What Are the Accounting Implications of Rent Escalation Clauses?

Rent escalation clauses require straight-line expense recognition under ASC 842, meaning tenants must average total lease payments across the entire lease term rather than recording actual monthly payments. This creates a right-of-use (ROU) asset and lease liability on the balance sheet, eliminating the previous deferred rent account. The escalation impacts both financial statements and tax deductions, as actual cash payments differ from recognized expenses throughout the lease.

Your commercial lease just renewed with a 3% annual rent escalation. Month one, you're paying $10,000. Year five? That's $11,255. Your bookkeeper records the actual payment, but your auditor says you need to recognize $10,613 every month for the entire five years.

Welcome to rent escalation accounting under ASC 842. Most commercial tenants handle escalating rent payments incorrectly, creating audit issues, distorting financial statements, and missing tax planning opportunities. The stakes are high, 9 out of 10 companies miss lease escalations monthly, leaving money on the table or facing compliance problems.

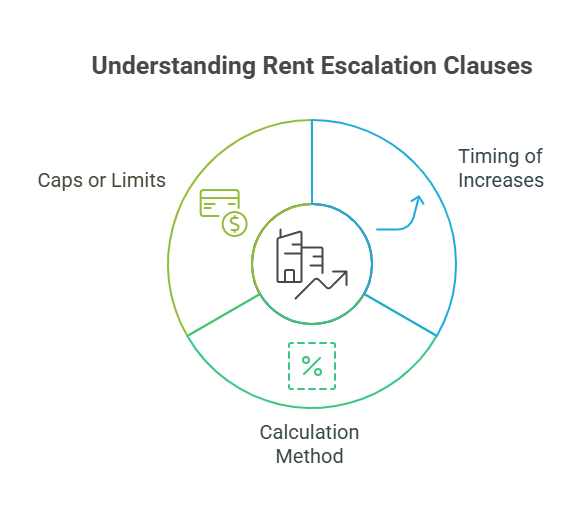

A rent escalation clause is a provision in a commercial lease agreement that allows landlords to increase rent periodically over the lease term. These clauses protect landlords against inflation while giving tenants predictable cost structures for budgeting.

The clause specifies three key elements: timing of increases (annually, every 3-5 years), calculation method (fixed percentage, CPI-based, or operating expense pass-through), and any caps or limits on maximum increases. Most commercial leases include escalations, without them, landlords can't keep pace with rising property taxes, insurance, and maintenance costs.

Escalation types vary significantly. Fixed escalations might increase rent by 3% annually or $0.50 per square foot each year. CPI-based escalations tie increases to the Consumer Price Index published by the U.S. Bureau of Labor Statistics, adjusting automatically for inflation. Operating expense escalations pass through increases in property taxes, common area maintenance (CAM), or insurance costs to tenants based on their proportionate share of the building.

Tax pass-through provisions deserve special attention. When a landlord's property taxes increase, tenants pay their proportionate share based on leased square footage. A tenant occupying 5,000 square feet in a 100,000-square-foot building covers 5% of any tax increases above the base year.

Rent escalation clauses complicate accounting because actual cash payments don't match expense recognition requirements. Under Generally Accepted Accounting Principles (GAAP), operating lease expenses must be recognized on a straight-line basis over the entire lease term.

Here's the problem: Year one, you're paying $120,000 annually ($10,000/month). Year five, you're paying $138,423 annually ($11,535/month) with 3% annual escalations. GAAP requires you to recognize $127,403 annually ($10,617/month) every single year, the average of all payments.

This timing difference between cash payments and expense recognition creates balance sheet accounts that didn't exist under cash-basis accounting. In early years, when you're paying less than the straight-line expense, you're accumulating a liability. Later, when payments exceed straight-line expense, that liability burns off.

ASC 842, the current lease accounting standard effective since 2019 for public companies and 2022 for private companies, completely changed how these timing differences appear on financial statements. The old deferred rent liability account disappeared, replaced by adjustments to the right-of-use asset and lease liability.

For property management companies and commercial tenants managing multiple leases, tracking escalations across dozens of properties becomes overwhelming without specialized lease accounting software. Missing an escalation means your financial statements misstate both assets and liabilities, affecting debt covenants and lending ratios.

ASC 842 fundamentally transformed lease accounting by requiring lessees to recognize nearly all leases on the balance sheet. Before ASC 842, operating leases stayed off-balance sheet entirely, appearing only as footnote disclosures.

