Tri-state real estate bookkeeping services provide specialized financial management for property investors operating across New York, New Jersey, and Connecticut. These services handle multi-state tax compliance, property-level accounting, and 1031 exchanges while navigating each state's unique tax codes. Professional CPAs reduce tax liabilities by 30-35% on average through strategic expense categorization that generalist accountants miss.

You own four rentals, two in Manhattan, one in Hoboken, one in Stamford. Last April, your general accountant missed New Jersey's reciprocal tax agreement, overpaid Connecticut estate tax by $8,000, and misclassified a capital improvement. Total cost: $14,000 in back taxes and penalties.

This happens constantly where property investors cross state lines but accountants don't understand the nuances.

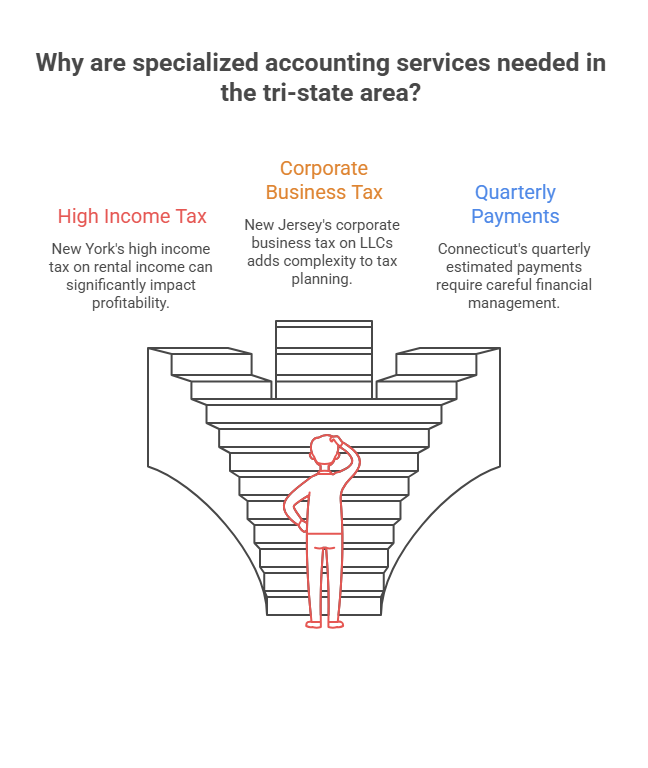

The tri-state area presents unique accounting challenges. New York imposes the highest state income tax on rental income (up to 10.9%), New Jersey adds separate corporate business tax on LLCs, and Connecticut requires quarterly estimated payments with different rules than federal.

Each state treats depreciation, passive losses, and property tax deductions differently. New York doesn't conform to federal bonus depreciation rules. New Jersey caps property tax deductions at $15,000. Connecticut taxes capital gains at ordinary income rates up to 6.99%.

CPAs specializing in tri-state real estate track these rules daily, saving clients $12,000-$25,000 annually in avoided penalties and optimized deductions. Missing a single New Jersey filing deadline triggers automatic 5% penalties plus interest.

Multi-Property Accounting: Specialized firms maintain separate books for each property while consolidating for owner-level reporting. You receive monthly P&L statements showing which assets perform. Software integrates with property management platforms, automatically categorizing rent, expenses, and contractor payments.

Cross-State Tax Preparation: CPAs file federal returns (1040 Schedule E, partnership 1065s), plus separate returns for New York (IT-203), New Jersey (NJ-1040), and Connecticut (CT-1040). They calculate pro-rata allocations, apply reciprocal agreements, and claim credits for taxes paid to other states, preventing double taxation.

Strategic Tax Planning: Cost segregation studies accelerate depreciation, generating $40,000-$100,000 in first-year deductions for properties above $1 million. CPAs structure 1031 exchanges and advise on entity formation. Real estate professional status unlocks unlimited passive loss deductions, saving $15,000-$30,000 annually for active investors.

Audit Support: When audited, your CPA responds to requests, organizes documentation, and represents you in hearings. Most audits close with no additional tax owed when proper documentation exists.

Essential Qualifications: Look for CPAs where 60%+ of clients are real estate investors and who actively manage 30+ tri-state portfolios. Request references from similar portfolios. Verify they use real estate-specific software (AppFolio, Buildium, Rent Manager) rather than generic QuickBooks.

