Tax season gets all the attention when people talk about accounting outsourcing. But the month-end close is where the ongoing, year-round value lives. It is repetitive, detail-heavy, deadline-driven, and follows the same basic steps every single month. That makes it ideal for an offshore team.

The challenge is coordination. A month-end close involves multiple people touching the same data at different stages. Add an offshore team in a different timezone and you either have a well-choreographed workflow or a mess of email threads and missed handoffs.

We have refined this workflow across hundreds of CPA firm engagements at Madras Accountancy. The version below is our standard framework. Each firm customizes it based on their clients, but the structure stays consistent. Our outsourced accounting services guide covers the full range of services. This article goes deep on month-end specifically.

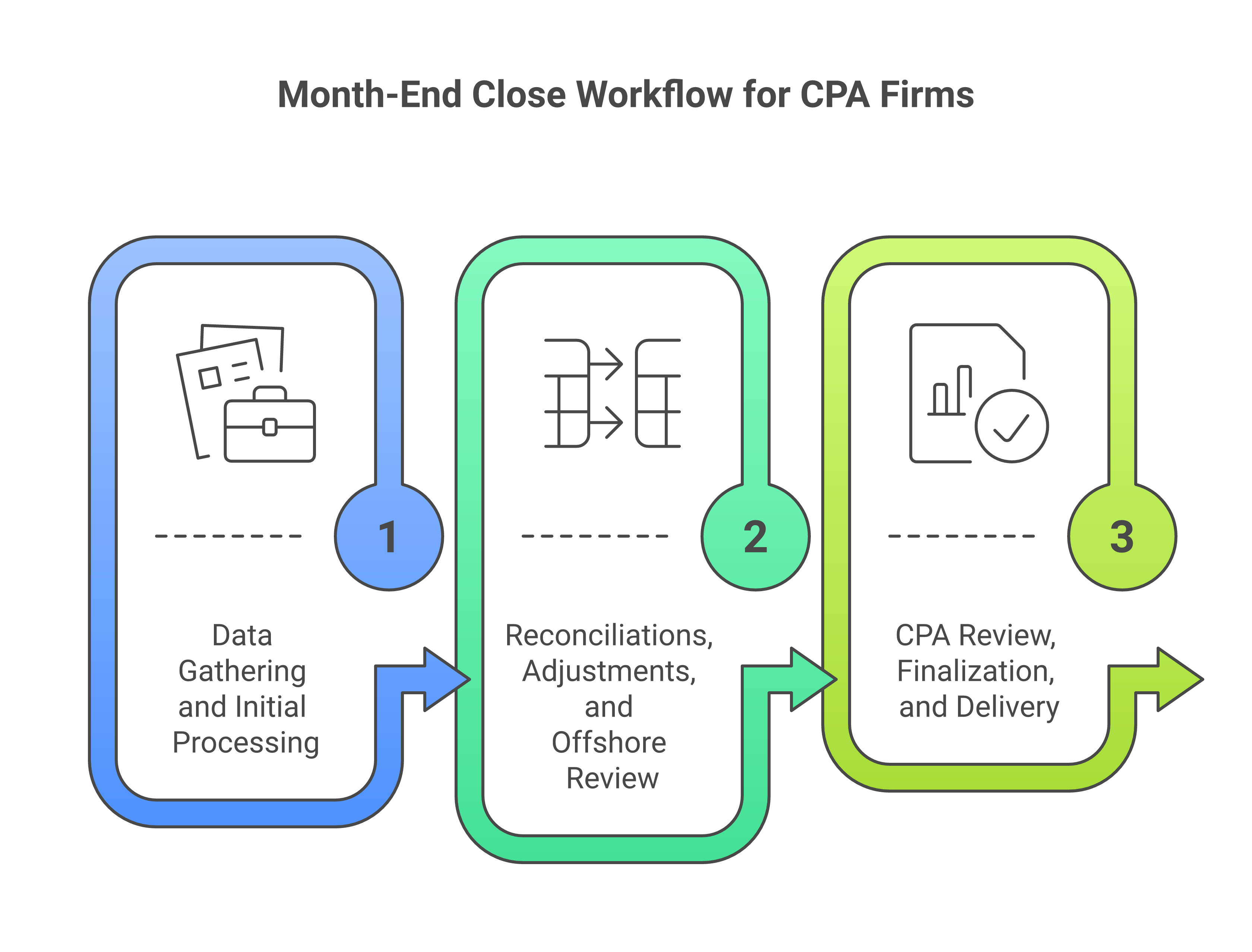

Most CPA firms target a 5 to 10 business day close cycle for their outsourced bookkeeping clients. Larger or more complex clients may take 10 to 15 business days. The workflow below assumes a standard close target of business day 10 after month-end.

The timeline splits into three phases. Days 1 through 3 are data gathering and initial processing. Days 4 through 7 are reconciliations, adjustments, and offshore review. Days 8 through 10 are CPA review, finalization, and delivery.

Day 1 (business day 1 after month-end) is about collecting everything the offshore team needs to work. The CPA firm or the client provides bank statements for all accounts (or confirms bank feed connections are current), credit card statements, payroll reports and pay registers, loan statements showing activity and balances, any manual transaction logs or cash receipts records, and accounts receivable and accounts payable reports from any separate systems.

Not all of this arrives on day 1. In fact, it rarely does. Bank statements are usually available immediately. Payroll reports often take a day or two. Loan statements trickle in. The key is that the offshore team does not wait for everything to start. They begin with what is available.

Our team starts working the evening of day 1 US time (morning day 2 India time). This is where the time zone advantage becomes tangible. While the US office is closed overnight, our team is processing bank transactions, categorizing expenses, posting payroll entries from the available reports, and flagging any missing documents.