Under the previous standard (ASC 840), accountants handled escalating payments through three accounts: prepaid rent (asset), deferred rent (liability), and accrued rent (liability). When straight-line expense exceeded cash paid, deferred rent accumulated. When cash payments exceeded straight-line expense in later years, deferred rent decreased.

ASC 842 eliminated these separate accounts. Now, everything flows through two accounts: the right-of-use asset and lease liability. At lease commencement, you calculate the present value of all future lease payments (including known escalations) and record both an ROU asset and lease liability for that amount.

The calculation works like this: Sum all lease payments over the term, discount to present value using your incremental borrowing rate, and record the result. For a 5-year lease with $10,000 base rent and 3% annual escalations, total payments equal $636,018. At a 5% discount rate, the present value is approximately $567,000, both your initial ROU asset and lease liability.

Each month, you recognize straight-line rent expense, reduce the lease liability by the cash payment, and record interest expense on the remaining liability balance. The ROU asset amortizes over the lease term. These mechanics ensure the balance sheet always reflects your remaining lease obligations.

Understanding how to read and interpret financial statements becomes critical when lease accounting changes impact key ratios that lenders and investors monitor.

Straight-line rent expense calculation follows a simple formula: total lease payments divided by total months in the lease term. The challenge lies in identifying all components that qualify as lease payments.

Start with base rent payments. A 60-month lease with $10,000 monthly base rent in year one, escalating 3% annually, totals $636,018 over five years. Divide by 60 months to get $10,600 monthly straight-line expense.

Include rent-free periods in your calculation. Many leases offer 3-6 months free rent upfront. These months count toward the lease term for straight-line calculations. A 63-month lease (60 months paid plus 3 months free) with $636,018 total payments yields $10,096 monthly straight-line expense, lower than the example above because you're spreading payments over more months.

Add lease incentives received from landlords. Tenant improvement allowances reduce your total lease cost. If a landlord provides $50,000 for buildout, subtract this from total payments before calculating straight-line expense. Your effective lease cost is now $586,018, reducing monthly straight-line expense to $9,302.

Exclude variable lease payments not based on an index or rate. Percentage rent based on gross sales, CAM charges that fluctuate with actual costs, and utility reimbursements aren't included in lease liability calculations. These remain period expenses as incurred.

The calculation grows more complex with step-up increases. A lease might specify $10,000 monthly for years 1-2, $11,000 for years 3-4, and $12,000 for year 5. Sum all payments ($648,000), divide by 60 months, and recognize $10,800 monthly regardless of actual payment amounts.

ASC 842 requires lessees to recognize a right-of-use asset and corresponding lease liability at lease commencement. These accounts dramatically increase reported assets and liabilities, affecting financial ratios and debt covenant compliance.

The lease liability equals the present value of future lease payments, calculated using your incremental borrowing rate (IBR), the rate you'd pay to borrow money for a similar term. Most companies use rates between 3-8% depending on creditworthiness and current market conditions.

The ROU asset calculation starts with the lease liability, then adjusts for: prepaid rent (adds to asset), lease incentives received (reduces asset), and initial direct costs paid (adds to asset). These adjustments ensure the ROU asset reflects your net investment in the lease.

Here's a practical example: Your 5-year lease has a present value of $567,000 at lease commencement. You paid $15,000 in broker fees (initial direct costs) and received a $30,000 tenant improvement allowance. Your initial ROU asset is $552,000 ($567,000 + $15,000 - $30,000).

Each month, two things happen simultaneously. First, you reduce the lease liability by your cash payment and record interest expense on the remaining balance. Second, you amortize the ROU asset on a straight-line basis over the lease term. The sum of ROU amortization and interest expense equals your straight-line rent expense.

Financial statement readers must understand these balance sheet accounts. A company with $10 million in operating leases previously showed zero lease assets or liabilities pre-ASC 842. Post-adoption, both assets and liabilities increased by $9-10 million, significantly impacting the debt-to-equity ratio and current ratio.

For growing businesses managing lease portfolios, scaling your finance department becomes essential when ASC 842 compliance requires specialized expertise beyond basic bookkeeping.

Operating lease expenses under ASC 842 remain remarkably similar to pre-ASC 842 treatment, straight-line recognition over the lease term. The mechanics changed, but the income statement impact stayed largely consistent.

Your monthly journal entry records total lease expense (the straight-line amount) as a debit. On the credit side, you reduce the lease liability by the cash payment amount and adjust the ROU asset for the difference. This keeps your total expense constant despite varying cash payments.

