parties must hold the exchanged properties for at least two years, or the exchange is disqualified and gain is recognized.

Some investors incorrectly assume they can take cash out during the exchange for improvements or other purposes. Exchange funds can only be used to purchase replacement property, pay qualified exchange expenses, or pay off mortgages secured by the relinquished property. Using funds for other purposes, even temporarily, disqualifies the exchange.

Fix-and-flip properties don't qualify for 1031 treatment because they're held for sale, not investment. The IRS looks at your intent when acquiring the property. If you bought specifically to renovate and flip quickly, it's inventory, not an investment property eligible for exchange treatment.

For real estate professionals managing complex exchanges across multiple properties, understanding how to read financial statements properly helps you evaluate exchange opportunities and track deferred gains that will eventually become taxable.

Not immediately. The replacement property must be held for investment or business use, not personal residence. While you can eventually convert a 1031 property to your primary residence, you must first hold it as a rental for a substantial period (typically at least two years) to prove investment intent. Converting too quickly may disqualify the exchange upon IRS audit.

The exchange fails and your gain becomes taxable in the year you sold the relinquished property. The IRS grants no extensions to the 45-day deadline except for federally declared disasters. This is why many investors identify backup properties and work with experienced real estate professionals to locate suitable replacements quickly.

Yes. There's no limit on how many times you can use Section 1031. Investors can exchange properties repeatedly, deferring taxes indefinitely. The deferred gain accumulates across all exchanges. Many investors use this strategy to build substantial real estate portfolios while continually deferring taxes, potentially until death when heirs receive a stepped-up basis.

Yes, as long as both properties are in the United States. You can sell property in California and buy in Texas, or any other state combination. However, you cannot exchange U.S. property for foreign property, they're not considered like-kind under IRS rules. State tax implications vary, so consult tax professionals about state-specific requirements.

A reverse exchange occurs when you acquire replacement property before selling your relinquished property. This is more complex and expensive, requiring an Exchange Accommodation Titleholder to hold either the replacement or relinquished property. The same 45-day and 180-day rules apply but in reverse order. Reverse exchanges help investors who found ideal replacement properties before selling existing holdings.

Qualified intermediary fees typically range from $800-$1,500 for standard exchanges, with more complex transactions costing $2,000-$3,500. Additional costs include legal fees for reviewing documents, accounting fees for tax preparation and Form 8824 filing, and potentially higher closing costs. These expenses are small compared to the six-figure tax savings most exchanges provide.

Yes. You can sell one property and buy two, three, or more replacement properties as long as the combined value meets or exceeds your relinquished property's value and you reinvest all proceeds. This strategy allows investors to diversify geographically or by property type while maintaining 1031 tax deferral benefits.

You'll pay taxes on the difference (boot). If you sell for $500,000 and buy replacement property for $450,000, the $50,000 difference is taxable capital gain. The exchange is still valid for the portion invested, but you must pay taxes on uninvested proceeds. To maximize deferral, always buy equal or greater value and reinvest all proceeds.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.