Property tax appeal accounting is a specialized service where accounting professionals challenge inflated property assessments to reduce clients' tax bills. Through strategic valuation analysis and formal appeal representation, CPAs typically achieve 15-40% assessment reductions, saving commercial property owners $50,000-$150,000 annually. The service requires expertise in real estate valuation, local tax laws, and appeals board procedures.

Property owners across the U.S. overpay $22 billion in property taxes annually because 95% never challenge their assessments, according to the National Taxpayers Union Foundation. Your commercial property's assessment might be costing you tens of thousands in unnecessary taxes, and most business owners don't realize they can fight back.

Property tax appeals have become a high-value service for accounting firms, combining technical valuation work with client advocacy. With commercial property reassessments showing 30-50% increases in many markets since 2020, appeal services now represent a critical cost-saving opportunity for property-owning businesses.

Property tax appeal accounting involves reviewing property tax assessments, identifying overvaluations, gathering supporting evidence, and formally challenging assessments through local appeals boards. Unlike general tax preparation, this specialized service requires understanding of three distinct valuation approaches: cost, market, and income methods.

Assessment overvaluation happens frequently. Local assessors evaluate thousands of properties using mass appraisal techniques and often rely on outdated data or miss property-specific factors like structural issues, economic obsolescence, or market shifts. When assessors overvalue property by even 10%, the tax implications compound annually until the next reassessment cycle.

The financial impact is substantial. A commercial property assessed at $2 million with a 2.5% local tax rate generates $50,000 in annual property tax. Reducing that assessment to $1.6 million (a 20% reduction) saves $10,000 yearly, $50,000 over a five-year reassessment cycle.

Property tax appeals represent a natural service extension for CPA firms already handling business tax compliance. The financial documentation needed for appeals, income statements, expense records, depreciation schedules, already exists in client files for firms providing tax planning and preparation services for U.S. startups.

The revenue model is attractive. Many firms work on contingency (typically 25-40% of tax savings), aligning incentives with client outcomes. With average commercial appeal savings of $50,000-$150,000, a single successful appeal generates $12,500-$60,000 in firm revenue. Unlike hourly billing, contingency work scales profitably without proportional time investment once systems are established.

Appeals work also strengthens client relationships. Processing property tax compliance and appeals gives firms deep insight into clients' real estate holdings, capital expenditures, and business operations. This knowledge naturally leads to additional service opportunities, fractional CFO services, cash flow planning, or equipment depreciation strategies under Section 179 and bonus depreciation.

The competitive advantage is timing. Property tax work is countercyclical to income tax season, providing revenue stability during slower periods. While many businesses struggle to find time for appeals during their 30-60 day filing windows, accounting firms can systematically process multiple client appeals simultaneously.

The appeal process follows a structured path across most U.S. jurisdictions. Property owners receive assessment notices typically in January-March, listing the assessed value that determines their tax bill. This triggers a narrow filing window, usually 30-60 days, to contest the valuation.

Step one involves evidence gathering. Successful appeals require documentation proving the assessed value exceeds fair market value. This includes comparable property sales data, third-party appraisals, property condition documentation, income and expense statements for commercial properties, and any special circumstances affecting value.

Filing the formal appeal typically requires submitting a written notice to the local assessment appeals board. Most jurisdictions provide forms, though some accept formal letters. The filing must clearly state the account number, proposed value, and grounds for appeal, common reasons include overvaluation compared to recent sales, incorrect property details, unequal assessment compared to similar properties, or economic factors affecting property value.

The informal review stage often comes next. Many jurisdictions encourage property owners to meet with the assessor before the formal hearing. This informal discussion can resolve 20-30% of appeals when errors are obvious (wrong square footage, outdated property classification, or mathematical mistakes in assessment calculations).

Formal hearings occur when informal resolution fails. The appeals board, typically appointed local officials or county commissioners, reviews evidence from both the property owner and assessor. Professional representation matters here. Data from Cook County, Illinois shows professional representation increases success rates from 40% to 65-70%.

If the initial appeal fails, most states offer a second-tier appeal to a state property tax commission or board of equalization. This level functions as a trial court with formal rules of evidence. Success at this stage typically requires professional appraisers and, for business entities, often legal representation.

The decision timeline varies, but boards typically render decisions within 30-90 days. Successful appeals result in revised assessments that reduce not just the current year's bill but establish a lower base value for future years, multiplying the financial benefit.