Here's the monthly entry for a $10,617 straight-line expense with a $10,000 cash payment:

Debit: Lease Expense $10,617

Credit: Cash $10,000

Credit: ROU Asset (amortization) $617

The $617 difference represents the timing gap between your straight-line expense and actual cash payment. In later years when cash payments exceed straight-line expense, the ROU asset credit reverses to a debit.

Interest expense appears separately for finance leases but gets bundled into total lease expense for operating leases. This distinction matters for EBITDA calculations, operating lease expenses reduce EBITDA, while finance lease interest doesn't.

Companies transitioning from ASC 840 to ASC 842 should see minimal change in total rent expense if they previously used straight-line recognition correctly. However, many companies discover they were recording cash-basis rent all along, requiring them to restate historical periods.

Watch for expense pattern changes with variable lease components. CPI-based escalations require reassessment annually when the new CPI index publishes. Your straight-line calculation updates to reflect the new payment schedule, creating a catch-up adjustment in the reassessment period.

Tax treatment of rent escalations diverges significantly from GAAP accounting, creating temporary differences that impact deferred tax calculations. The IRS generally permits cash-basis deductions for rent payments, regardless of when you recognize the expense for financial reporting.

Here's the divergence: Year one, you recognize $127,403 rent expense on your GAAP financial statements but only pay $120,000 cash. For tax purposes, you deduct $120,000. This creates a $7,403 unfavorable temporary difference, you're recognizing more expense for book purposes than tax purposes.

Year five flips the situation. Your GAAP expense remains $127,403, but you're paying $138,423 cash. Tax deduction exceeds book expense by $11,020, reversing the earlier unfavorable difference.

These temporary differences require deferred tax accounting. In year one, you record a deferred tax asset for the $7,403 difference multiplied by your tax rate (assume 21%). The entry creates a $1,555 deferred tax asset that reverses in later years when tax deductions exceed book expenses.

Companies must track these differences carefully across multiple leases. A portfolio of 50 leases with various escalation patterns creates complex deferred tax calculations requiring specialized software or expertise.

Operating expense pass-throughs receive different treatment. When you pay additional rent for increased property taxes or CAM charges, these costs are immediately deductible as operating expenses. No temporary differences arise because both book and tax recognize the expense when incurred.

Tax planning strategies around lease structuring can significantly impact your effective tax rate, especially when negotiating new leases or renewal options.

Most accounting mistakes with rent escalations stem from misunderstanding ASC 842 requirements or failing to implement proper controls around lease data management.

Recording cash payments as expense. This remains the most common error. Accountants familiar with pre-ASC 842 practices continue recording actual monthly payments rather than calculating straight-line expense. The fix requires reviewing every lease, calculating correct straight-line amounts, and posting catch-up adjustments.

Excluding free rent periods from calculations. Rent-free months must be included in both the lease term and straight-line calculation. Many companies mistakenly start recognizing expense only when cash payments begin, understating early-year expenses and overstating later years.

Misclassifying lease incentives. Tenant improvement allowances should reduce the ROU asset, not appear as separate income. Receiving $50,000 from a landlord for buildout isn't revenue, it's a reduction in your net lease cost that affects straight-line expense calculations.

Failing to update for remeasurement events. When lease terms change, payment amounts adjust, or renewal options become reasonably certain to exercise, you must remeasure the lease liability and ROU asset. Companies often overlook these triggering events, leaving outdated calculations on the books.

Incorrect discount rates. The incremental borrowing rate significantly impacts lease liability calculations. Using a company-wide rate (like your term loan rate) when individual leases have different terms creates measurement errors. A 5-year lease requires a 5-year IBR, not your 10-year debt rate.

Neglecting lease modifications. Rent escalation clause amendments, early termination options added mid-lease, or space expansions constitute lease modifications requiring specific accounting treatment. These don't simply adjust existing balances, they require new present value calculations.

Property management companies handling accounting for multiple properties face additional complexity. Without proper lease management systems, tracking escalations across 20+ locations becomes impossible to maintain accurately.

Common accounting mistakes compound quickly when dealing with lease portfolios, making proactive error prevention more cost-effective than fixing problems during audits.

Manual lease accounting with spreadsheets breaks down quickly once you exceed 10-15 leases. Software solutions automate calculations, generate journal entries, and maintain audit trails required for ASC 842 compliance.

Dedicated lease accounting platforms like LeaseQuery, Visual Lease, and CoStar provide end-to-end solutions. These systems store lease abstracts, calculate straight-line expense automatically, generate monthly journal entries, and produce ASC 842 disclosure reports. Pricing typically ranges from $5,000-50,000 annually depending on lease volume and company size.

