A Nevada real estate accounting company provides specialized financial services including bookkeeping, tax preparation, entity structuring, and strategic advisory tailored for property investors, developers, property managers, and real estate professionals operating in Nevada.

These firms understand Nevada's unique advantages, no state income tax, favorable LLC laws, and transaction volume dynamics in markets like Las Vegas and Reno, and structure accounting systems that maximize these benefits. This expertise matters because real estate transactions involve complex depreciation schedules, 1031 exchanges, multi-entity structures, and cash flow management that generic accountants handle poorly.

Nevada's tax-free status attracts real estate investors nationwide, but this doesn't eliminate tax complexity. Federal taxes still apply, local option taxes exist in certain jurisdictions, and Nevada's Modified Business Tax on payroll affects property management companies and development firms. Whether you're flipping houses in Henderson, managing vacation rentals near Lake Tahoe, or developing commercial projects on the Las Vegas Strip, specialized accounting determines whether your investments generate sustainable profits or create unexpected liabilities. Here's what you need to know about working with a Nevada real estate accounting company.

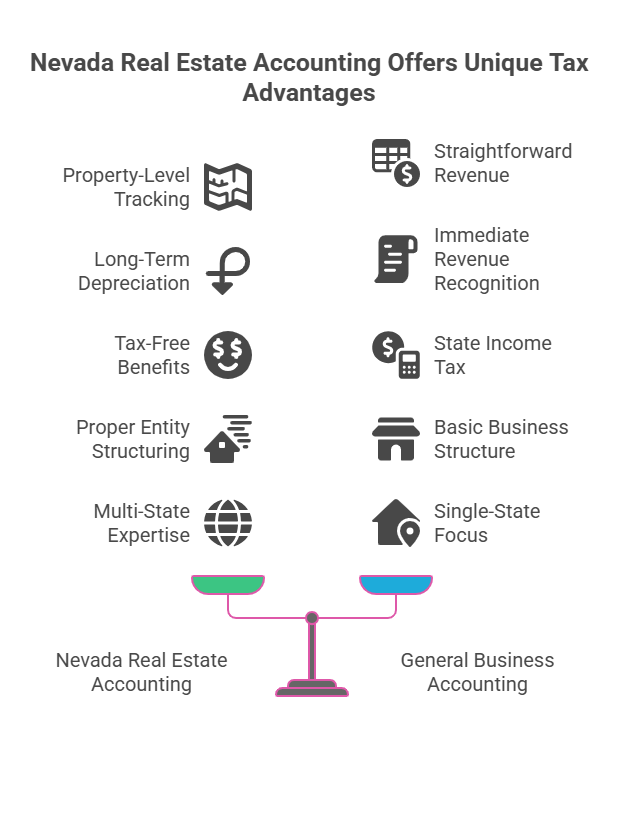

Real estate accounting requires property-level financial tracking, long-term depreciation management spanning 27.5 to 39 years, coordination of 1031 exchanges with strict IRS deadlines, and handling complex partnership structures for syndicated deals. Unlike service businesses with straightforward revenue recognition, real estate involves capital versus repair decisions, cost segregation studies, and passive activity loss rules that significantly impact tax outcomes.

Nevada's lack of state income tax creates unique planning opportunities. Real estate investors don't pay state tax on rental income or capital gains, allowing them to keep more profit compared to California (13.3% top rate) or Oregon (9.9%).

However, this advantage disappears if you don't structure entities properly or fail to document Nevada residency correctly. Accounting firms specializing in Nevada real estate ensure clients maximize tax-free benefits while maintaining defensible positions during IRS audits.

The Modified Business Tax (MBT) applies to Nevada businesses with employees, charging 1.475% on wages exceeding $50,000 per quarter for most industries. Property management companies with leasing agents, maintenance staff, or administrative employees must track quarterly payroll thresholds and file MBT returns. Real estate developers with construction crews face similar requirements. Specialized accountants monitor these thresholds, calculate quarterly payments, and integrate MBT into overall tax planning.

