Most businesses sell a product or a service, collect payment, and record revenue. Construction does not work that way. A general contractor signs a $4.2 million contract in January, spends 14 months building the project, bills monthly based on progress estimates, holds retainage that will not be collected for 60 to 90 days after substantial completion, and recognizes revenue using a method that most bookkeepers have never encountered.

Try handing that to a bookkeeper who usually handles dental practices and e-commerce stores. It will not go well.

CPA firms serving construction clients know this. The accounting requirements are specialized, the financial statements have unique line items, and the tax implications of revenue recognition method choices can run into six or seven figures. The problem is finding bookkeeping support that actually understands construction. Not bookkeepers who will learn on the job at your client's expense.

We built our construction accounting capability because CPA firms told us, repeatedly, that they could not find outsourced teams competent enough to handle their contractor clients. Here is what the work actually involves and how we approach it.

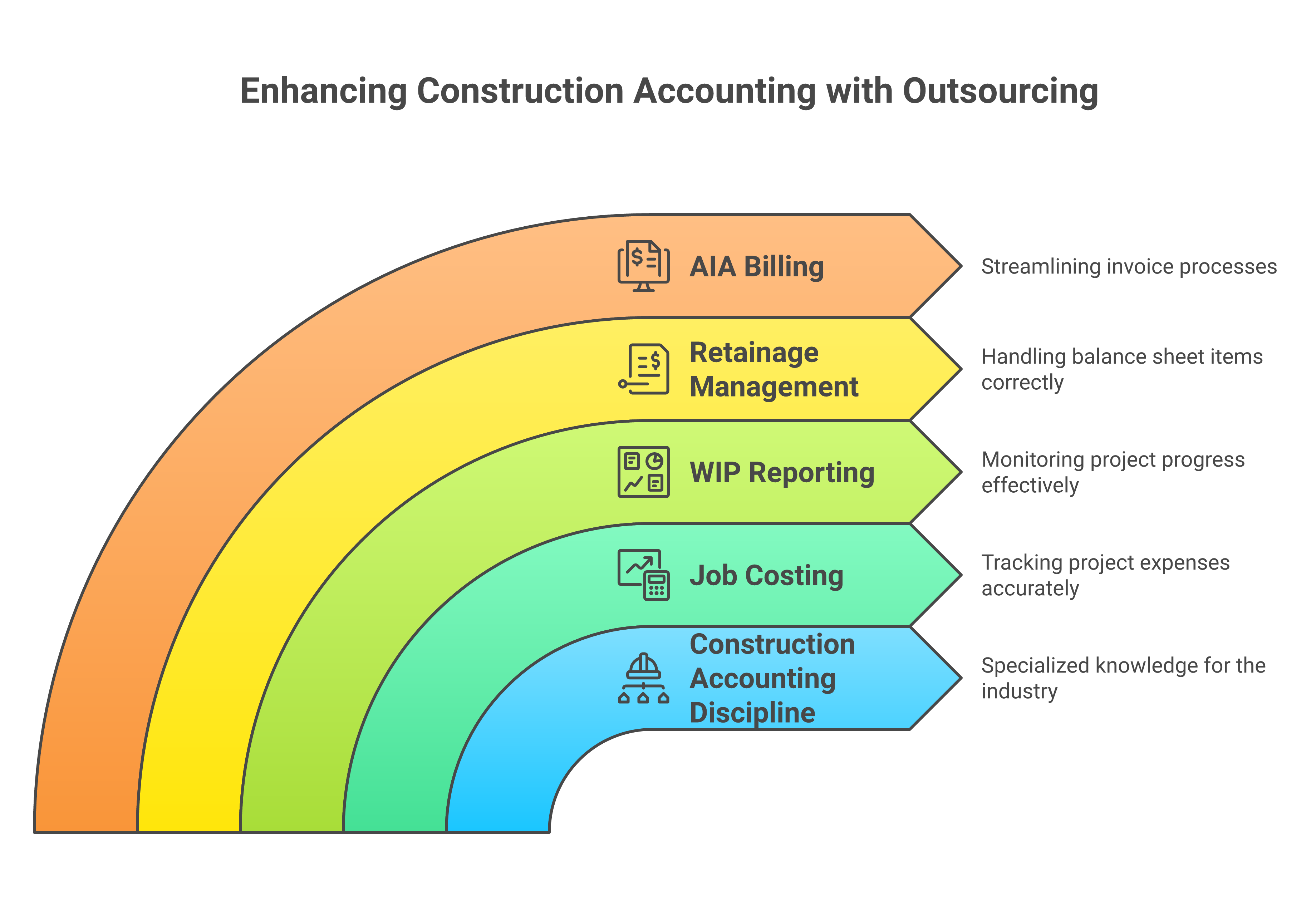

In construction accounting, the job is the unit of analysis. Not the department, not the product line, not the location. The job. Every dollar of cost and every dollar of revenue must be tracked to a specific project. If your bookkeeping team cannot do this accurately and consistently, every financial statement, every WIP report, and every tax return built on that data is unreliable.

Job costing in construction means tracking costs across several categories for each project:

Direct labor. The wages, burden (payroll taxes, workers' comp, benefits), and overtime for crew members working on a specific job. This requires either job-specific timekeeping or allocation based on time records. Certified payroll for prevailing wage jobs adds another layer of complexity.

Materials. Lumber, concrete, steel, fixtures, finishes. Every purchase order and material receipt needs to be coded to a job. When materials are purchased in bulk and used across multiple jobs, the bookkeeper needs to allocate costs based on actual usage, not just split them evenly.

Subcontractor costs. On most commercial projects, subcontractors represent 40 to 70 percent of total job cost. Each sub's contract, change orders, invoices, and retainage must be tracked at the job level. A bookkeeper who records a subcontractor invoice to a general "subcontractor expense" account without job coding has defeated the entire purpose.

Equipment costs. Owned equipment used on a job needs internal rental rates applied. Rented equipment is coded directly. Either way, it goes to the job.