The software handles complex scenarios automatically: CPI-based escalations that update annually, step-up rent structures with different rates by year, and lease modifications that require remeasurement. Instead of manual Excel calculations prone to formula errors, the system applies correct accounting standards consistently.

Integration with general ledgers eliminates manual journal entry posting. Modern platforms connect directly to QuickBooks, NetSuite, Sage, and major ERP systems, posting calculated amounts automatically each month. This reduces accounting time by 10-15 hours monthly for companies with 20+ leases.

Smaller businesses with fewer leases can use simplified solutions. QuickBooks Enterprise and Xero offer basic lease accounting modules for operating leases with straightforward terms. These handle fixed escalations well but struggle with complex CPI-indexed increases or expense pass-throughs requiring regular updates.

The key decision factors: lease volume (more than 20 suggests dedicated software), lease complexity (CPI indexing or frequent modifications require robust platforms), and internal resources (companies without dedicated lease accountants benefit more from automated solutions).

Cloud-based platforms offer additional advantages: automatic software updates when accounting standards change, multi-user access for finance teams and auditors, and built-in compliance with ASC 842 disclosure requirements. Most vendors provide implementation support and training as part of licensing fees.

Outsourcing accounting services often includes lease accounting support, providing both software expertise and technical knowledge without requiring in-house specialists.

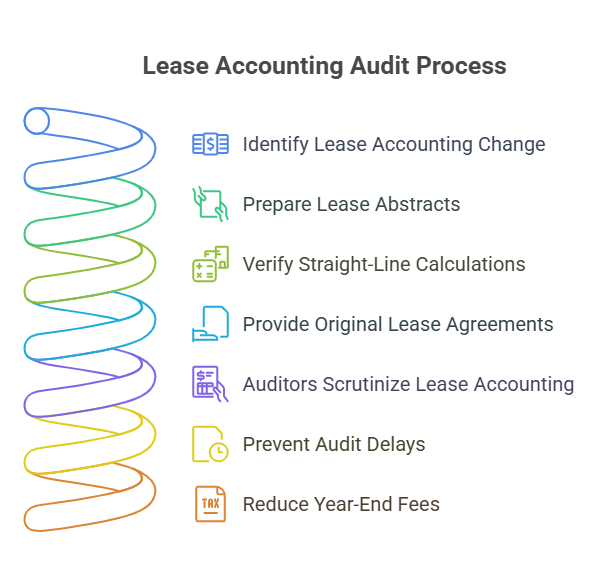

Auditors scrutinize lease accounting heavily because ASC 842 represents a significant accounting change affecting most companies. Proper documentation prevents audit delays and reduces year-end fees.

Start with complete lease abstracts documenting every relevant term: commencement date, initial monthly payment, escalation formula, rent-free periods, renewal options, and early termination clauses. Auditors need to verify your straight-line calculations independently, requiring access to original lease agreements.

Maintain calculation workpapers showing: total lease payments by year, present value discount rate and source, ROU asset initial amount and adjustments, monthly amortization schedules, and actual cash payments recorded. These workpapers create an audit trail from lease terms through financial statement amounts.

Document your incremental borrowing rate methodology. How did you determine the 5% rate used for present value calculations? Most companies reference similar-term debt, add credit spread adjustments, or obtain third-party rate assessments. Auditors expect written IBR policies describing your approach.

Track lease modifications separately with documentation explaining the accounting treatment. Did you remeasure the lease or treat the change as a separate contract? What triggered the modification? Contemporaneous documentation prevents disputes with auditors months later.

For operating expense pass-throughs, maintain supporting invoices from landlords showing actual tax increases, CAM charges, or insurance costs. These variable payments need verification that amounts billed match lease terms and actual expense increases.

Implement quarterly lease reviews identifying new leases, modifications, terminations, and upcoming renewals. This process catches accounting changes promptly rather than discovering issues during year-end close. Most companies assign lease administration responsibilities to specific team members with defined review procedures.

External auditors typically request lease accounting software access during audits, allowing them to review calculations directly rather than examining hundreds of pages of Excel workpapers. This transparency speeds audits and demonstrates strong internal controls over lease accounting.

How do rent-free periods affect straight-line rent expense calculations?

Rent-free periods must be included in both the lease term and the straight-line expense calculation. If you have a 5-year lease with 3 months free rent upfront, your lease term is 63 months total. Calculate straight-line expense by dividing total cash payments by all 63 months, not just the 60 months you're paying. This lowers your monthly expense but ensures accurate expense recognition across the entire period you control the space.

