Direct Answer: Section 179 deductions are available for rental property, but only if your rental activity qualifies as a trade or business (not passive investment) and only for specific property types. You can expense tangible personal property like appliances and furniture in residential rentals. For commercial properties, qualified improvement property (QIP), roofs, HVAC systems, and fire/security systems also qualify. The IRS requires active management involvement and profit motive to establish business status.

You've purchased appliances, equipment, or made improvements to your rental property. Now you're looking at potential tax benefits. The Section 179 deduction promises immediate expensing instead of years of depreciation, but rental property rules are complex and widely misunderstood. Many tax professionals still believe Section 179 doesn't apply to rentals at all, costing property owners thousands in missed deductions.

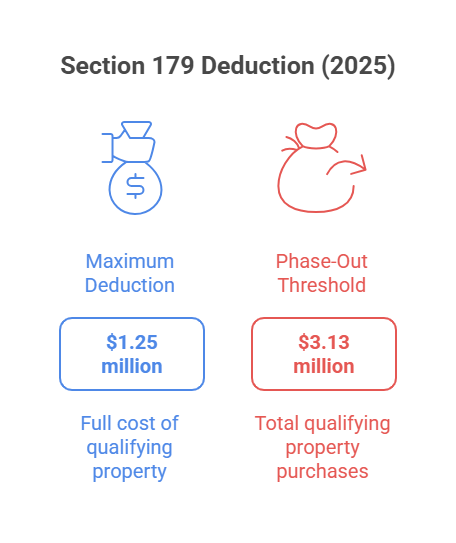

Section 179 of the Internal Revenue Code allows businesses to deduct the full cost of qualifying property in the year it's placed in service, rather than depreciating it over multiple years. For 2025, the maximum deduction is $1.25 million, with a phase-out beginning when total qualifying property purchases exceed $3.13 million.

Before the Tax Cuts and Jobs Act of 2017, Section 179 was effectively unavailable for residential rental property. The law changed starting in 2018, expanding eligibility to include personal property used in residential rentals. However, confusion persists because many tax professionals aren't aware of these changes or misunderstand the eligibility requirements.

The fundamental requirement is that property must be acquired for use in a trade or business, as defined by Section 162 of the tax code. This distinction between "trade or business" versus "investment" determines whether Section 179 applies to your rental property.

The IRS doesn't automatically consider rental property ownership a trade or business. According to IRS Publication 946, property acquired only for the production of income, such as investment property or rental property where renting is not your trade or business, doesn't qualify for Section 179 deductions.

The Supreme Court defines "trade or business" as an activity conducted with continuity and regularity, with the primary purpose of earning income or making profit. For rental property, this means you must be actively involved in management activities, not merely collecting rent checks.

Courts have established that even a single rental property can qualify as a business if managed properly. Key factors include regular and systematic involvement in property management decisions, active participation in tenant selection and lease negotiations, direct oversight of maintenance and repairs, documented involvement in marketing vacancies, and profit motive with organized business operations.

You can hire property managers or agents while maintaining business status, as long as you remain actively involved in strategic decisions. Setting rental policies, approving major expenses, and directing overall property operations demonstrate active management. Understanding these requirements helps ensure your rental activities qualify for Section 179 benefits and proper tax planning strategies that maximize legitimate deductions.

Qualifying property differs significantly between residential and commercial rentals. For residential rental property (average tenant stays exceeding 30 days), Section 179 applies to tangible personal property not permanently attached to land or buildings. This includes appliances like refrigerators, stoves, washers, dryers, and dishwashers, furniture provided to tenants, carpets, rugs, drapes, blinds, and window treatments, removable items like portable air conditioners or heaters, and maintenance equipment used in rental operations.

You can also expense property used for rental business operations but not located inside rental units, such as office furniture and equipment for your rental business office, computers and software for property management, tools and equipment for maintenance work, and vehicles used primarily for rental business purposes.

Section 179 cannot be used for residential rental buildings themselves, structural components like plumbing or electrical systems, permanent improvements attached to land such as fences, walkways, swimming pools, or paved parking areas, or land and landscaping.

For commercial rental property and short-term rentals (average stays under 30 days), eligibility expands significantly to include qualified improvement property (QIP), which covers most interior improvements made after the building is first placed in service, excluding structural framework, elevators, and escalators, roofs, HVAC systems, fire protection and alarm systems, and security systems.

The deduction cannot exceed your taxable business income for the year. For rental property owners, this means your net rental income (gross rental income minus expenses) limits your Section 179 deduction. If you claim $10,000 in Section 179 deductions but only have $7,000 in net rental income, you can deduct only $7,000 currently.