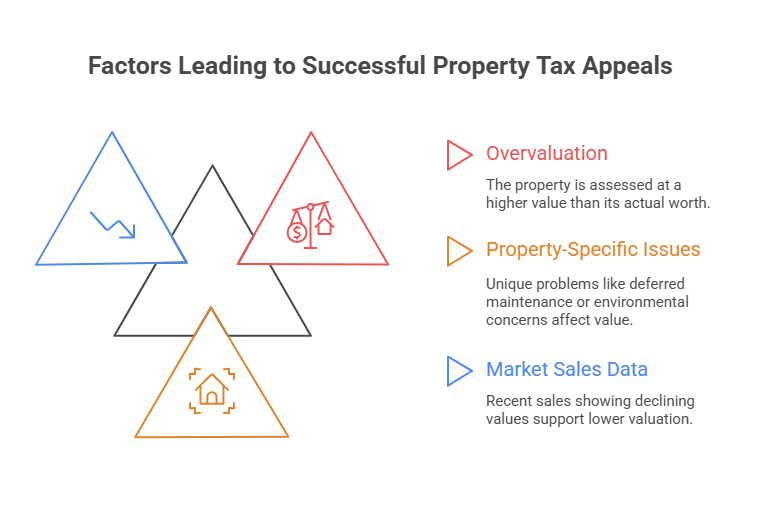

Overvaluation drives most successful appeals. Assessors use mass appraisal techniques that may not capture property-specific issues. A commercial building with deferred maintenance, environmental concerns, or outdated systems deserves a lower valuation than comparable properties in excellent condition. Recent market sales data showing declining values in the property's class or neighborhood provides strong supporting evidence.

Assessment errors offer the easiest wins. Incorrect square footage, wrong property classification (commercial vs. residential), outdated improvements (valuing a building that's been demolished), or double assessments where the same property appears twice in tax rolls are all grounds for immediate correction. About 15-20% of successful appeals stem from clerical or data errors.

Unequal assessment claims succeed when similar properties carry significantly lower assessments. Local assessors must apply consistent methodology. If three comparable office buildings in the same market have assessments of $180-$190 per square foot while yours is $240 per square foot, you have grounds for adjustment to achieve assessment equity.

Economic factors affecting value include lease-up periods for new construction, declining rental rates in your market, or increased vacancy rates in your property class. For income-producing properties, demonstrating below-market rental income or higher-than-anticipated operating expenses directly impacts valuation under the income approach.

Physical obsolescence, functional issues that reduce property value, also supports appeals. This includes poor layout, outdated building systems, environmental contamination requiring remediation, or zoning restrictions limiting property use. Professional appraisals documenting these factors strengthen appeal cases significantly.

Systematic tracking prevents missed deadlines. Firms should maintain a property tax calendar noting assessment notice arrival dates and appeal deadlines for all client properties. Missing a 30-day window means waiting an entire year (or longer in multi-year reassessment cycles) for the next appeal opportunity.

Evidence documentation must be thorough. Create a standard evidence package including comparable sales analysis (at least three similar properties sold within six months), professional appraisal (for properties over $1 million), property condition photos, income and expense statements for commercial properties, and any correspondence with the assessor documenting property issues.

Automation tools streamline multi-client management. Property tax compliance software helps firms track multiple properties, scan and organize assessment notices, extract data automatically, and maintain secure document databases accessible during appeals. For firms managing outsourced accounting services, integrating property tax tracking into existing workflows is essential.

Professional appraisals carry significant weight with appeals boards. While comparable sales data helps, third-party appraisals from licensed professionals provide independent valuation support that assessors find harder to dismiss. The $2,000-$5,000 appraisal cost is justified when potential savings exceed $30,000.

Strategic client selection maximizes firm ROI. Focus appeals efforts on commercial properties over $500,000 in value, recent assessment increases exceeding 20%, properties in markets with declining values, and clients with multiple properties enabling portfolio-wide appeals strategies.

Commercial real estate requires income approach analysis. Office buildings, retail centers, and industrial properties are valued primarily on their income-generating capacity. Accounting firms can leverage their financial expertise by demonstrating declining net operating income, increased vacancy rates, or below-market rents that justify lower valuations.