Overhead allocation. Job-related overhead (supervision, job site office costs, small tools) versus general company overhead. The allocation method needs to be consistent and defensible.

Getting job costing right is not optional for construction clients. Contractors use job cost reports to make real-time decisions: whether to bid more aggressively, whether a project is losing money, whether a subcontractor's costs are running over budget. If the books are three weeks behind or the cost coding is sloppy, those decisions get made on bad information.

The Work in Progress (WIP) schedule is the most important financial report in construction accounting. It is also the report most commonly done wrong by bookkeeping teams that do not specialize in construction.

A WIP schedule shows, for every active job:

The over/under billing calculation is what makes this unique. If a contractor has billed more than the revenue earned to date, they are overbilled, meaning they have collected cash ahead of the work performed. If they have billed less than earned, they are underbilled. The net overbilling or underbilling position flows directly to the balance sheet.

Why do outsourced teams struggle with this? Several reasons.

They do not understand estimated cost at completion. This is not a number the bookkeeper calculates from the books. It requires input from the project manager or estimator. The bookkeeper's job is to capture the current estimate, compare it to costs incurred, and flag significant changes from the prior period. But first, they need to know to ask for it.

They confuse billings with revenue. In construction, cash collected and invoices sent are not revenue. Revenue is recognized based on the percentage of completion method (for most contractors using GAAP or for tax purposes under IRC Section 460 for long-term contracts). A bookkeeper who records billings as revenue will produce financial statements that are materially wrong.

They do not reconcile the WIP to the general ledger. The WIP schedule is a supporting schedule. The underbilling and overbilling amounts on the WIP must tie to the balance sheet. If they do not, something is wrong in either the WIP inputs or the general ledger. This reconciliation step gets skipped constantly by teams unfamiliar with construction.

At Madras, our construction team prepares WIP schedules monthly for every active job. We work with the CPA firm and the contractor's project managers to get updated cost estimates. We reconcile the WIP to the GL. We produce the schedule in the format the CPA firm needs for financial statement preparation and tax planning.

Retainage is a standard feature of construction contracts. The project owner withholds a percentage (usually 5 to 10 percent) of each progress payment until the project reaches substantial completion or passes final inspection. The contractor, in turn, typically withholds retainage from their subcontractors on the same terms.