The $3,000 excess carries forward to future tax years when you have sufficient income. This income limitation prevents Section 179 from creating losses. If you're married filing jointly, your spouse's salary and business income can increase your available income for Section 179 purposes.

Property must maintain at least 50% business use throughout its depreciation period. If business use drops below 50%, the IRS requires depreciation recapture, you report previously claimed deductions as taxable income. For a vehicle with a five-year depreciation period, you must maintain more than 50% business use for all five years to avoid recapture.

To claim Section 179, complete Part I of IRS Form 4562 and attach it to your tax return. The election is not automatic, you must actively choose to use Section 179 rather than regular depreciation. Strategic planning around which assets to expense versus depreciate can significantly impact your tax position, making consultation with professionals experienced in Section 179 and bonus depreciation strategies valuable for maximizing benefits.

Both Section 179 and bonus depreciation accelerate deductions, but they work differently. Section 179 is an election allowing you to expense qualifying property up to annual limits. Bonus depreciation is a percentage deduction (40% in 2025, phasing down from previous years) applied after Section 179 but before regular depreciation.

Key differences include income limitations. Section 179 cannot exceed taxable business income, while bonus depreciation has no income requirement and can create losses. Property limits also differ, Section 179 has dollar limits ($1.25 million for 2025) and phase-outs, while bonus depreciation has no such caps.

Section 179 requires an active election on Form 4562, while bonus depreciation applies automatically unless you opt out. For timing flexibility, Section 179 offers more control, as you can choose which specific assets to expense and in what amounts.

Real property treatment varies significantly. Section 179 can apply to qualified improvement property on commercial rentals, while bonus depreciation applies to a broader range of property types. Section 179 may be preferable when you have limited taxable income and want to maximize current-year deductions without creating losses, need flexibility to choose specific assets to expense, or want to carry forward unused deductions to future years.

Bonus depreciation works better when you have high income and want to create losses to offset other income, have property that doesn't qualify for Section 179, or prefer automatic application without annual elections.

The most costly error is assuming Section 179 doesn't apply to rental property at all. Many owners miss thousands in legitimate deductions because they or their tax preparers aren't aware of post-2017 law changes. This knowledge gap particularly affects residential rental property owners who could be expensing appliances, carpets, and other personal property.

Failing to establish trade or business status creates problems. Passive investors who don't actively manage properties cannot use Section 179. Document your involvement in property management decisions, maintain records of time spent on rental activities, and demonstrate regular, systematic engagement with your rental business.

Mixing property types causes confusion. Section 179 eligibility differs between residential (30+ day average stays) and commercial properties. Short-term rentals under 30 days average stay qualify for expanded Section 179 treatment similar to commercial property, including qualified improvement property deductions.

Ignoring the 50% business use requirement leads to recapture issues. If you purchase equipment or vehicles for rental property use, maintain detailed logs proving business use exceeds 50% throughout the depreciation period. Personal use above 50% disqualifies the property from Section 179 and may trigger recapture of previously claimed deductions.

Missing the income limitation causes problems. Section 179 cannot exceed net taxable business income. Calculate your net rental income before claiming Section 179 deductions. Excess deductions carry forward but don't provide current-year benefits, so strategic planning around timing and property selection matters.

Section 179 doesn't eliminate depreciation, it's essentially accelerated depreciation claimed in year one. Properties expensed under Section 179 still appear on your depreciation schedule with full basis immediately deducted. This matters for depreciation recapture when you sell the property or if business use drops below required thresholds.

Qualified improvement property creates unique opportunities for commercial rental owners. Post-2017 law expanded Section 179 eligibility to include interior improvements, roofs, HVAC, and fire/security systems. These improvements, when combined with cost segregation studies, can generate substantial immediate deductions.

Real estate professional status amplifies Section 179 benefits. If you qualify as a real estate professional under IRS rules (spending 750+ hours annually in real property trades or businesses and more than 50% of working hours in those activities), rental losses from Section 179 deductions can offset all income types rather than being limited to passive income. Working with advisors who understand both IRS audit risks and proper documentation requirements helps ensure your Section 179 claims withstand scrutiny.

The IRS requires comprehensive documentation to support Section 179 deductions. Maintain purchase receipts and invoices showing property description, cost, purchase date, and seller information. Keep records proving the property was placed in service during the tax year you're claiming the deduction.