Day 2 continues processing. The offshore team works through the transaction categorization for the full month. For clients on accrual basis, they also record revenue based on invoicing data and post cost of goods sold entries if applicable. Any transactions that cannot be categorized with confidence are flagged for the CPA team with a specific question ("Is this $4,200 payment to ABC Corp an office expense or a contractor payment?").

Day 3 finishes the initial processing. By end of day 3, all available transactions should be entered and categorized. The trial balance should be taking shape, even if some items are still pending (waiting for a statement, waiting for clarification on a transaction).

At the end of day 3, the offshore team sends a status update to the CPA firm. This update includes what has been completed, what is still pending and why, any questions that need CPA or client input, and an estimated completion date.

This day 3 status update is not optional. It is a checkpoint that keeps both teams aligned and surfaces problems early. If a bank statement is missing and the client has not responded, the CPA firm can follow up on day 4 instead of discovering the gap on day 8.

This is the core of the close process and where the offshore team does the most detailed work.

Day 4: Bank reconciliations. Every bank account is reconciled to the statement. Outstanding checks and deposits in transit are identified and documented. Any discrepancies are investigated and resolved or flagged. Bank reconciliation is the single most important control in the close process. If the bank rec does not tie, nothing else matters until it does.

Our team uses a standard reconciliation format that includes the GL balance, the bank statement balance, outstanding items, and the reconciling difference (which should be zero). Each outstanding item is aged. Items outstanding for more than 60 days get flagged for investigation. Our month-end close checklist for controllers covers the 20 most common errors in this process.

Day 5: Credit card and loan reconciliations, plus intercompany entries. Credit card accounts are reconciled to statements. Loan balances are verified and interest expense is posted. For clients with multiple entities, intercompany transactions are posted and balanced. Intercompany work is often the most time-consuming part of multi-entity closes, so starting it on day 5 gives adequate time for resolution.

Day 6: Adjusting entries. With reconciliations complete, the offshore team posts standard adjusting entries. Depreciation per the fixed asset schedule. Amortization of prepaids and other deferred items. Accrued expenses (rent, insurance, professional fees) based on the client's accrual schedule. Accrued payroll if pay period does not align with month-end. Deferred revenue adjustments if applicable.