Nevada's popularity for out-of-state investors creates additional complexity. California residents buying Nevada rental properties must track income and expenses separately for California tax purposes, Nevada's tax-free status doesn't eliminate California obligations. Accountants experienced in multi-state real estate help investors maintain proper documentation, file non-resident returns correctly, and avoid costly mistakes that trigger state audits.

Specialized accounting firms set up systems tracking each property's income, expenses, cash flow, and performance metrics separately while consolidating data for portfolio-level analysis. This property-level detail reveals which investments generate returns and which drain resources, information impossible to extract from combined bookkeeping.

Most successful Nevada real estate investors use QuickBooks Online Plus with class tracking or dedicated property management software like AppFolio or Buildium. These systems create separate profit-and-loss statements for each property, showing rental income, operating expenses, mortgage payments, and net cash flow. When you own properties across Las Vegas, Reno, and Mesquite, property-level tracking identifies geographic performance differences and informs acquisition decisions.

For investors managing 5+ properties or complex structures involving multiple LLCs, professional outsourced bookkeeping services handle monthly transaction recording, bank reconciliation, and financial reporting. This frees investors from data entry while ensuring accurate records for tax preparation and performance analysis. The time saved, typically 15-20 hours monthly, redirects toward finding deals and managing tenants.

Depreciation tracking becomes critical as portfolios grow. Each property has its own placed-in-service date, depreciable basis, and accumulated depreciation. When you sell a property, recapture calculations depend on accurate depreciation records spanning ownership. Accountants maintain detailed depreciation schedules, coordinate cost segregation studies when beneficial, and ensure proper reporting on tax returns and during property sales.

Specialized firms focus on maximizing federal deductions, timing income recognition strategically, structuring entities for liability protection and tax efficiency, coordinating 1031 exchanges to defer capital gains, and documenting real estate professional status for investors seeking to offset W-2 income with rental losses.

Nevada investors avoid state income tax but still pay federal tax rates up to 37% on ordinary income and 20% on long-term capital gains. Cost segregation studies accelerate depreciation by identifying property components depreciable over 5, 7, or 15 years instead of 27.5 or 39 years. A $3 million apartment complex might generate $200,000+ in first-year depreciation through cost segregation versus $80,000 using straight-line depreciation, creating $30,000-$40,000 in immediate tax savings for high-income investors.

Understanding Section 179 and bonus depreciation opportunities helps investors time equipment purchases and property improvements for maximum tax benefit. While Section 179 doesn't apply to rental property buildings, it covers equipment like appliances, furniture in furnished rentals, and vehicles used for property management. Bonus depreciation allows 60% immediate write-off for qualified improvement property in 2025, creating significant tax savings when renovating properties.

Real estate professional status qualification allows active investors to deduct rental losses against W-2 income or business income, bypassing passive activity loss limitations. This requires 750+ annual hours in real estate activities and more time in real estate than any other business activity. Nevada accountants help investors document qualifying activities, structure record-keeping systems proving material participation, and defend positions during IRS examination. For high-income earners with substantial rental losses, this status saves $20,000-$60,000 annually in tax.

Section 1031 exchanges allow real estate investors to defer federal capital gains tax by reinvesting sale proceeds into like-kind property. Nevada accountants coordinate the 45-day identification deadline, 180-day closing requirement, qualified intermediary selection, and proper documentation ensuring exchanges meet IRS requirements while deferring federal tax liability.

Nevada's zero state income tax means investors avoid state capital gains tax on property sales, a major advantage over California, where state tax adds 13.3% to federal liability. However, federal capital gains tax still applies unless you execute a proper 1031 exchange. Selling a property with $500,000 in appreciation creates $100,000 in federal tax (20% rate plus 3.8% net investment income tax). A successful exchange defers this tax indefinitely, allowing reinvestment of full proceeds.