Document business use percentage for all Section 179 property. For vehicles and equipment with mixed personal and business use, maintain detailed logs showing dates, purposes, and miles or hours of business use. These logs must demonstrate business use exceeds 50% throughout the depreciation period.

Evidence of active trade or business status is critical. Keep records of time spent on rental activities, property management decisions, tenant communications, and marketing efforts. Document involvement in repairs, maintenance scheduling, lease negotiations, and financial management. This evidence proves your rental activity meets the "trade or business" requirement.

Form 4562 must be completed correctly and filed with your tax return. Part I of the form details your Section 179 election, including specific property descriptions and amounts being expensed. Errors or omissions on this form can result in disallowed deductions.

Section 179 makes sense when you have sufficient net rental income to absorb the deduction. If your rental properties generate $50,000 in net income and you're purchasing $30,000 in qualifying equipment, Section 179 provides immediate tax benefits. Without adequate income, the deduction carries forward with delayed benefits.

Property owners planning significant purchases of qualifying property should consider timing. Purchasing and placing property in service before year-end allows current-year deductions. Strategic timing around high-income years maximizes the value of accelerated deductions.

Commercial property owners making interior improvements, roof replacements, or HVAC upgrades gain substantial benefits from Section 179. These improvements, previously requiring 39-year depreciation schedules, can now be expensed immediately under the expanded qualified improvement property rules.

Coordination with other tax strategies matters. If you're also conducting cost segregation studies, utilizing 1031 exchanges, or managing passive activity losses, Section 179 decisions should fit within your overall tax plan. Professional guidance from specialists in comprehensive tax planning and preparation services ensures these strategies work together effectively.

Yes, courts have held that ownership of even a single rental property can qualify as a trade or business if you actively manage it. The key is demonstrating regular, systematic involvement in property management decisions, tenant relations, and maintenance oversight. Document your activities to prove business status rather than passive investment.

The maximum Section 179 deduction is $1.25 million for 2025, with a phase-out beginning when qualifying property purchases exceed $3.13 million. However, your actual deduction is further limited by your net taxable business income from the rental activity. Deductions exceeding your income carry forward to future tax years.

Yes, hiring a property manager doesn't disqualify you from Section 179 deductions. You must remain actively involved in strategic decisions, setting policies, approving major expenses, selecting tenants, and directing overall operations. Delegation of day-to-day management is acceptable as long as you maintain active business involvement.

Short-term rentals with average stays under 30 days qualify for expanded Section 179 treatment similar to commercial property. This includes qualified improvement property for interior improvements, roofs, HVAC, and fire/security systems. These properties often qualify more easily as a trade or business due to higher management involvement.

When you sell property previously expensed under Section 179, you face depreciation recapture. The IRS requires you to report the previously deducted amount as ordinary income, taxed at your regular rate rather than capital gains rates. This recapture applies to the extent of gain on the sale.

For residential rentals, improvements permanently attached to the property don't qualify for Section 179, only removable personal property qualifies. For commercial rentals, qualified improvement property (most interior improvements), roofs, HVAC, and fire/security systems qualify for Section 179 if made after the building is first placed in service.

Section 179 provides immediate deductions rather than spreading them over years, creating cash flow benefits when you have adequate taxable income. However, it may not be optimal if current-year income is low, if you prefer spreading deductions over multiple years, or if bonus depreciation offers better benefits for your situation.

Maintain detailed logs of time spent on rental activities, documentation of property management decisions, records of tenant communications and lease negotiations, evidence of involvement in repairs and maintenance planning, and financial records showing regular oversight of rental operations. These records prove your rental activity constitutes a trade or business.

Section 179 deductions offer significant tax benefits for rental property owners, but eligibility requirements are specific and often misunderstood. Your rental activity must qualify as a trade or business through active management involvement, not passive investment. Qualifying property types differ between residential and commercial rentals, with expanded opportunities for commercial properties and short-term rentals. The income limitation means you need sufficient net rental income to utilize Section 179 deductions currently, though excess amounts carry forward.

Property must maintain at least 50% business use throughout its depreciation period to avoid recapture. Strategic use of Section 179, particularly when combined with cost segregation studies and proper entity structuring, can substantially reduce tax liability.

Since 2015, Madras Accountancy has partnered with U.S. CPA firms and real estate investors to navigate complex depreciation strategies, including Section 179 elections and bonus depreciation planning. Our team understands the documentation requirements, eligibility criteria, and strategic considerations that maximize tax benefits while ensuring IRS compliance for rental property portfolios of all sizes.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.