Each adjusting entry references the supporting schedule or calculation. No adjusting entry is posted without documentation. This is a firm rule at Madras. An adjusting entry with no support is an error waiting to happen.

Day 7: Offshore peer review. A second member of the offshore team reviews the entire close package. They are checking that all reconciliations tie, all standard adjusting entries are posted, the trial balance is reasonable (no unusual balances, no sign errors, no suspense account balances), the financial statements are generating correctly from the trial balance, and the preparation checklist is complete.

The peer reviewer has fresh eyes. They have not been in the weeds of this client's transactions for the past week. Their job is to catch the things the preparer missed because of familiarity or fatigue.

By end of day 7, the close package is ready for CPA review. It includes the trial balance, financial statements (income statement, balance sheet, cash flow if required), all bank and credit card reconciliations, supporting schedules for adjusting entries, the completed preparation checklist, and a review notes memo highlighting any items that need CPA judgment.

Day 8: CPA review begins. The onshore CPA or senior accountant reviews the close package. Their focus is on whether the financial story makes sense. Revenue is up 15 percent from last month, is that real or an error? Operating expenses dropped 20 percent, what drove that? Cash is lower than expected, where did it go?

The CPA reviewer is not re-doing the reconciliations. That work was done in layers 1 and 2 (preparation and peer review). The CPA is applying professional judgment and client knowledge.

Review notes go back to the offshore team with specific instructions. "Reclassify the $3,200 from office supplies to equipment (it was a laptop purchase)." "Confirm with the client whether the $10,000 deposit on 3/28 is a customer prepayment or a loan draw." "Add a footnote explaining the insurance expense spike (annual premium paid in one month)."

Day 9: Revisions and resolution. The offshore team processes review notes and resolves open items. Most revisions are completed within a few hours. Items requiring client input may take longer and are tracked separately.

Day 10: Final review and delivery. The CPA does a final review of the revised package, approves it, and delivers the financial statements to the client. Delivery format varies by client, from a simple email with PDF statements to a presentation in the client's accounting portal.

The handoff between offshore and onshore teams is the point where most coordination problems occur. We use a structured handoff protocol that eliminates ambiguity.

Offshore to onshore handoff (day 7 to day 8) includes a handoff email with a standardized subject line (Client Name, Month-Year Close, Ready for Review). The email contains a link to the close package in the shared document system, a summary of any open items or questions, the completed preparation checklist, and a flag for any items that are time-sensitive.

Onshore to offshore handoff (review notes, day 8 to day 9) uses the same structure. Standardized format, specific instructions, severity level for each item. We avoid vague review notes like "check the revenue" in favor of specific ones like "Revenue of $142,000 is $18,000 higher than the prior month. Confirm whether invoice #4892 ($18,500) should be recognized in March or April based on the delivery date."

The handoff happens at a consistent time each day. Our standard handoff time is 6 PM US Eastern, which is 3:30 AM India Standard Time. Our team picks up the work at 9 AM IST (approximately 11:30 PM Eastern). By the time the US office opens the next morning, the overnight work is done. This creates a continuous workflow where each team picks up where the other left off.

No month-end close runs perfectly every time. Here is how we handle the common complications.

Missing documents. When a bank statement or other document is not available by day 3, the offshore team proceeds with all other work and sends a specific request to the CPA firm listing exactly what is missing. The CPA firm follows up with the client. If the document is still not available by day 6, we prepare the close with the available data and note the incomplete items. The close is delivered with a qualification, and the missing items are resolved when the documents arrive.

Client-dependent questions. Some transactions require client input to categorize correctly. We batch these questions and send them to the CPA firm on day 2 or 3 (not in a trickle of individual emails). The CPA firm relays them to the client. If answers are not back by day 6, we use the most reasonable categorization, flag it, and adjust when the answer comes.

Prior period adjustments. Sometimes the review uncovers an issue from a previous month. If it is material, we post a prior period adjustment and note it in the current month's close memo. If it is immaterial, we adjust it in the current month. The CPA makes the materiality judgment.