The identification period requires strict compliance. Investors have exactly 45 calendar days from sale closing to identify replacement properties in writing to their qualified intermediary. Accountants help clients identify backup properties, understand the three-property rule (any three properties regardless of value), and evaluate whether identified properties meet exchange requirements. Missing this deadline, even by one day, disqualifies the exchange and triggers immediate tax liability.

Partial exchanges create taxable "boot" requiring careful planning. If you sell a $2 million property and reinvest only $1.8 million, the $200,000 difference is taxable income.

However, accountants structure transactions to minimize boot, for example, using mortgage financing on the replacement property to achieve equal or greater debt, or identifying multiple smaller properties totaling sufficient value. These strategies require coordination between your accountant, qualified intermediary, and lender before initiating the exchange.

Property management companies face unique accounting challenges including trust account management, owner distribution calculations, 1099 reporting for owners and contractors, Modified Business Tax compliance for employee wages, and financial reporting satisfying both property owners and lending institutions. Nevada law imposes strict trust accounting requirements creating serious liability if violated.

Trust accounting represents the highest compliance risk. Nevada requires property managers to deposit owner funds, rent, security deposits, late fees, into separate trust accounts and maintain detailed records reconciling owner balances. Commingling trust funds with company operating accounts violates Nevada Real Estate Division regulations and creates civil and criminal liability. Accountants set up proper trust accounting systems, perform monthly three-way reconciliations, and ensure compliance with Division audit requirements.

Property managers must issue 1099-NEC forms to property owners receiving $600+ in annual net proceeds and contractors paid $600+ for repairs or services. This seems straightforward but becomes complex when management fees and expenses reduce owner proceeds below reporting thresholds. Nevada accountants track these amounts throughout the year, prepare accurate 1099s by January 31, and handle backup withholding when contractors fail to provide W-9 forms.

The Modified Business Tax applies to property management companies with employees. Wages exceeding $50,000 per quarter trigger the 1.475% tax. For companies with 5-10 employees handling leasing, maintenance coordination, and administration, quarterly MBT obligations range from $2,000-$6,000 annually. Accountants monitor payroll totals, calculate quarterly payments, and file required reports with the Nevada Department of Taxation. For firms managing payroll complexities across multiple locations, reviewing comparative payroll service options ensures compliance while minimizing administrative burden.