What happens to deferred rent balances when transitioning to ASC 842?

Deferred rent balances from ASC 840 are eliminated at transition, with the balance reclassified to adjust your opening right-of-use asset. If you had a $50,000 deferred rent liability, this becomes a $50,000 reduction to your initial ROU asset. The income statement impact remains similar post-transition, you'll still recognize straight-line expense, but the balance sheet presentation changes completely.

Can landlords structure escalation clauses to minimize tenant accounting complexity?

Yes, landlords can simplify tenant accounting by using fixed percentage escalations rather than CPI-based or operating expense pass-throughs. A clause stating "3% increase annually" requires one calculation at lease commencement. CPI-based clauses force tenants to remeasure annually when new index data publishes, creating ongoing complexity. This tenant-friendly approach can become a negotiation point during lease discussions.

How do variable lease payments affect ASC 842 calculations?

Variable lease payments not based on an index or rate are excluded from lease liability calculations and expensed as incurred. Percentage rent based on sales, fluctuating CAM charges, and utility reimbursements don't affect your initial ROU asset or liability. However, CPI-indexed escalations are included because they're based on a published index. This distinction significantly impacts which payments flow through the balance sheet versus income statement only.

What discount rate should tenants use for lease liability calculations?

Tenants should use their incremental borrowing rate, the rate they'd pay to borrow money for a similar term. For a 5-year lease, use a 5-year borrowing rate; for 10 years, use a 10-year rate. Most companies reference their term loan rates, add credit spread adjustments based on their credit rating, or use third-party rate services. The rate significantly impacts present value calculations, so proper determination is critical for accurate financial statements.

Do escalation clauses affect lease classification as operating versus finance?

Escalation clauses themselves don't change lease classification. The tests for finance lease classification focus on: ownership transfer, purchase options, lease term relative to asset life, present value of payments, and specialized asset characteristics. Whether rent escalates 2% or 5% annually doesn't affect these tests. However, higher escalations increase total lease payments, potentially pushing the present value above the 90% threshold that triggers finance lease classification.

How often must companies reassess CPI-based rent escalations?

Companies must reassess CPI-based escalations whenever new CPI data publishes that affects lease payments, typically annually. When the Bureau of Labor Statistics releases new CPI figures, calculate the new payment amount per your lease formula. This triggers a lease remeasurement, requiring you to recalculate the lease liability present value and adjust the ROU asset. The remeasurement happens in the period the new CPI data becomes available, not retroactively.

Should property management companies handling landlord accounting treat escalations differently?

Landlords generally account for escalating rent income on a straight-line basis, similar to tenant expense treatment. However, lessor accounting under ASC 842 differs significantly for lease classification and ongoing measurement. Landlords with operating leases recognize straight-line rental income even though cash receipts vary with escalations. For direct financing or sales-type leases, escalations affect net investment calculations and interest income recognition patterns. Most landlords benefit from specialized accounting support for complex lease portfolios.

Rent escalation accounting under ASC 842 demands more than basic bookkeeping skills. The straight-line calculation, balance sheet recognition, and documentation requirements create compliance challenges for businesses managing even modest lease portfolios.

The biggest risk isn't complexity, it's not knowing what you don't know. Companies discover lease accounting errors during audits, facing restatements, extended audit timelines, and accounting fees that dwarf the cost of getting it right initially.

Madras Accountancy provides specialized lease accounting support to U.S. businesses navigating ASC 842 compliance. Our offshore accounting teams combine technical expertise in lease standards with practical experience managing escalations across diverse property types, from simple office leases to complex retail agreements with CPI indexing and CAM pass-throughs.

We've helped 200+ companies implement compliant lease accounting since ASC 842's effective date, processing lease portfolios from 10 to 500+ locations. Our approach delivers technical accuracy at 40-50% less cost than expanding in-house teams, with dedicated accountants who understand both GAAP requirements and practical lease administration.

Whether you're transitioning to ASC 842 for the first time, discovering errors in current lease accounting, or need ongoing support managing escalations across growing property portfolios, we provide the expertise that keeps financial statements audit-ready and compliant.

Related read: asc 842.

Single-entry vs double-entry bookkeeping made simple: how each accounting system works, the key differences, and which one your small business needs.

%2075-100%20(12).png)

CPA vs EA (enrolled agent) vs tax attorney: how each tax professional differs, who can represent you to the IRS, and which fits your tax needs.

%2075-100%20(9).png)

Learn how tax professionals should respond to a data breach, report theft to the IRS and states, notify clients, meet FTC rules, and prevent future attacks.