This creates two balance sheet items that construction bookkeepers must track:

Retainage receivable. The amount the contractor has billed but the owner is holding. This is a real asset. It will be collected, usually within 60 to 90 days of project completion. But it cannot be lumped in with regular accounts receivable. It has different aging characteristics and different collection triggers.

Retainage payable. The amount the contractor is holding from subcontractors. This is a real liability that will be paid upon project completion and subcontractor sign-off.

The bookkeeping errors we see most often with retainage:

If your outsourced bookkeeping team treats retainage as an afterthought, your construction client's balance sheet is wrong. And a wrong balance sheet means the contractor's bonding company, bank, and surety are making decisions based on inaccurate information. For a contractor, bonding capacity is directly tied to financial statement quality. Bad books can literally cost them their ability to bid on projects.

Most commercial construction contracts use AIA (American Institute of Architects) billing documents. The two most common are:

These are not normal invoices. They are structured documents with specific fields, calculations, and sign-off requirements. The project owner's representative (usually an architect or construction manager) reviews and approves each application before the owner processes payment.

Preparing AIA billing requires the bookkeeper to:

Many CPA firms handle AIA billing prep as part of their advisory work, but increasingly we see this delegated to the bookkeeping team. Our construction accounting team at Madras can prepare AIA billing documents, though the percentage completion estimates always come from the contractor's field team. We process the numbers. We do not estimate how much concrete has been poured.

The percentage of completion (POC) method is the required revenue recognition approach for most long-term construction contracts under GAAP (ASC 606, as applied to construction) and for tax purposes under IRC Section 460 for contracts expected to take more than two years (or one year for certain smaller contractors).

Under POC, revenue is recognized based on the ratio of costs incurred to total estimated costs. If a job has a $1 million contract value, estimated total costs of $800,000, and costs incurred to date of $400,000, the job is 50 percent complete and $500,000 of revenue should be recognized.

The bookkeeping implications:

For the bookkeeper, the monthly task is clear: update the cost inputs, apply the POC calculation, record the revenue adjustment, and post the over/under billing entry. But "clear" and "simple" are not the same thing. The team needs to understand why they are making these entries, not just follow a template. When cost estimates change, when change orders are approved, when a job goes from profitable to unprofitable, the bookkeeper needs to recognize the implications and adjust the entries accordingly.

Some smaller contractors use the completed contract method for tax purposes (where eligible). This is simpler from a revenue recognition standpoint, but it creates different bookkeeping requirements. All costs are accumulated as an asset (construction in progress) until the job is complete, at which point all revenue and costs are recognized. The bookkeeper needs to track CIP balances and ensure costs are not prematurely expensed.

Construction bookkeeping cannot be done in a vacuum. Unlike a service business where the bookkeeper can pull bank feeds and credit card statements and work largely independently, construction accounting requires regular input from the field.

Updated cost estimates. At least monthly, the project manager or estimator needs to provide revised cost-to-complete estimates for each active job. Without this, the WIP schedule is stale and the POC calculations are unreliable.

Timesheets with job codes. Labor is a major cost category and it needs to be allocated to jobs accurately. The bookkeeper needs timesheets or time tracking data that shows which employees worked on which jobs and for how many hours.

Subcontractor invoices with job references. When a sub submits an invoice, it needs to reference the specific job and the contract or change order it relates to. Invoices that just say "progress payment" without job context create delays and potential miscoding.

Change order documentation. Approved change orders affect the contract amount, the schedule of values, and the cost estimate. The bookkeeper needs copies of approved change orders to update the job cost records and WIP schedule.

Completion percentages for billing. If the bookkeeper is preparing AIA billing, they need line-item completion percentages from the field.

At Madras, we establish a simple monthly cadence with the CPA firm and their construction clients. We provide a checklist of what we need by a specific date each month. When the information arrives, we process it. When it does not arrive on time, we follow up through the CPA firm. This is the kind of operational discipline that the first 90 days of any construction engagement need to establish firmly.

We serve CPA firms, not contractors directly. This is an important distinction. The CPA firm remains the expert advisor. We are the execution layer.

For a typical construction client, our monthly scope includes:

We work with the major construction accounting platforms:

Each platform handles job costing, WIP, and retainage differently. We do not force contractors onto a specific platform. We work with what they use.