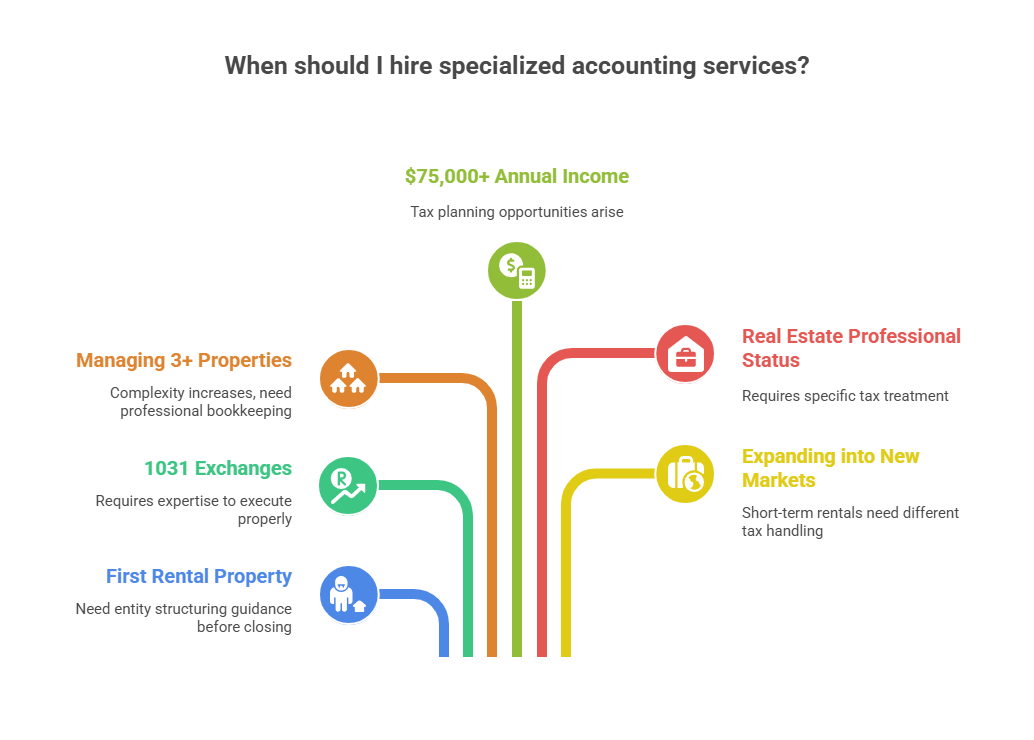

Investors should engage specialized accountants when purchasing their first rental property, before executing 1031 exchanges, when managing 3+ properties, if generating $75,000+ in annual rental income, when considering real estate professional status, or when expanding into new markets like short-term vacation rentals requiring different tax treatment.

First-time investors need entity structuring guidance before closing. Holding property in your personal name versus an LLC creates different liability protection and tax consequences.

Nevada charges only $425 initial filing fees and $350 annual fees for LLCs, significantly lower than California's $800 minimum franchise tax. However, creating separate LLCs for each property multiplies costs quickly. Accountants analyze your portfolio plans, insurance coverage, and tax situation to recommend optimal structures rather than generic online advice.

Investors crossing 3-4 properties reach complexity where DIY bookkeeping becomes counterproductive. You're spending 12-18 hours monthly on transaction recording instead of managing properties or finding deals. Professional accounting provides property-level reporting, handles multi-entity tax returns, and delivers monthly financial statements showing portfolio performance, information driving better investment decisions.

Real estate investors generating substantial income, $75,000+ annually, face tax planning opportunities that dwarf accounting fees. Strategies like cost segregation, entity restructuring for asset protection, or maximizing deductions typically save $8,000-$25,000 annually in federal tax. Without specialized guidance, investors leave money on the table through missed deductions, improper entity structures, or failing to document deductible expenses properly.

When facing IRS audit or examination, experienced accountants become essential. Real estate audits often focus on depreciation claims, passive activity loss treatment, or improper deduction classifications. CPAs represent clients during audits, organize documentation, and negotiate with examiners, preventing costly mistakes and unnecessary assessments. Understanding common audit triggers helps investors maintain defensible positions and avoid issues that draw IRS attention.

Madras Accountancy provides comprehensive real estate accounting services for Nevada investors, developers, property managers, and real estate professionals. We handle monthly bookkeeping at the property level, multi-entity tax preparation, 1031 exchange coordination, strategic tax planning, and financial reporting for clients across Las Vegas, Reno, Henderson, and statewide.

Our team understands Nevada's tax advantages and compliance requirements. We help investors maximize federal tax benefits while maintaining Nevada residency documentation protecting tax-free status. For clients with properties in multiple states, we coordinate multi-state tax filings, track nexus issues, and ensure compliance across jurisdictions.

We specialize in serving real estate investors with 2-25 properties who need more than basic bookkeeping but don't justify full-time accounting staff. Our services include monthly financial reporting showing property-level performance, consolidated portfolio views, cash flow analysis, and key metrics driving investment decisions. We coordinate cost segregation studies when beneficial, structure 1031 exchanges with proper documentation, and provide tax planning guidance that reduces federal liability by thousands annually.

For property management companies, we deliver trust accounting systems complying with Nevada Real Estate Division requirements, proper 1099 reporting for owners and contractors, Modified Business Tax calculation and filing, and financial reporting satisfying property owners and lenders.