Technology Standards: Modern real estate accounting requires cloud-based systems with real-time dashboards. Integration with property management software eliminates double-entry. Establish communication expectations, quarterly meetings work for most investors, with 24-hour response times during business days.

Pricing Models: Expect $200-$400 monthly per property for full bookkeeping, plus $800-$2,000 per state return annually. Volume discounts start at 10 properties. Most investors see 4:1 to 8:1 returns through better tax planning. Avoid hourly billing without fee caps.

Using General Accountants for Real Estate: Your personal tax preparer likely doesn't understand passive activity loss rules, depreciation recapture, or multi-state nexus. They'll miss deductions, attempting to save $2,000 in CPA fees costs $10,000 in lost deductions.

Not Tracking State-Specific Basis: NY, NJ, and CT each maintain different basis calculations for depreciation. When you sell, incorrect tracking triggers overpayment. Professional bookkeeping services track state-by-state differences from acquisition through disposition.

Mixing Personal and Rental Finances: Using one account creates impossible audit records. Open dedicated accounts per property. This prevents 80% of audit problems.

Portfolio Thresholds: Single-property owners in one state can manage with general CPAs. At 3-4 properties or when crossing state lines, specialized services pay for themselves. At 10+ properties, professional bookkeeping becomes essential.

Calculate breakeven: If specialized services cost $5,000 more annually but save $18,000 through better tax planning, you gain $13,000 net value.

Immediate Need Indicators: Hire specialists if you're completing 1031 exchanges, own properties in multiple states, pursuing real estate professional status, earning $150,000+ in rental income, or syndicating deals. The ROI of outsourcing accounting services typically reaches 300-500% for these categories.

We've provided real estate bookkeeping and tax services for 500+ investment properties across the tri-state area since 2015. Our CPAs are licensed in NY, NJ, and CT with specific expertise in cross-state compliance.

We maintain property-level books, integrate with major property management platforms, and deliver monthly financial statements. Our clients average $14,000 in annual tax savings through depreciation optimization and meticulous compliance. Finding a qualified CPA for real estate typically means premium rates, our offshore model delivers the same expertise with better value.

Do I need separate bookkeepers for properties in different states?

No. One specialized service handles all properties across NY, NJ, and CT, maintaining property-level detail while managing multi-state tax compliance through a unified system.

How much do tri-state real estate bookkeeping services cost?

Expect $200-$400 monthly per property plus $800-$2,000 per state for annual tax prep. A four-property portfolio spanning two states runs $1,200-$1,800 monthly. This typically returns 3-5x through tax savings.

Can I switch accountants mid-year without problems?

Yes, though transitions work best at year-end. Your new CPA requests prior-year returns and current books. Most transitions complete in 2-4 weeks.

What records do I need to provide?

Monthly bank statements, receipts, rent rolls, property management reports, loan statements, and closing documents. Cloud systems automate most data flow through property management software integration.

How do CPAs handle audit representation?

Licensed CPAs represent you before IRS and state authorities, responding to requests, preparing documentation, and attending hearings. Most audits resolve without additional tax owed. Representation typically costs $2,000-$5,000.

Should I form LLCs in Delaware or the property state?

Form LLCs where the property sits. Delaware offers no tax advantage for rentals, you'll still file and pay taxes in NY, NJ, or CT. Delaware adds unnecessary fees without benefit.

Do I need a CPA for one rental property?

One property might not justify specialized services immediately. Once rental income exceeds $50,000 annually or you're considering additional purchases, professional guidance prevents costly mistakes.

How often should I meet with my CPA?

Quarterly meetings work for most investors, reviewing performance, estimated taxes, and decisions. Monthly communication makes sense during acquisition periods.

Real estate investors across New York, New Jersey, and Connecticut face tax complexity that generalist accountants can't navigate. Specialized expertise returns 3-5x its cost through eliminated penalties and optimized deductions.

Request a portfolio review from tri-state real estate CPAs this week. Bring prior-year returns, property lists, and questions about your situation.

Contact Madras Accountancy to discuss how tri-state real estate bookkeeping supports your investment goals. We'll identify immediate tax-saving opportunities tailored to your portfolio across NY, NJ, and CT.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.