Our quality control process for construction clients includes construction-specific review points:

The reviewer assigned to construction clients has construction accounting experience. They are not just checking that debits equal credits. They are checking that the financial story the books tell makes sense in a construction context.

Construction accounting touches several tax areas that the CPA firm needs to monitor. The bookkeeping team's accuracy directly affects:

Revenue recognition method election. The choice between percentage of completion, completed contract (where eligible), and other methods has significant tax implications. The bookkeeping records need to support whichever method the CPA firm has elected for the client.

Section 460 look-back calculations. For long-term contracts subject to Section 460, the IRS requires a look-back calculation (Form 8697) when a contract is completed. This compares the actual results to what was reported in prior years and calculates interest on any underpayment or overpayment. The bookkeeping team needs to maintain the historical data to support this calculation.

Section 199A qualified business income. Construction companies may qualify for the 199A deduction, but the calculation requires accurate income data by activity. Job costing accuracy directly affects this.

State-specific contractor taxes. Some states impose gross receipts taxes or specific contractor taxes. The bookkeeping team needs to track revenue by state for multi-state contractors.

These are the CPA firm's responsibility to manage. But the bookkeeping data needs to be clean enough to support the analysis. If job costs are miscoded or revenue recognition entries are wrong, the CPA firm is working from a corrupted foundation.

A full-time construction bookkeeper in the US with the right experience typically costs $60,000 to $80,000 in salary, plus benefits, plus the overhead of office space, software licenses, and management time. In major markets like Dallas, Phoenix, or Denver (where construction is booming), that number can go higher.

Our fully managed construction bookkeeping service, including job costing, WIP preparation, retainage tracking, and all the specialized work described above, typically costs 40 to 60 percent less than that in-house hire. And you get backup coverage, training continuity, and scalability that a single employee cannot provide. For a detailed breakdown, our outsourced accounting services guide covers pricing structures and what to expect.

For CPA firms, the math is straightforward. Outsourcing the construction bookkeeping lets you offer a high-value service to your contractor clients without building an in-house team with a very specific (and hard-to-find) skill set.

If you are a CPA firm serving construction companies and you need bookkeeping support that actually knows construction, we are ready for the conversation.

Visit madrasaccountancy.com to set up a call. We will review your construction clients' specific needs: the software they use, the types of contracts they work, the reporting the bonding company requires, and the scope of work that makes sense.

We have done this enough times to know what works and what does not. The right outsourcing partner for construction clients is not the cheapest provider. It is the one that does not force you to redo the WIP every month.

Yes, if they are specifically trained for it. Construction accounting follows defined rules and methods that can be taught systematically. What cannot be taught is the field experience to estimate costs or assess project completion. That is why our model works: we handle the bookkeeping and financial reporting, while the contractor's project managers provide the field estimates and the CPA firm provides advisory oversight. The division of responsibilities is clear.

We update the WIP schedule monthly using the latest cost-to-complete estimates from the contractor's project manager. When an estimate changes significantly, we document the change and its impact on the completion percentage and recognized revenue. We flag material changes to the CPA firm so they can discuss the implications with the client. For loss contracts (where revised estimates show total cost exceeding the contract amount), we alert the CPA firm immediately because the full expected loss needs to be recognized in the current period.

We support the major construction accounting platforms. If a contractor uses something outside our current list, we evaluate whether we can develop proficiency quickly enough to serve the client effectively. In some cases, we may recommend migration to a supported platform, but that recommendation goes through the CPA firm, and the decision is theirs. We never refuse a client solely because of their software choice without first exploring whether we can make it work.

During financial statement engagements, we provide the CPA firm with all supporting schedules, reconciliations, and documentation they need. This includes the monthly WIP schedules, retainage reconciliations, job cost detail reports, and any adjusting entries with supporting documentation. We respond to auditor inquiries routed through the CPA firm and prepare requested schedules as needed. Our goal is to make the CPA firm's engagement more efficient, not to create additional work.

Yes. We prepare certified payroll reports (WH-347) for prevailing wage projects, including Davis-Bacon Act federal projects and state prevailing wage jobs. This requires tracking employee classifications, ensuring wage rates meet the applicable wage determination, and calculating fringe benefit compliance. We work with the contractor's payroll data and the applicable wage determinations to produce compliant reports.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.