Volume spikes. Some clients have months with significantly higher transaction volumes (retail clients in December, construction companies in summer). We plan for these based on historical patterns and temporarily assign additional preparers during high-volume months.

The 10-day workflow above is the standard framework, but it flexes based on client complexity.

Simple clients (single entity, cash basis, fewer than 100 transactions per month) can close in 5 to 7 business days. The offshore team often completes preparation and peer review in 3 to 4 days, leaving the CPA only 1 to 2 days for review.

Complex clients (multi-entity, accrual basis, intercompany transactions, 500 or more transactions per month) may need 12 to 15 business days. The extra time is primarily in the reconciliation and intercompany elimination phases. These clients also typically need a more detailed CPA review.

Clients with external reporting deadlines (lender covenants, board reporting, investor updates) have fixed delivery dates that drive the timeline backward. If the board meeting is on the 15th and they need financials two days before, the close must be done by the 13th. We work backward from these deadlines to set the offshore team's start date and milestones.

We track three metrics for every month-end close engagement.

Close cycle time measures the number of business days from month-end to delivery of final financial statements. We track this monthly and trend it over time. The goal is consistency more than speed. A client that closes in 8 days every month is better off than one that closes in 5 days some months and 15 days in others.

Revision rate measures how many review notes the CPA sends back per close. A declining revision rate over time indicates the offshore team is learning the client and the CPA is spending less time on corrections. Our outsourcing ROI analysis shows how reduced review time translates to cost savings.

Open items at delivery tracks how many items are still unresolved when the financial statements are delivered. Ideally this is zero. A small number of immaterial open items is acceptable if they are clearly documented and tracked for resolution.

If your firm currently handles month-end closes entirely in-house and wants to transition to an offshore model, the process takes 2 to 3 months per client.

Month 1 is the shadow month. The offshore team prepares the close in parallel with the in-house team. Both produce the same deliverables. The CPA compares the two and identifies gaps in the offshore team's work. This reveals what additional training or documentation is needed.

Month 2 is the transition month. The offshore team takes the lead, but the in-house team is still available as a backstop. The CPA reviews the offshore team's work more thoroughly than they will in steady state.

Month 3 is steady state. The offshore team owns the preparation and the CPA reviews at the standard level. The in-house staff previously handling this client's close is now available for higher-value work.

Our first 90 days guide for offshore accounting teams covers this transition in more detail across all service types.

If your firm handles month-end closes for multiple clients and your onshore team is spending too much time on preparation work instead of review and advisory, offshoring the close process can reclaim that time.

At madrasaccountancy.com, we can walk you through how this workflow would look for your specific client base. We will assess your client mix, identify which clients are good candidates for offshore close work, and set up the handoff protocol and timeline that matches your firm's process.

It depends on complexity. A single offshore accountant can typically handle 8 to 12 simple bookkeeping clients or 4 to 6 complex multi-entity clients per month. We staff based on total hours required, not just client count, because a single complex client can take as much time as five simple ones.

We work in QuickBooks Online, QuickBooks Desktop, Xero, Sage, NetSuite, and several other platforms. Our team accesses the firm's software through secure remote connections. There is no data migration or software change required on the firm's side.

It is rare but it happens. When it does, we correct the error immediately, document it in our error tracking system, conduct a root cause analysis to understand why it passed through all review layers, and update our process to prevent recurrence. The CPA firm is always informed and we take responsibility for the correction work at no additional charge.

Yes. Our team is trained on US GAAP, and GAAP compliance is built into our preparation checklists and review process. For clients with specific GAAP requirements (revenue recognition under ASC 606, lease accounting under ASC 842, etc.), we include additional checklist items and review steps specific to those standards. Our GAAP handover playbook covers how we handle GAAP-specific requirements for offshore work.

Each client engagement is set up individually with the client's existing chart of accounts. Our team does not impose a standard chart of accounts. We work within whatever structure the CPA firm and client use. Industry-specific categorization (construction cost codes, medical practice revenue categories, nonprofit fund accounting) is part of the onboarding and training for each client.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.