Residential investment properties benefit from sales comparison approaches. Gathering recent comparable sales within a half-mile radius provides strong evidence. For multi-family properties, rental income analysis combined with comparable sales creates a compelling two-pronged appeal strategy.

Vacant land and development properties often face overvaluation. Assessors may not account for development restrictions, environmental issues, or market absorption rates. Understanding state and local tax nuances helps build strong cases for vacant property appeals.

Personal property appeals (business equipment, furniture, fixtures) represent an overlooked opportunity. Many businesses don't realize tangible personal property is separately assessed. Depreciation schedules and disposal records can demonstrate overvalued equipment assessments, generating significant savings for manufacturing and retail clients.

Recent purchases near assessment value limit appeal success. If you bought property six months ago for $2 million and it's assessed at $2.1 million, appeals boards view the sale as strong market value evidence. The 5% differential typically won't justify appeal costs unless you can prove the sale included unique circumstances.

Rising market conditions work against appeals. In rapidly appreciating markets, even if your assessment seems high today, it may reflect fair market value. Appeals boards review recent sales data, if comparable properties are selling at or above your assessment, success becomes unlikely.

Cost-benefit analysis matters. For properties with potential savings under $5,000 annually, professional appeal services may not justify their cost. Small residential properties or low-value commercial spaces often fall into this category unless clerical errors are obvious.

Recent improvements require caution. Adding square footage, renovating, or improving property increases fair market value. Filing an appeal might prompt the assessor to inspect and discover improvements not yet reflected in the assessment, potentially raising your valuation rather than lowering it.

Since 2015, Madras Accountancy has helped U.S. businesses optimize their complete tax strategy, including property tax compliance and planning. While we specialize in comprehensive accounting and tax preparation for growing businesses, our expertise in navigating complex state and local tax issues positions us to guide clients through property tax assessment challenges.

Our approach integrates property tax planning into broader financial strategy. We work with clients to maintain proper documentation supporting lower valuations, identify optimal timing for property improvements to minimize assessment impacts, and coordinate with specialized property tax counsel when appeals require litigation support.

Key Statistics:

Property tax appeals represent a significant cost-saving opportunity that most businesses overlook. Whether you're managing a single commercial property or a multi-state real estate portfolio, understanding your appeal rights and the valuation process can save substantial annual tax dollars while establishing a more accurate assessment base for future years.

How long does a property tax appeal take?

Most appeals resolve within 60-90 days from filing to decision. Informal reviews with the assessor can conclude in 2-3 weeks, while formal appeals board hearings typically occur 45-60 days after filing with decisions rendered within 30 days of the hearing.

What percentage of property tax appeals succeed?

Success rates vary by jurisdiction but average 40-50% for self-represented property owners and 65-75% with professional representation. About one-third of appeals result in partial reductions, one-third achieve full requested reductions, and one-third are denied.

Can I appeal my property tax assessment every year?

Most jurisdictions allow annual appeals, though reassessment cycles vary. Some areas reassess annually while others use 3-5 year cycles. You can typically appeal each year within the designated filing window, but repeated appeals without new evidence become less effective.

Do I need a lawyer to appeal property taxes?

Not for most appeals. Initial appeals to local boards don't require legal representation. Accounting professionals, appraisers, or property owners can represent themselves. Legal counsel becomes valuable for state-level appeals, complex commercial properties, or litigation.

What evidence do I need for a property tax appeal?

Strong appeals include comparable sales data from the past 6-12 months, professional appraisal reports, property condition documentation including photos, income and expense statements for commercial properties, and any correspondence documenting assessment errors or special circumstances.

Will appealing increase my property tax assessment?

Generally no. Most jurisdictions prohibit increasing assessments during appeal proceedings. However, appeals may prompt closer property inspection, potentially revealing previously undocumented improvements. Never appeal if you've made unreported improvements without consulting a professional.

How much does it cost to appeal property taxes?

Filing appeals is typically free. Professional representation costs vary: property tax consultants often work on contingency (25-40% of savings), while CPAs may charge hourly ($150-$400/hour) or flat fees ($1,000-$5,000 depending on property complexity). Professional appraisals cost $2,000-$5,000.

What is the deadline to file a property tax appeal?

Deadlines vary by jurisdiction but typically range from 30-60 days after receiving your assessment notice. Some areas have specific calendar dates (often April-May) regardless of when notices arrive. Missing the deadline means waiting until the next appeal period, usually one year or longer.

Related read: property tax.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.