Our offshore partnership model provides CPA-supervised work at costs significantly below traditional Nevada firms, delivering premium service without premium pricing.

Costs vary by portfolio complexity. Single-property investors typically pay $1,000-$1,800 annually for tax preparation. Investors with 3-5 properties spending $2,500-$4,500 for monthly bookkeeping and tax services. Larger portfolios (8+ properties) or property management companies invest $6,000-$18,000 annually for comprehensive accounting including property-level reporting, tax planning, and advisory services. Most firms offer monthly retainer arrangements spreading costs throughout the year.

No, federal taxes still apply and represent the largest tax burden for real estate investors. Federal income tax rates reach 37%, capital gains tax hits 20% plus 3.8% net investment income tax, and depreciation recapture adds 25% tax on accumulated depreciation. Strategic planning, cost segregation, 1031 exchanges, real estate professional status, saves $10,000-$50,000 annually for active investors with substantial portfolios, making Nevada accounting expertise valuable despite state tax-free status.

Yes, but they should understand Nevada-specific requirements like Modified Business Tax, trust accounting rules for property managers, and Nevada residency documentation protecting tax-free benefits. Many California CPAs lack Nevada expertise, potentially missing opportunities or creating compliance issues. If you're a California resident with Nevada properties, you need multi-state expertise handling both California non-resident returns and Nevada regulations properly.

Accountants track transient lodging tax obligations for vacation rentals, which vary by jurisdiction, Clark County charges 13.38%, Washoe County 13%, and other areas have different rates. They categorize income properly (Schedule C for active rentals versus Schedule E for passive), track occupancy taxes, handle 1099-K reporting from platforms like Airbnb and Vrbo, and maintain records supporting deductions for direct expenses like cleaning, supplies, and utilities that differ from long-term rental treatment.

Most investors use single-member LLCs for each property or group of properties, providing liability protection without complex tax filing. Nevada's low LLC fees ($350 annually) make per-property LLCs affordable. Larger investors might use series LLCs (available in Nevada) creating separate liability protection for multiple properties under one umbrella. For syndications or partnerships, multi-member LLCs taxed as partnerships provide flexibility with proper operating agreements. Your accountant should analyze your specific situation, property count, financing plans, liability concerns, before recommending structures.

Establish Nevada domicile through multiple factors: physical presence in Nevada 183+ days annually, Nevada driver's license, vehicle registration, voter registration, homestead declaration on Nevada property, closing out-of-state voter registration and licenses, and using Nevada address for all official documents. Accountants help document these factors and maintain evidence supporting Nevada residency during potential state audits from your previous state, particularly California, which aggressively pursues former residents.

Maintain detailed trust account records showing all deposits and disbursements, monthly three-way reconciliations (bank balance, general ledger, owner balances), owner ledgers tracking income and expenses by property, security deposit tracking separately from rent, contractor payment records with W-9s on file, employee payroll records for MBT reporting, and all documentation for six years. Nevada Real Estate Division can audit at any time, making proper record-keeping essential for maintaining your license.

Only if you qualify as a real estate professional under IRS rules, requiring 750+ hours annually in real estate activities and more time in real estate than any other work. If you don't qualify, rental losses are passive and only offset passive income. However, investors with adjusted gross income below $100,000 can deduct up to $25,000 in passive rental losses against W-2 income, phasing out completely at $150,000. Nevada accountants help determine qualification status and document activities supporting real estate professional claims.

Madras Accountancy specializes in accounting services for Nevada real estate investors, property managers, developers, and real estate professionals. Our team delivers property-level bookkeeping, multi-entity tax preparation, 1031 exchange coordination, and strategic tax planning that maximizes federal deductions while ensuring compliance with Nevada requirements. We combine real estate expertise with efficient offshore delivery, providing premium service at competitive rates for clients across Las Vegas, Reno, and statewide. Schedule a free consultation to discuss how we support your Nevada real estate investment goals and streamline your accounting operations.

Related read: federal tax.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.